Over the past 6 years there was not a sign of the beer market stabilization, but now we can cautiously speak of it in three different aspects – economic, demographic and competitive. On the one hand, the changes are touching upon the consumption structure, i.e. the beer volumes drunk by different generations of the Russians are coming to equilibrium. On the other hand, the fall of beer sales by international companies was balanced by the growth of their smaller competitors. The economy in 2016 is more stable, the spring-summer season passed without shocks and the Russians, heated by the good weather, thought of beer. The year was marked by three events on the market, i.e. beer advertisement return to TV, Baltika’s sales fluctuations, and transition of Carlsberg and Gosser brands to the mainstream segment.

About zero

Beer market trends

Want something cheaper?

Want something Russian?

Want something alcohol-free?

The leading companies’ positions

Carlsberg Group

Efes Rus

Heineken

AB InBev

Beer consumption

Affordable delight

Will the youth support the market?

Hot season

About zero

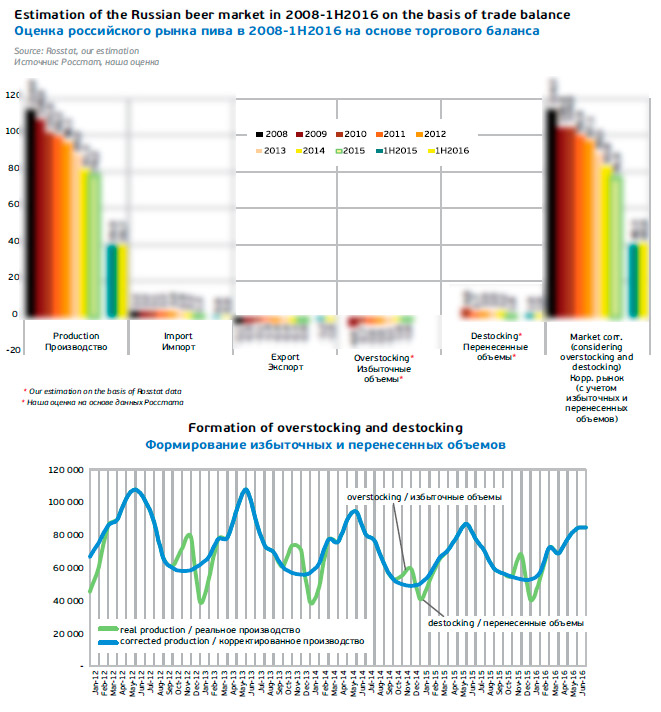

The production growth was observed in the first quarter of 2016, and then there was a minor correction. As a result, by the end of the first half of 2016, the beer production expanded by 0.7 % to 39.7 mln hl. Judging by inspiring operational data for July (+8%) and August (+9%) the third quarter and the year in general will also show positive results.

According Rosstat data, the beer sales in the first half-year of 2016 fell by 1.6 % to 38.7 mln dal (-8.4 % in the first half of 2015). Taking into account the Unified State Automated Information System introduction into the wholesale and retail trade, one can assume that these figures started reflecting the actual market volumes. And the dynamics improvement indeed took place.

The decline slowdown is also spoken about by Marina Lapenkova*, global companies cooperation director at «Nielsen Russia». According to the retail audit, beer sales in 1H2016 fell by 3.6 % year to year by volume, while in 1H2015 the decline equaled 6.2 %.

* Vedomosti #4130 of 03.08.2016 “Beer almost at bottom”

Besides, the estimated market size – the trade balance – is also undergoing the transition from the decline to zero dynamics. Over the first half-year, it declined by 0.5 % to 38.7 mln hl. In the trade balance estimation we took into account the growth of the carry-over stocks volume against 2015. This growth resulted from no excise increase in 2015 and in 2016 there was a 2 ruble/liter increase which incited producers to load the warehouses before the New Year. But even if we take into account these volumes, the trade balance was a little behind the production dynamics, which can be explained by fast growth of Russian beer export.

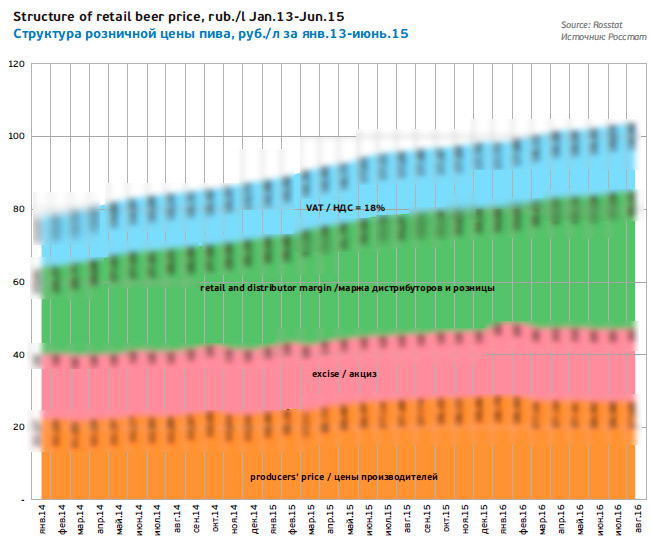

According to Rosstat publication, from March 2015 to January 2016, brewers were constantly raising the producer’s prices. The first half of 2015 saw the most rapid price increase. In the first turn, the increase was caused by international companies’ strive to offset the currency revenue decline according to brewers’ reports. Yet, in the first half of 2016, on the contrary, there was a minor correction. If we compare June 2016 and 2015, we can say the prices have returned to the former figures.

Basing on these data we can calculate brewers’ revenue volume. In 2015, it went …% up to RUB … bn. And in the first half of 2016, it grew by nearly …% to RUB … bn.

The ruble devaluation resulted in a dramatic collapse of brewers’ sales in dollars. In 2015, the revenue fell nearly …% to $… bn, and by …%, to $… bn in the first half of 2016. However, if we keep in mind that the ruble devaluation peak was passed at the beginning of 2016, by the year end, dollar revenue decline is expected to total less than …%.

The dynamics of retail prices for beer made in Russia, according to Rosstat data, since the beginning of 2015, has been in in phase opposition to price index for groceries. Obviously, the sellers were striving to retain the retail price for beer at moments of inflation surges most perceivable for consumers. Accordingly, at the start of 2016, when groceries prices almost stabilized, beer began getting more expensive rapidly, and the price dynamics did not level until May. A contribution into the beer price increase was certainly made by the excise growth from 18 to RUB 20 for a liter at the beginning of 2016.

Thus, the beer market by value was not much behind brewers’ revenue. Under our estimation, in 2015, it grew by …% to RUB … bn*, and in the first half of 2016, there was a …% increase to RUB … bn. In dollars the decline totaled …%, to $… bn, in 2015, and …%, to $… bn in the first half of 2016.

* The market volume in money terms is a conventional figure as about …% of beer is sold by HoReCa establishments and nearly …% is sold at the specialized beer retail, where the prices were not monitored and the trade mark-up can vary.

Beer market trends

Want something cheaper?

There is no surprise that in the crisis conditions, retailers and consumers are trying to meet halfway, and the sales of private labels in Russia have gone up rapidly. Understandably, among the retail networks, discounters have become particularly popular. And in them the share of private labels at most attractive prices is particularly large.

According to press publications of Nielsen audit, in IIQ2016, there was a stabilization of private labels following a rapid growth during 2015. By the end of 2016, the private labels share is likely to amount to about …% in city retail (and aprox. …% in the net beer sales volume under our estimation).

Audit data also show that in the beer category private labels share is several times lower than in other categories. The producer and brand are often important for consumers. Despite the quality improvement efforts, and intensive inter-network promotion, such beer would still create “unoriginal” image because of the low price, plain-spoken marketing and brand existence only within the network. So the growth of beer private labels is driven by a forced necessity to adapt to the crisis that the Russians are currently facing. The market share of owned brands stabilized mostly due to stabilization and reduction of prices for affordable mass brands.

A danger, greater than private labels for the leading producers, was lying in promo actions by owned brands which have become routine. In 2016, almost a third of beer volumes sold in supermarkets, was purchased at discounts or engaging other methods of purchase incentive.

Yet, the fast promo package growth started as far back as in 2013 and was connected not to consumers’ economizing but to the competition and efforts to retain mass brands sales. This trend was strengthened by the economy problems later.

Want something Russian?

Want something Russian?

What is then the sales engine of regional brewers? Can we say they take the share from the mass brands only by the price competition? It looks like the main role in these processes belongs to patriotic feelings which were openly expressed by the Russians in the course of a recent poll.

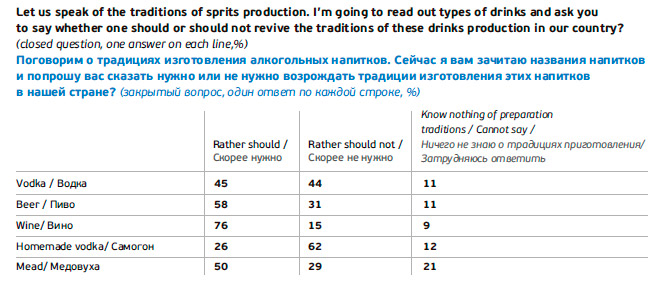

At the sales season start, Russian Public Opinion Research Centre (VCIOM) asked the Russians, which beer they preferred to see on the shelves*. The findings say the Russians want “the Russian brewing traditions to revive” and look forward to seeing “traditional Russian beer” on offer.

* VCIOM polls were held on 31 April – 1 May and 4-5 June 2016. The polls were carried out by telephone interview by stratified double-based random sampling of fixed and mobile numbers to the volume of 1600 respondents. The sampling was formed basing on the full list of phone numbers active in the RF. The data are weighted to selecting probability and by social and demographic parameters. For this sample the upper limit size of error with 95% probability does not exceed 2.5%.

Certainly responds allocation was much dependent on personal attitude to various drinks consumption and their social image. While the idea of reviving the tradition of home distilling was received negatively, opinions as for vodka divided into two equal parts, fermented beverages – wine, beer, and mead got a positive reaction.

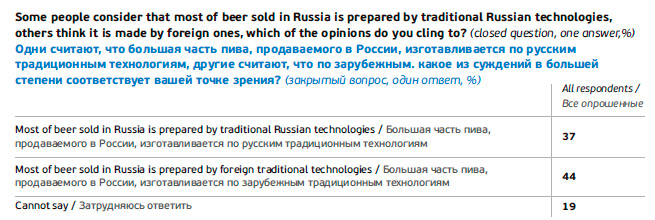

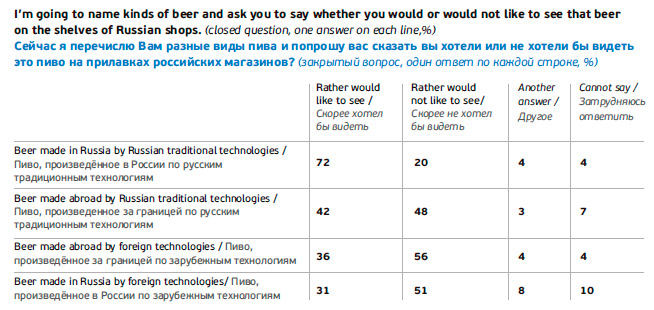

The poll demonstrated the wide spread opinion that most of beer on the shelves are manufactured in the country by “foreign”, not Russian technologies (…% against …% accordingly). Meanwhile, …% of the respondents would like to see beer produced by Russian traditions on the shelves, and only …% would prefer products made by foreign technologies.

The poll demonstrated the wide spread opinion that most of beer on the shelves are manufactured in the country by “foreign”, not Russian technologies (…% against …% accordingly). Meanwhile, …% of the respondents would like to see beer produced by Russian traditions on the shelves, and only …% would prefer products made by foreign technologies.

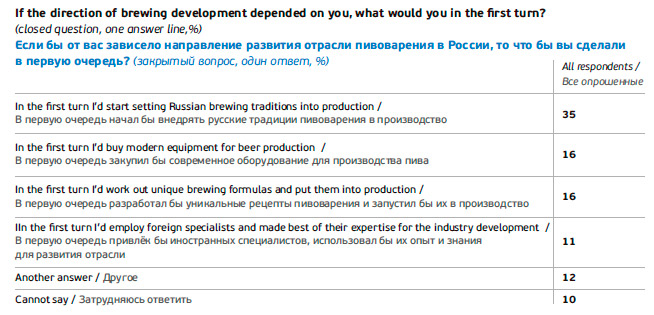

In this light, reviving of Russian brewing traditions is among others the most promising direction for the home brewing industry according to the Russians (…% said so). The idea of employing foreign specialists and making use of their experience is supported by much less (…%).

Mentioning the traditions of the Russian brewing most probably appealed to respondents’ associations with nostalgic images (Zhigulevskoe Yachmennyi Kolos and others), as well as with original tastes of regional beer.

Want something alcohol-free?

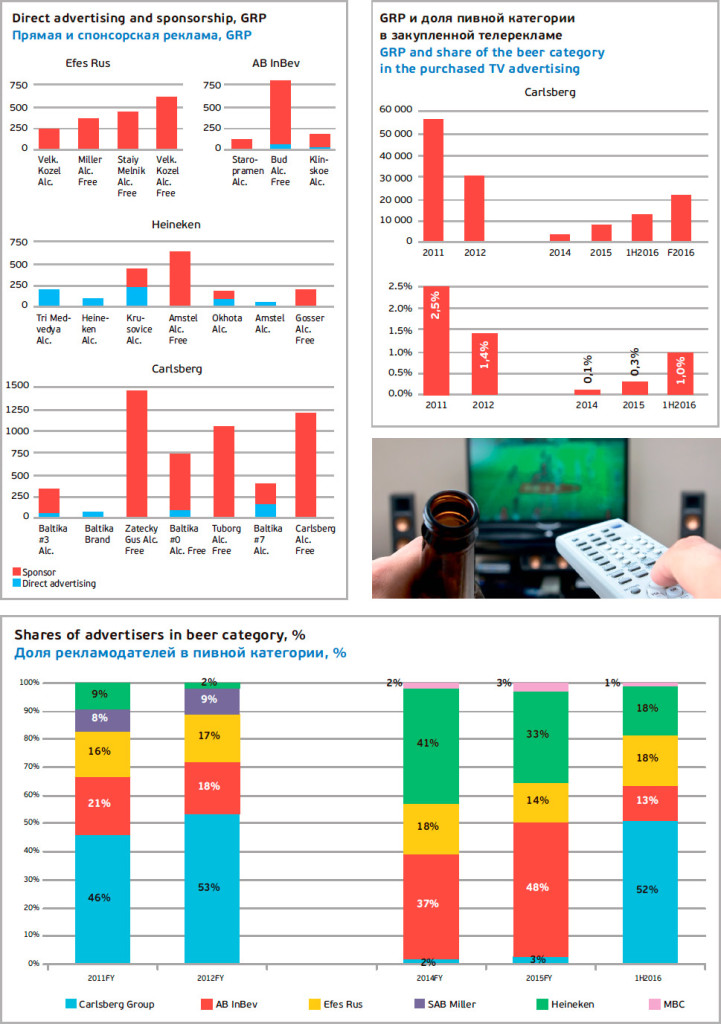

Another big event of 2016 is the full scale return of beer ads to TV. Without advertisement major companies found it too difficult to support the image and the adequate positioning of the mass brands.

According to OMD OM Group’s * analysis, the end of 2014- beginning of 2015 was marked by a mighty collapse of the Russian advertisement market. Analysts Skorodumov and Anton Yefimov comment on the situation of those years: “Quite negative outlooks for 2015 prevented beer advertiser from expanding marketing budgets significantly.

* OMD OM Group analysis of advertising activity in the beer industry prepared for Sostav.ru.

Besides, the absence of landmark sport events in 2015 and production capacities adaptation for non-alcoholic beer also took toll.

The point is, according to the amendments to Advertisement act in force, alcohol beer advertisement on TV is permitted only during sports translation, as well as on the specialized sports channels. The most reasonable option in this case is to buy a sponsor’s packet of the major sports events on TV, and placing direct commercials within the broadcasts, which is actively practiced by advertisers.

Not until 2016 have we seen a serious activation of beer advertisers on TV – this was connected both to recovery of relative stability in the economy (that is, a more long-term planning), and to an impressive list of the sport events (hockey world championship in Moscow and football Europe championship in France, Summer Olympic Games and others)”.

Not until 2016 have we seen a serious activation of beer advertisers on TV – this was connected both to recovery of relative stability in the economy (that is, a more long-term planning), and to an impressive list of the sport events (hockey world championship in Moscow and football Europe championship in France, Summer Olympic Games and others)”.

The advertising activity that has grown very high displeased the Rospotrebnadzor. The Federal Service considers that storylines of the commercials are taken by consumers as promotion of alcoholic drink, but not its alcohol-free analogue. According to newspaper Izvestia, at a consulting meeting with the Federal antimonopoly service, Rospotrebnadzor’s officers were suggested to carry out a poll among viewers to find out whether they really perceive such promotion of alcohol-free beer as an ad of alcoholic products. The poll is to be carried out by the Service during the next 6 months.

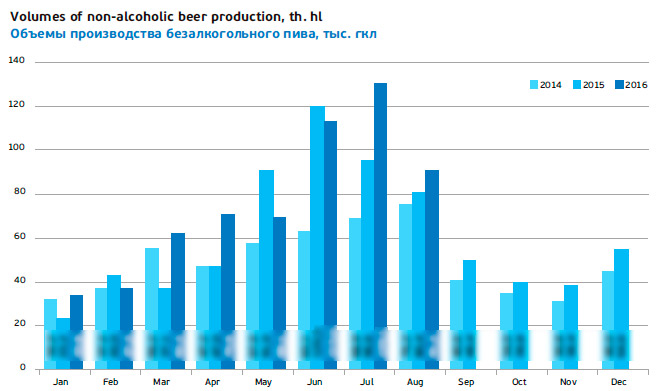

The producers argue that the ad and promotion of non-alcoholic beer induces a gradual shift to alcohol-free products. Over the recent years, a rapid growth of non-alcoholic beer production was registered by Rosstat. In 2015, it equaled …% and by the end of 2016, it is likely to reach …% to … mln dal. This category growth is almost fully a merit of the major producers.

One more threat for alcohol-free beer is associated with a possibility of excise introduction. The RF Finance Ministry offered to tax it at the same level as alcoholic beer “… in order to provide balance to budgets of the Russian Federation subjects”. As of now, beer with …% alcohol content inclusively (that is, virtually alcohol-free) is levied by “zero” excise.

The leading companies’ positions

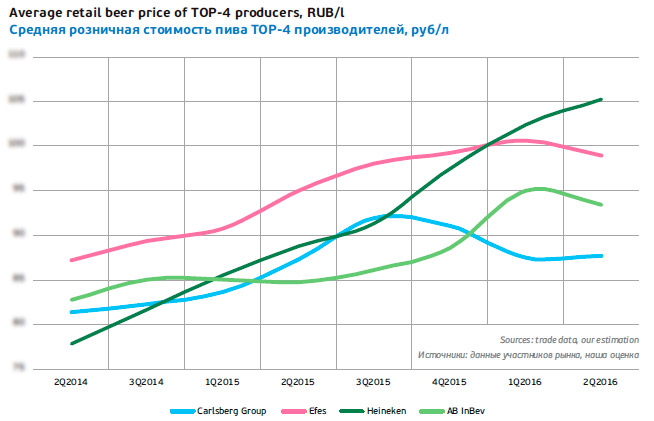

Slower rates of decline in beer production and even growth during the summer 2016 can be considered a consequence of two opposite trends’ balancing. The sales fall of four transnational companies was for the first time offset by a growth in “other” producers.

This tendency formed in 2015, but then the sales of TOP-4 were decreasing too fast and pressed the market too hard. The leaders’ share has fallen by … p.p. to …% over one year which can be called an unprecedented collapse. In the first half of 2016, the TOP-4 decline almost stopped.

If we take up the situation by companies, the event on the beer market was the market leader’s, that is, Baltika’s, sales nose-dive in the second half of 2015. The subsequent partial recovery turned out to be not less significant.

Carlsberg Group

Carlsberg Group

In 2015 Baltika cut down its sales and market share considerably. According to the company’s data, they fell …% and by our estimation amounted to nearly … mln hl. However, if we compare the first half-year of 2015 and 2016, the dynamics will look not so sharp. That means that the rapid decline took place in the second half of 2015.

By the way, leveling of the negative dynamics meant that the low base effect can result in a slight sales growth of Carlsberg Group by the end of 2016.

The reduction of Carlsberg Group’s market share was to a considerable extent caused by rapid price increasing started in May 2015. This decision was certainly taken because of the ruble devaluation and efforts to offset the currency revenue fall, so it was a forced decision. The share decline resulted from the company’s “price leadership” in summer 2015, as said in Carlsberg’s message. But the price increase turned out to be untimely in the run-up to the sales season and against a more cautious policy of other producers. The market average prices were growing gradually without leaps, so difference was very much marked. As a result, according to the market players’ data, sales of Baltika brand as well as of some regional brands started shrinking rapidly in the middle of summer, the most important brewers’ season.

In previous years, Carlsberg Group managed to refocus the mass consumer onto premium Baltika №7, which became the major subbrand in the company’s portfolio. Yet, currently all the key brands are experiencing a sales fall, including Baltika №3 and Baltika Cooler, which have been long and quite intensively losing their market share.

In its yearly report the company said the decline was linked to consumers’ shifting to cheaper local brands. However, in the fourth quarter of 2015, the trend changed, and the company’s market share started recovering rapidly, having almost returned to the previous level by the year end. In our view there are four major reasons, why the company managed to return the lost volumes.

In its yearly report the company said the decline was linked to consumers’ shifting to cheaper local brands. However, in the fourth quarter of 2015, the trend changed, and the company’s market share started recovering rapidly, having almost returned to the previous level by the year end. In our view there are four major reasons, why the company managed to return the lost volumes.

Firstly, by the year end, when it became obvious that the sales were falling, the prices for Carlsberg Group’s products stopped growing too. Then, there was a correction and they started approaching the Russian average as after Carlsberg Group other producers sooner or later joined the price races. Now the retail prices for the company’s brands seem average against the competitors’ price increase. That is, the conditions that caused the rapid sales decline were removed.

Secondly, the company started a serious price offensive at the economy beer segment. The company reduced the price for people’s brand “Zhigulevskoe” sharply.

Most producers place their Zhigulevskoe brand into the economy segment. However Carlsberg Group positioned it nearly at the lower border of the mainstream segment. The price collapse at the end of the last year was so deep, that Zhigulevskoe by the market leader moved to the discount segment and became cheaper than most of its counterparts by regional producers. For example, its price in the first quarter of 2016, was approximately at the level with the private trade marks by the retail networks.

Quite naturally, that consumers who set themselves up for economizing, appreciated the attractive offer, and market share of Zhigulevskoe by Carlsberg Group grew … according to the market participants’ data. However, Zhigulevskoe was not able to fully offset the market share decline of other brands by the company.

Thirdly the restoration of Carlsberg Group’s market share in the first half of 2016 was followed by a heavy promotion. According to OMD OM Group analysis, before the beer advertisement was banned in 2012, Carlsberg Group was the absolute leader in the category, with a share of about …%. In 2014-2015, the traditional leader was not particularly active, but in 2016 again steadily won more than …% of the air time.

6 brands and subbrands were heavily promoted. In descending order of GRP, the non-alcoholic brands list looked this way Zatecky Gus*, Carlsberg*, Tuborg*, and Baltika №0, as well as alcoholic Baltika №7 and Baltika №3. For instance, subbrand Baltika №3 was one of the major beer sponsors of the Hockey World Championship and in summer 2016, the subbrand had its package renewed for the first time in 9 years. Baltika №7 became the official sponsor of UEFA EURO 2016.

6 brands and subbrands were heavily promoted. In descending order of GRP, the non-alcoholic brands list looked this way Zatecky Gus*, Carlsberg*, Tuborg*, and Baltika №0, as well as alcoholic Baltika №7 and Baltika №3. For instance, subbrand Baltika №3 was one of the major beer sponsors of the Hockey World Championship and in summer 2016, the subbrand had its package renewed for the first time in 9 years. Baltika №7 became the official sponsor of UEFA EURO 2016.

* Alcohol-free brand sorts

However, despite the media support, the share growth of Baltika №7 and Baltika №3 did not grow but rather stabilized after the decline in the first half-year of 2016. Apparently, the share of Baltika Cooler went on reducing rapidly too. Instead, “polar” by alcohol content sorts, namely, strong Baltika №9 and, understandably Baltika №0, saw their sales rise. But in our estimation their growth could no way offset the fall of the leading three subbrands.

Brand was launched in non-alcoholic format and received a full scale advertisement. The main character of the new advertising campaign is a bearded brewer with a goose in his arms. The bird’s name is Pan Gus and it expresses its respect by a glass of Zatecky Gus Non-Alco. As yet, the brand positions are fluctuating despite the TV promotion, so it would be too early to speak of a stable positive turn in dynamics.

In the fourth place, the market share recovery resulted from an unprecedented step by the company as it dramatically cut the price for its title brand Carlsberg. In the end of 2015, its retail price fell by …% approx. to RUB 90/l. In actual fact, former superpremium title brand became cheaper than Zatecky Gus and now is positioned in the mainstream segment. Consumers were enthusiastic with such step and by the year end, one can expect Carlsberg beer share to exceed …%, while it amounted only several tenths of a percentage point in autumn 2015. Such a knight’s move does not even contradict the premium brands positioning, as now there is a considerable price gap between them and Carlsberg. This step can be called only forced but it proved to be effective.

In the fourth place, the market share recovery resulted from an unprecedented step by the company as it dramatically cut the price for its title brand Carlsberg. In the end of 2015, its retail price fell by …% approx. to RUB 90/l. In actual fact, former superpremium title brand became cheaper than Zatecky Gus and now is positioned in the mainstream segment. Consumers were enthusiastic with such step and by the year end, one can expect Carlsberg beer share to exceed …%, while it amounted only several tenths of a percentage point in autumn 2015. Such a knight’s move does not even contradict the premium brands positioning, as now there is a considerable price gap between them and Carlsberg. This step can be called only forced but it proved to be effective.

Besides, according to Baltika’s data, referring to retail-audit by Nielsen Russia, in the first half year 2016, the company raised its share in the draft beer channel by … p.p. Such a rapid growth in the draft beer segment was obviously connected to an active promotion of Zhigulevskoe and regional brands. Owing to weak presence of other leaders on the keg beer market, Carlsberg Group’s sales growth is an alarm signal for independent regional breweries in the first turn.

At the same time, Carlsberg Group’s drift towards the economy segment is taking place against the sales decline of the major mainstream subbrands. That could point to a deterioration of the product mix, yet the rapid growth of the cheaper Carlsberg, can compensate the negative changes partially or even in full.

At the same time, Carlsberg Group’s drift towards the economy segment is taking place against the sales decline of the major mainstream subbrands. That could point to a deterioration of the product mix, yet the rapid growth of the cheaper Carlsberg, can compensate the negative changes partially or even in full.

Efes Rus

Efes company’s share has shrunk considerably since merging. After a certain stabilization in 2014, there again was a sales drop in 2015. Basing on the company report, we can assume that sales in Russia went …% down to … mln hl over 2015. The market was reducing at a slower rate, so the company’s share decreased.

In the first half of 2016, the reduction continued by approx. …% under our estimation. Yet at that time the company started gaining market weight and probably in the second half-year the dynamics will be better.

The company’s production dynamics by regions reflects a considerable volume redistribution from the center towards regions. A big brewery in Kaluga supplying beer to Moscow market, in 2015 maintained the output volumes, but cut them down by …% during the first half of 2016. At the same time beer output at Ulyanovsk brewery was growing rapidly. This growth has compensated the reduction not only in Kaluga but also in Ufa where the production volumes are falling at two-digit speed. In Kazan the output was decreasing slower than the market in 2015-2016.

At the same time, Efes sales decline during the first half of 2016 was to a large extent connected to sales redistribution by the price segments. The company has lost some of its positions at the inexpensive beer market, but aspires to leadership in the marginal segments of the market. Thus, having lost the volumes company has managed to improve its product mix considerably.

In the period of the fast beer market development, Efes made a mistake of focusing on the lower mainstream segment. One could tell the company’s portfolio is polarized and covers the lower and mainstream segment blurring the borders on both sides.

In the period of the fast beer market development, Efes made a mistake of focusing on the lower mainstream segment. One could tell the company’s portfolio is polarized and covers the lower and mainstream segment blurring the borders on both sides.

At that time brands Beliy Medved, Gold Mine Beer, and Green Beer in big PET packs came to the fore being affordable and actively promoted branded products at the same time. Their sales were fluctuating and Green Beer in 2016 virtually disappeared from the company’s portfolio. Yet, in 2014, the share of Beliy Medved, Gold Minе Beer was comparatively stable. Meanwhile, until 2014, there was a very rapid growth of Zhigulevskoe which was used by the company as a weapon against the regional brewers and declining production volumes. At the peak, these three brands provided almost a half of Efes sales on the Russian market.

However, in 2015, according to market players’ data, the sales of Beliy Medved, Gold Mine Beer started falling rapidly. Compared to them Zhigulevskoe by Efes looked better but also was yielding its positions. Yet, under market players’ estimation, in summer 2016, the company’s major brand Beliy Medved became more affordable and started regaining its sales.

The fall of the market share can be fully explained by Efes efforts to maintain the currency revenue and the lower mainstream positioning. That meant a fast growth of the retail prices for three affordable brands that started in spring 2015 and ended in autumn. By that time, the retail prices for beer Beliy Medved and Gold Mine Beer approached the mainstream and mass brands, but the growing popularity of regional brewers’ production aggravated the situation. Such condition of affordable brands by Efes was complicated by a fierce competition for shelf space in the net retail as well as other factors disrupting the competitive space (see below).

Mainstream Zolotaya Bochka that previously belonged to mass brands has also lost momentum. However, its positioning in the same category with Stary Melnik has apparently stood in the way to development in the conditions of sales decrease and shelf-space reduction. The brand share was shrinking especially in regions and it might even disappear from the portfolio or become regional. At least launching of sort Zolotaya Bochka Shabolovskoe especially for Moscow market bespeaks intention to convert the brands popularity into sales.

Mainstream Zolotaya Bochka that previously belonged to mass brands has also lost momentum. However, its positioning in the same category with Stary Melnik has apparently stood in the way to development in the conditions of sales decrease and shelf-space reduction. The brand share was shrinking especially in regions and it might even disappear from the portfolio or become regional. At least launching of sort Zolotaya Bochka Shabolovskoe especially for Moscow market bespeaks intention to convert the brands popularity into sales.

Efes refocusing onto premium brands is expressed by the advertising activity in the first half of 2016. The company has purchased much more broadcasting time, second to Baltika but at the level with the other two market leaders. Despite the drop of Beliy Medved and God Mine Beer sales the report by OMD OM Group does not contain any data of them being advertised on TV. Instead non-alcoholic and alcoholic sorts of Velkopopovicky Kozel were heavily promoted. The second and the third places were occupied by non-alcoholic Stary Melnik and Miller correspondently. Alcohol-free sorts in Efes portfolio appeared at the threshold of promotional campaigns.

Early in 2016, there appeared a new sort, Velkopopovicky Kozel non-alcoholic. The launch was supported by the advertising campaign, featuring a Czech hipster brewing beer at an old brewery and then, by a contest for bearded men.

Early in 2016, there appeared a new sort, Velkopopovicky Kozel non-alcoholic. The launch was supported by the advertising campaign, featuring a Czech hipster brewing beer at an old brewery and then, by a contest for bearded men.

The alcohol-free version of Miller beer was launched in spring, virtually at the same time with a promoting commercial. The brand was output in a can resembling a speaker box that also looked like Miller Genuine Draft designed as a speaker too.

When promoting brand Stary Melnik iz Bochonka Non-alcoholic, Efes kept in mind the growing interest to Russian traditions, so the brokage process with “sidling up” on barrels was depicted.

The promotion campaign of new alcoholic sort Stary Melnik Svetloe iz Bochonka was made in the same spirit. Marina Dolnikova, Efes Rus marketing manager commented on it in the following way: “When people speak of brewing, they normally think of Germany or Czech republic, but not of Russia. However, anciently in Rus there were our own original brewing methods as well as a host of traditions connected to beer consumption. This allows us to say that in Ancient Rus beer was a classic drink just like in Europe”.

All three promoted brands, Velkopopovicky Kozel, Miller, and Stary Melnik iz Bochonka had a good performance in the first half of 2016 as far as we know. At least, the company claimed to be a leader in the premium market segment in its half-year report.

Heineken

After a certain stabilization, company Heineken started losing its market share again as the crisis outburst. Under our estimation, in 2015, it went …p.p. down to …% and in the first half of 2016, it dropped by … p.p. to …%.

Russian sales of Heineken in 2015 fell …% to … mln hl and in the first half of 2016 continues falling at the same rates, that is, were worse than the market.

Regional Rosstat data for the first half of 2016, show a dynamics deterioration of the output at Volga brewery in Nizhniy Novgorod (by up to -…%) and a … decline in the average at the breweries in Kaliningrad, Yekaterinburg, and in Irkutsk region. In Saint Petersburg the beer output apparently did not fall as the company started expressing an intention to expand the brewery’s volumes.

Regional Rosstat data for the first half of 2016, show a dynamics deterioration of the output at Volga brewery in Nizhniy Novgorod (by up to -…%) and a … decline in the average at the breweries in Kaliningrad, Yekaterinburg, and in Irkutsk region. In Saint Petersburg the beer output apparently did not fall as the company started expressing an intention to expand the brewery’s volumes.

However, the production expansion in Saint Petersburg can be connected to the company’s decision to cease beer manufacturing at Kaliningrad brewery starting from 1 January, 2017. That will be a third shutdown in Russia, though there has not been any for a long time since 2009. Under our estimation, in 2015, the volume decline of the brewery in Kaliningrad reached nearly …mln hl with the capacity of 1 hl. The two digit reduction went on in the first half of 2016.

The main reason for Heineken sales decline was stronger competition with regional brewers and the company’s being ousted from the economy segment.

After 2008, as a respond to volume reduction, Heineken decided to line up strong regional brands that compete with products by independent medium producers where company’s breweries operate. Zhigulevskoe enjoyed a very mighty sales increase as Heineken was one of the first companies that focused on this brand, both in package and kegs. At that the brand cost really little, unlike the counterparts by the other market leaders. Having these brands the company managed to secure a position at specialized shops selling beer on tap.

After 2008, as a respond to volume reduction, Heineken decided to line up strong regional brands that compete with products by independent medium producers where company’s breweries operate. Zhigulevskoe enjoyed a very mighty sales increase as Heineken was one of the first companies that focused on this brand, both in package and kegs. At that the brand cost really little, unlike the counterparts by the other market leaders. Having these brands the company managed to secure a position at specialized shops selling beer on tap.

So it is now clear, that the current increase of independent regional producers, who offer an affordable alternative as well as a competition escalation in the economy segment had such a negative effect on Heineken sales. According the market players, the volume of Zhiguleskoe fell by approx. a third and sales of many regional brands decreased even harder, sometimes by times.

However, the branding activity of the company bespeaks its efforts to overcome the negative trend by launching new unusual sorts at regional breweries. Let us look at the most prominent among them.

At the beginning of 2015, Heineken brewery in Irkutsk started delivering new regional brand Feilong with a “Chinese accent” which became the first one for the company in the segment of Asian rice beer. Feilong distribution was carried out by regions located in proximity of China, where Chinese traditions are known to the population. The sales have obviously equaled the company’s’ hopes and in 2016, the production was launched at plant Amur-pivo too.

At the beginning of 2015, Heineken brewery in Irkutsk started delivering new regional brand Feilong with a “Chinese accent” which became the first one for the company in the segment of Asian rice beer. Feilong distribution was carried out by regions located in proximity of China, where Chinese traditions are known to the population. The sales have obviously equaled the company’s’ hopes and in 2016, the production was launched at plant Amur-pivo too.

Inspired by the success of the regional “Chinese” rice beer, in summer 2015, the company started outputting “Japanese” rice beer. Okome brand was launched specially for the Far East population and it is positioned in the mainstream market segment. As far as we know, this regional brand has also showed a good performance.

Heineken brewery in Kaliningrad in February 2016, started bottling renovated beer Königsberg. This year, the company completed the brand relaunching having freshened up the taste and the label design, which has become emphatically German, depicting the history of the city.

In March 2016, Heineken tried entering the craft segment, by bottling beer “I am Stephan Razin”. This is classic pale ale brewed in English style with a bright hop aroma. The new brand designed was made by a studio that works with Russian craft breweries. According to Johnny Kahill, Heineken Russia marketing director, the new brand will be promoted to Petersburg markets where Stephan Razin has the strongest positions, the brand share fluctuating …% over the recent several years. Besides, in Petersburg craft beer is particular high.

In June 2016, Bashkiria retail got a new sort, namely Shikhan Grechnevoe, the first beer in Russia brewing with buckwheat grains. According to Georgiy Gubeladze, Shikhan brewery director, new brand manufacturing and taste experimentations is the only way to reinforce positions in such a competitive market as Russia. Besides, he noted that the home producers pay attention to the origin of beer ingredients and look positively at using primordially Russian products.

In June 2016, Bashkiria retail got a new sort, namely Shikhan Grechnevoe, the first beer in Russia brewing with buckwheat grains. According to Georgiy Gubeladze, Shikhan brewery director, new brand manufacturing and taste experimentations is the only way to reinforce positions in such a competitive market as Russia. Besides, he noted that the home producers pay attention to the origin of beer ingredients and look positively at using primordially Russian products.

National economy brand Tri Medvedya has lost some of the market share but demonstrated a better stability than regional brands and Zhigulevskoe, remaining one of the two major brands in the company’s portfolio. In 2016, Heineken made Tri Medvedya the sponsor of sports broadcasting on TV, in an effort to maintain its sales.

Quite unexpectedly there was a launch of sort Tri Medvedya zhivoe, despite the inflation of the live category. Yet it was this market space vacating that could have driven the launch. Besides, brand Tri Medvedya got rid of many ineffective sorts and became a good candidate for expansion.

In the mainstream segment of the beer market all Heineken sales volume is formed by beer Okhota. Being one of the two major brands in Heineken portfolio, it retains the leadership in the strong beer segment. However, the brand is gradually yielding its share. For example, the retail price for Baltika №9 in 2016 was reduced to nearly the level of Okhota, that is, corresponds to low mainstream segment. At that, the brand sales growth has obviously negatively affected Okhota market share.

Yet Heineken management considers the aggressive acts of Carlsberg Group to effect the marginal segment more. Commenting on the results of the first half of 2016, Laurence Debroux, CFO and Member of the Executive Board of Heineken N.V. said the following:

“It remains for us a well-managed and relatively resilient business, albeit in a market that remains challenging and difficult. So in the first half Heineken volumes declined high single digit, likely a bit more than the market and indeed one of our competitors has been aggressively reducing the prices of one of the premium brands and I can be more precise on that because the Carlsberg CEO made no mystery of the fact that they went aggressively to reduce the price on the brand Carlsberg in the first half. And that has been definitely detrimental to us in terms of volume. And we believe to the market in terms of profit in general.”

Let us notуe that Heineken had weapons against brand Carlsberg that grew cheaper, we can also say that the company provoked the competitor to some extent. In spring 2015, Heineken launched production of beer Gosser at major Russian breweries. The retail price for beer Gosser produced locally corresponds to Carlsberg price.

Licensed Gosser allowed balancing the brands portfolio in terms of their price positioning, stated Johnny Kahill, marketing director of Heineken Russia. “The company portfolio is getting an international brand comparable by price with Russian brands, which will be helpful in attracting a maximally wide beer audience” The launch of Gosser own brewery was followed by a three-months advertising campaign “155 years of men’s stories”.

In a year, according to the modern traditions of brand-building, the first batches of non-alcoholic beer were brewed in Gosser. Its launch is supported by advertising campaigns and claims of over-the-plan sales of the alcoholic brand version.

One can expect Gosser to become the major licensed beer in the company’s portfolio and leave Amstel behind by the end of 2016. Gosser market share is likely to amount to at least …%. Note that Gosser and Amstel are rather close by price positioning. That is why no wonder that amid the rapid volume increase of the Australian brand, the non-alcoholic version of Amstel has been getting a heavy advertising support in 2016, which allows it maintaining volumes.

One can expect Gosser to become the major licensed beer in the company’s portfolio and leave Amstel behind by the end of 2016. Gosser market share is likely to amount to at least …%. Note that Gosser and Amstel are rather close by price positioning. That is why no wonder that amid the rapid volume increase of the Australian brand, the non-alcoholic version of Amstel has been getting a heavy advertising support in 2016, which allows it maintaining volumes.

One could say that the company was doing not bad in the mainstream segment even amid the crisis. Yet the market share of Doctor Diesel and Zlaty Bazant, that do not get any promotion any more, is shrinking. Bochkarev, once being one of the biggest brands has almost disappeared from the market.

Till the end of 2016, Heineken has become the exclusive sponsor of the best rated sports broadcasts of Match TV channel, which are supported by brands Heineken, Krusovice, Amstel, Okhota, and Ttri Medvedya. Against the higher media activity of other brewers, this contract looks good. Albeit in 2014 Heineken was a major advertiser, currently its advertisement weight is roughly equal to its position among the market leaders.

The sale volumes in the premium segment in 2015 were driven by brand Krusovice. The licensed launch and retail price drop of the “royal” brand which was once a leader in the import beer market, made it possible to reach the same popularity level as title Heineken brand. After such lift-off, the growth prospects of Krusovice are likely to have reached the maximum.

The sale volumes in the premium segment in 2015 were driven by brand Krusovice. The licensed launch and retail price drop of the “royal” brand which was once a leader in the import beer market, made it possible to reach the same popularity level as title Heineken brand. After such lift-off, the growth prospects of Krusovice are likely to have reached the maximum.

Yet the company’s nearest prospects in the market of marginal beer look positive. Following pilot import deliveries, in spring 2016, Heineken started bottling Singaporean beer Tiger, one of the top brands in Asia and the Pacific region, under a license. In Russia Tiger is positioned in the premium segment (approx. RUB 120/l) and promoted mainly in big cities with a population of more than a million people.

Thus, one can speak of a significant change in the company’s sales structure. In the regional markets Heineken is following specialization trend, yielding its positions to independent producers. Besides the brands portfolio is actively reformatting giving ever bigger space to the world-known brands and getting rid of once popular ones. In general, this is to result in a considerable improvement of product mix, despite the big volume loss.

AB InBev

A protracted reduction of AB InBev market share seems to have stopped in 2015, yet it gained momentum in the first half of 2016. The Russian sales of the company in 2015 declined by …% to … mln hl and the rates were nearly the same in the first half of 2016.

Under our estimation, AB InBev market share has gone … p.p. down to …% during this half-year. However, taking into account Heineken’s faster decline, over this and next year, AB InBev can get back to the third position in the leaders’ list.

The main problem of AB InBev was similar to that of other market players, namely consumers’ interest decline to the old Russian brands. Once catching up with the Russian market leader, the company was basing its strategy on development of megabrands such as Tolstyak, Klinskoe, and Sibirskaya Korona, as well as licensed beer. Other brands either played a minor role initially or have been squeezed out in the fierce competition as company’s competitors have been more active and flexible.

In 2015, AB InBev according to OMD OM Group data was a major advertiser on TV having reached almost a half of GRP in the beer category. Apparently this unusually high activity gave AB InBev’s brands an advantage. Yet, in 2016, this advantage is no more here, as other market players have also gone on the air.

Apparently, the global beer leader’s marketing policy has been influenced by the global competition rather than the local realities. But still the global strategy of Bud promotion has allowed AB InBev going beyond the constant frame of the three weakening brands and finding a new footstep in the Russian market.

In terms of the sales dynamics by the price segments, 2014-2016 has been the most problematic period for the economy brands by AB InBev. The company reacted to the protracted volume decline in summer 2014, by launching new discount sort Tolstyak Zhivoe. The subbrand has indeed “livened up” Tolstyak’s volumes, rapidly becoming its major sort and converted the negative trend for a long time. But in 2015after the summer nostalgia for “live” beer, the interest to the brand withered again. Since then, the positions of Tolstyak Zhivoe, have looked unsteady, and the brand is not likely to repeat its success in the season of 2016. On the one hand the acquaintance effect has already passed, on the other hand, regional companies as well as competitors who again got interested in “live” beer stand in the way.

In terms of the sales dynamics by the price segments, 2014-2016 has been the most problematic period for the economy brands by AB InBev. The company reacted to the protracted volume decline in summer 2014, by launching new discount sort Tolstyak Zhivoe. The subbrand has indeed “livened up” Tolstyak’s volumes, rapidly becoming its major sort and converted the negative trend for a long time. But in 2015after the summer nostalgia for “live” beer, the interest to the brand withered again. Since then, the positions of Tolstyak Zhivoe, have looked unsteady, and the brand is not likely to repeat its success in the season of 2016. On the one hand the acquaintance effect has already passed, on the other hand, regional companies as well as competitors who again got interested in “live” beer stand in the way.

Klinskoe brand is still among the key ones in the Russian portfolio of AB InBev, under our estimation, accounting for a third of the volumes, though this share is gradually decreasing. Previously, the company tried to liven up sales by launching various bright sorts, but they gradually leave the market, and today, Klinskoe is becoming simply “light” (with a sort share in volumes exceeding …% under our estimation).

During 2015, AB InBev was striving to keep down the retail prices for Klinskoe, and that helped the company not to lose the brand’s market share, while the competitors started raising prices by steps. Ever bigger volumes of Klinskoe were sold in PET package, which now accounts for a significant sales volume. Indeed, the beer in PET of big volume was competing by price with economy brands. That is why, while Klinskoe retail price was kept down, the brand expectably was growing more attractive to consumers of less promoted products. But when AB InBev started raising prices, though much behind other brewers, consumers’ attention and the marked shared dropped.

During 2015, AB InBev was striving to keep down the retail prices for Klinskoe, and that helped the company not to lose the brand’s market share, while the competitors started raising prices by steps. Ever bigger volumes of Klinskoe were sold in PET package, which now accounts for a significant sales volume. Indeed, the beer in PET of big volume was competing by price with economy brands. That is why, while Klinskoe retail price was kept down, the brand expectably was growing more attractive to consumers of less promoted products. But when AB InBev started raising prices, though much behind other brewers, consumers’ attention and the marked shared dropped.

At the same time, the mainstream beer in can and glass bottle suffered from consumers’ economizing and experienced a strong pressure on the part of regional brands. To a certain extent Klinskoe might have been negatively affected even by related Zhigulevskoe standing near on the supermarket shelves and in fridges. Besides, many key brands by competitors in the first half of 2016 received more promotion than Klinskoe did.

Sibirskaya Korona which is positioned in the upper mainstream segment has been losing its share since autumn 2014. Obviously this brand suffered from licensed specialties launched by competitors in the same price segment. Note that not only Sibirskaya Korona has faced problems, but the most of the “old” marginal brands have. Under the conditions of limited promotion, they lack brand’s power to stand against the international names.

AB InBev continues attracting unusual beer lovers by specialties under Sibirskaya Korona umbrella. At the end of 2015, on the back of strong beer popularity rise, sort Sibirskaya Korona Krepkoe was launched. The new sort with a 8.3% strength is brewed with Citra and Chinook hops addition, which is widely used by craft brewers.

At the same time, the company has got inspired by the national images having output range Siberian Character. Each of the three sorts has a bright distinctive taste and is dedicated to one on the Siberian animals. These are IPA “Altaian Sapsan”, rye ale “Amur Tiger”, and stout “Taiga Brown Bear”. The retail price of these sortsapprox. RUB 140/l) corresponds to the premium segment. A non-standard for big brewers approach and advertising campaign started in summer 2016, attracted attention of original beer lovers.

At the same time, the company has got inspired by the national images having output range Siberian Character. Each of the three sorts has a bright distinctive taste and is dedicated to one on the Siberian animals. These are IPA “Altaian Sapsan”, rye ale “Amur Tiger”, and stout “Taiga Brown Bear”. The retail price of these sortsapprox. RUB 140/l) corresponds to the premium segment. A non-standard for big brewers approach and advertising campaign started in summer 2016, attracted attention of original beer lovers.

Yet, as of now, the market shares of strong beer and Siberian Character range are measured in tenths of percentage. Original and expensive specialties in the nearest future will not be able to compensate the decline of the major sorts Klassicheskoe and Svetloe, but there seem not be any other development ways left for the “old” Russian brands.

In spring 2016, Bloomberg wrote that premium Bud volumes in Russia are catching up with Klinskoe brand. Certainly, as yet, there is big distance between them. But Bud has become the second in the company’s portfolio, and if the current trend persists, it can become the first one in several years.

In spring 2016, Bloomberg wrote that premium Bud volumes in Russia are catching up with Klinskoe brand. Certainly, as yet, there is big distance between them. But Bud has become the second in the company’s portfolio, and if the current trend persists, it can become the first one in several years.

Higher priority of Bud over the local brands appears from both the company’s global strategy and the fact that only Bud got a considerable advertising support in the first half of 2016 according to OMD OM Group data. By the way, non-alcoholic Bud, which is an international FIFA partner, was the first brand to place a TV commercial in June-July 2014, after the amendment to advertisement legislation was adopted.

According to the strategy of the global positioning, Beer Bud with a price of RUB 110/l is to take the mass sort role in the premium segment. Stella Artois costing nearly RUB 160/l will remain one of the best-selling brands in the superpremium segment. Beer Corona with its retail price of RUB 260/l is to occupy the first position in AB InBev marginal segment range and one should expect its market share to expand.

Thus, Bud is claiming the first positions in the premium market segment, yet the today’s leader, Velkopopovicky Kozel, is not going to yield its position to Bud. Besides, after the transit to the mainstream segment, Carlsberg has become Bud’s competitor. If we speak of the whole category of licensed brands, Carlsberg will exceed Bud by sales volumes in 2016. The title brand by AB InBev will face serious difficulties keeping the consumers of international brands loyal.

The old licensed brands by AB InBev, namely Lowenbrau, Hoergaarden, Staropramen, and Stella Artois in the first half of 2016, maintained stability and even grew a little. At the same time, AB InBev has become the absolute leader of the import beer market with a share of …% (see article Import beer market). For instance, the company’s portfolio contains import brands #1 and #2 in the Russian market, namely Spaten and Corona.

Certainly, the import is already influencing the company’s sales. Its share in natural terms will amount to …% by the end of 2016. And taking into account that the average retail price for import beer is at least three times more than that of a local beer, in monetary terms, the import share will exceed …%.

Domination in the import segment, Bud’s growth, and the volume decline of cheap beer means that though the natural volumes are decreasing, and the largest brands have lost their stability, AB InBev is improving the sales structure and adapting to the new market conditions in the stress mode.

Beer consumption

Affordable delight

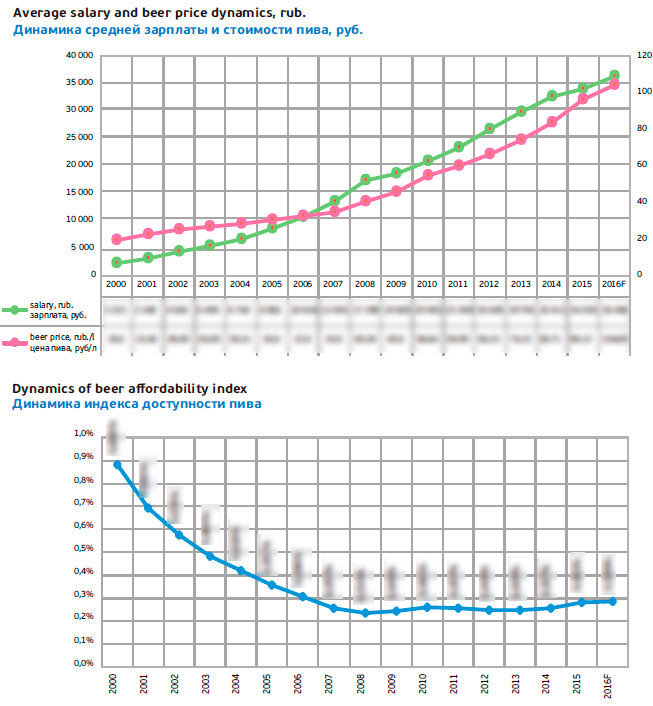

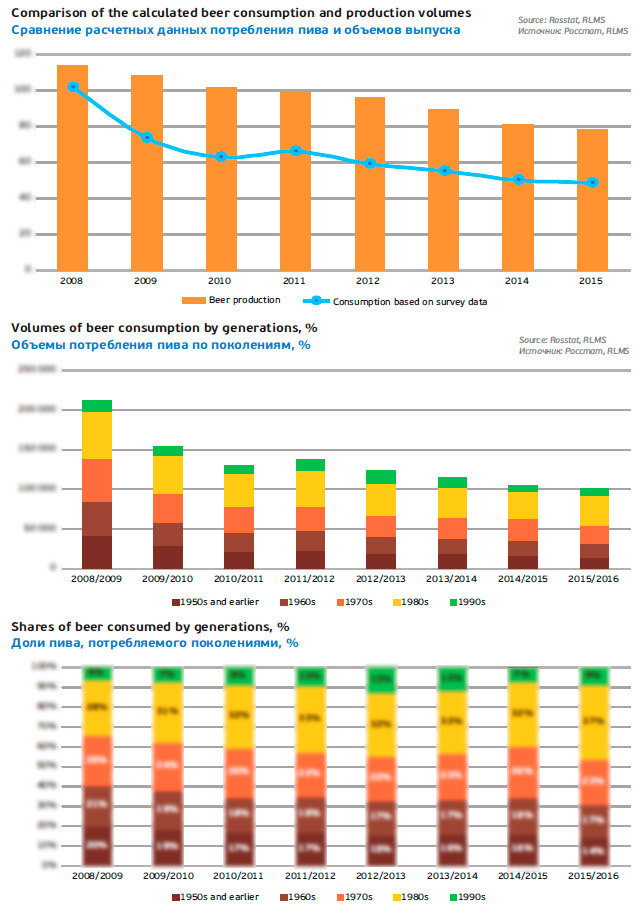

The riot growth of beer consumption till 2008 was associated with a considerable decline of the poverty level and the middle class increase. The Russians’ welfare was growing at a much higher rate than beer price. This trend is particularly well demonstrated at the graph of beer affordability (the proportion of beer price in the wages).

Turning point in the riot growth of beer consumption coincided with the beer affordability stabilization. In the subsequent reduction of the beer market share the main role was played by demographics and state regulation. In 2015, the state regulation did not much influence the market, but the affordability index grew substantially for the first time in many years.

However, it is known that change in beer prices does not influence its consumption as much as the general economic situation (comparatively stable results of 2010 are a good proof of it as then prices leapt due to the excises). In 2016, some important for consumers economic factors look better if compared dynamically to 2015.

• In the conditions of falling market, producers and sellers were striving to keep process down prices even at the expense of their own profits.

• Salary growth is almost at the level with the beer prices growth, that is, the affordability index has stabilized.

• The inflation of 2016, though high, has slowed down by two times, ruble is comparatively stable, the official level of unemployment has not gone up.

However, according to Romir data, austerities, introduced by the consumers after the shocks of 2015, are not loosening but even toughening. The dynamics of nominal expenses of the Russians are still positive due to salaries growth. But the real, that is, clear from inflation expenses of the Russians were this summer lower than last three years, and in August the expenses index fell from … to …%*.

* 100% = January 2012

The fact that the decline of the actual expenses was not followed by beer market decline can be explained by alternations in the structure of the expenses. For example, in August 2016, those who economized were among high income population group (…%), while the middle and low income groups virtually retained the income level (…% and …%, respectively).

For most people beer is an impulse product they can well do without in the austerity regime. The decision whether to economize on unnecessary products depends not so much on affordability of a certain commodity as on awareness of its purchase appropriacy in the present economic condition. And the material condition depends on the real income dynamics relating to the inflation and the consumption structure.

The share of food items in the general daily basket of the Russians in August 2016 returned to …% after a sharp leap to …% in July. Apparently not the conscious economizing by consumers was the reason, but it was caused by the seasonal price reduction for vegetables and fruits. In any case, the Russians could spend more on not basic goods. Beer is still one of the first affordable “unnecessary luxuries”.

Thus, we can say that the high season of beer sales 2016 took place in relatively steady economic situation. The Russian beer market was able to stabilize with no shocks hitting.

Will the youth support the market?

In order to better understand the outlooks for the beer market, let us try and analyze the fundamental demographic factor basing on the data obtained by the regular polls.

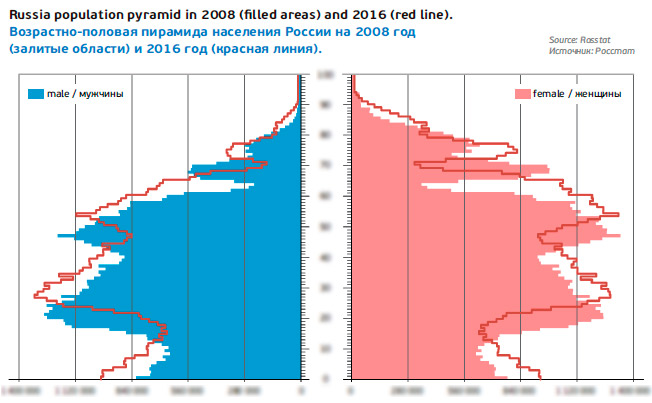

The fact that draws your immediate attention is that the age groups’ size changes work against the beer market.

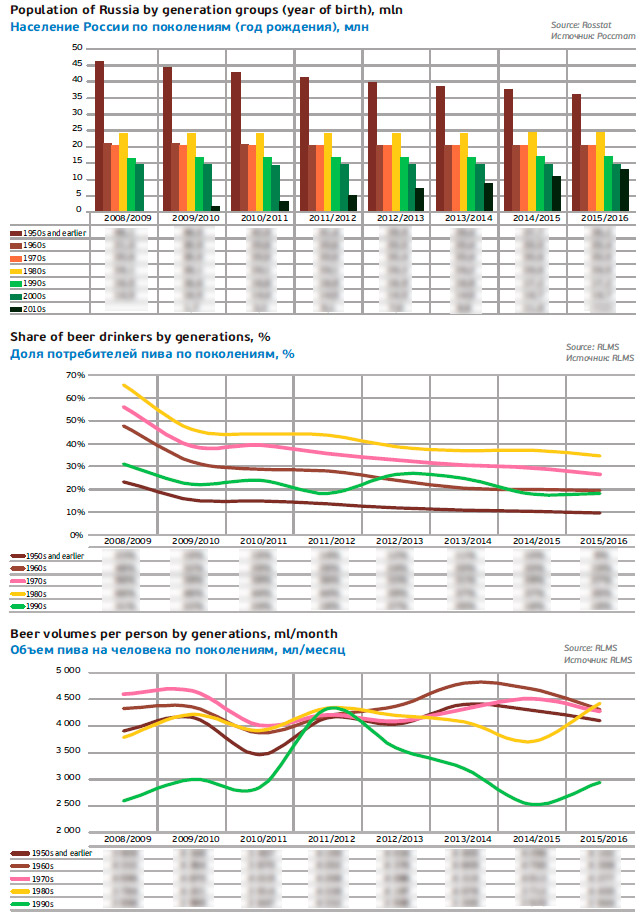

In the peak year for the beer market 2008, there were … mln of men aged 18-25. But by 2016, the number of people who drove the beer consumption ten years ago became …mln, that is decreased by …%. This means that dwindling inflow of youth was for a long time unable to compensate for going of aging beer lovers.

Presently, Russia is already at the lower demographic point of population aged 16-19. And from now on the beer consumption could have started improving as the number of teen-aged population born in the noughties, has started growing. Yet, before predicting a positive influence of demographics, one should pay a thorough attention to youth’s attitude to beer.

Born in the 90-ies

It is possible to assess the attitude to beer of the youth basing on the share of beer consumers among them. And we excluded those who, during the poll, could not tell how often he/she drank and how much was drunk.

Thus years 2008/2009 were not indicative, as the poll results give evidence of an abrupt reduction of consumption by all generations due to the economic problems. But then one would expect the generation born in the 90-ies to consume more beer as they grow older and pay attention to alcohol. However, this share did not grow fluctuated and by 2014/2015 it stabilized at the minimum level – …% (in 2008 the share of beer consumers in this generation was …%).

Thus years 2008/2009 were not indicative, as the poll results give evidence of an abrupt reduction of consumption by all generations due to the economic problems. But then one would expect the generation born in the 90-ies to consume more beer as they grow older and pay attention to alcohol. However, this share did not grow fluctuated and by 2014/2015 it stabilized at the minimum level – …% (in 2008 the share of beer consumers in this generation was …%).

In other words, many young people gave up beer before tasting it properly.

One would expect teenagers to drink more beer as they grow older. Indeed, the volumes of consumed beer per capita grew sharply by 2011/2012. At the same time, those who consumed small volumes of beer dropped out from the consumers’ group. But then, the consumption volumes per capita started decreasing rapidly and have just gone a little up.

Obviously, the youth started drinking less due to stricter regulation of beer consumption and sale. Since 2005, it has been forbidden to drink beer outside and since the end of 2012, one has not been able to buy beer in the nearest kiosk. Thus, the consumption decline 2012/2013 was reflected by the poll data.

However, not only beer but also strong alcohol consumption experienced decrease, while that market did not overcome any dramatic changes of regulations. There are ever fewer people who consume any alcohol. Their share reduction (same as per capita consumption volume) supported the world trend of lower frequency of teen age alcohol consumption, first registered in 2006. This turning point is discussed in the article*, published in spring 2015

* “Decreases in adolescent weekly alcohol use in Europe and North America: evidence from 28 countries from 2002 to 2010” Published by Oxford University Press on behalf of the European Public Health Association. Eur J Public Health. 2015 Apr;25 Suppl 2:69-72. doi: 10.1093/eurpub/ckv031.

The authors based on sociological research “Health Behaviour in School-Aged Children”. It was noted that even in the Eastern countries, where in 2002-2006 there was a steady growth trend of alcohol consumption by school children, in 2006-2010 the weekly consumption of alcohol declined from … to …%.

Without exaggeration, from the early 90-ies and till nearly 2006, beer was the youth’s iconic drink. Then the media changed their attitude to it from cool to negative. Such position to alcohol much differs from the older generation’s culture that set a high value on alcohol as a tool to secure the social status. Currently, the process of beer consumption plays a much smaller role in bridge building and pastime of young people.

Most of opinion leaders among the youth pursue an active life style; fitness and social welfare are valued by them. Consuming big amounts of beer (and alcohol in general) is considered not reasonable, as presently it doesn’t promote but stand in the way to success. The alcohol as a stimulator has got many alternatives now – from computer games to extreme sports. Teenagers’ entertainments often require a high concentration level which is not possible if much alcohol is consumed.

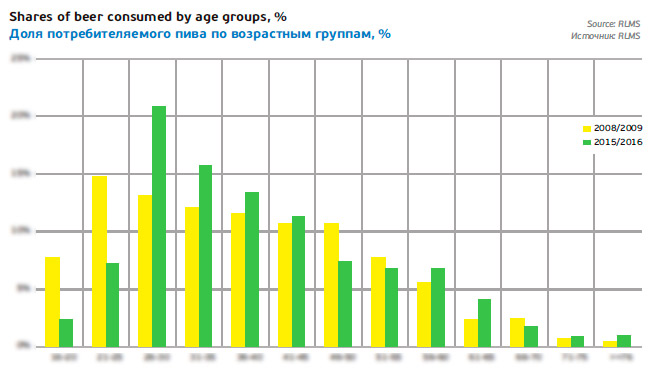

The reduction of the young population and their refuse of alcohol played a big part in the allocation of consumed beer by the age groups. In 2008, the consumption peak was in the group … year old, and in 2015 consumers’ group aged … is prominent. Besides, back in 2008, the group of … year old consumers also had a considerable weight, but nowadays the teenagers drink several-fold less beer.

Hipsters, who in the generation of the 90-ies form the consumers’ trends, have also influenced the culture of beer consuming. Their contribution is the world’s boom of craft brewing. Now less beer is consumed, it is drunk not so often and it should be an increasingly special beer. That is why the popularity decline of mass youth’s brands can be associated not only with the demographics.

Born in the 80-ies

Due to the loyalty lack for beer in young people, the consumers’ core has grown notably older, and it is now based on the people born in the 80-ies. They were those who made the biggest contribution in the beer market development. This generation still love beer and continue consuming one third of the general amount consumed. And there are several reasons for this.

In the first place, people born at the dawn of the “developed socialism” became the most numerous group who is massively climbing the age pyramid.

In the first place, people born at the dawn of the “developed socialism” became the most numerous group who is massively climbing the age pyramid.

In the second place, the share of beer consumers in this generation totaled …% at the poll time, while the average is …%. Though by 2015/2016, the share reduced by … p.p., but according to the same poll the estimated per capita consumption has grown by …%. By the way this growth is also observed in the younger consumers’ group and opposes the dynamics of the older groups.

So, why do people aged 26-36 love beer so much now? That is so because for the early millenials beer has been a part of their life. Due to its high availability and low price as well as lack of other “light” psychostimulating products, beer was one of the main drinks of the Russian youth in the 90-ies. Its status was supported by the ads and popular TV hits, dedicated to beer.

Born in the 70-ies

Generation P who grew adult at the times of difficult economic reforms of the 90-ies was choosing not only Pepsi. The soviet society transformation into a society of consumption implicated a special approach to beer, which became a status drink after the deficit and anti-alcohol company. It is known that in the 90-ies, the alcohol played a key role in social relations. Besides, informal cultures, that enjoyed their flush in the late 80-ies and early 90-ies also made a contribution into the positive image of beer.

As a result, people born in the 70-ies had a positive attitude to beer. Nowadays, due to their age and marital status they are not the most active beer consumers. Quite possibly, the share of beer drinkers is gradually decreasing. Yet, this group’s contribution into the total volume of the consumed beer is still high, due to continued growth of per capita consumption. That is, those people who went on drinking beer drank more of it. And not before 2015-2016, did the polls registered a slight decline of the specific volumes.

Conclusion

Conclusion

The analysis of beer consumption of different generations of the Russians shows that the beer market has probably approached the equilibrium point. At least, between 2015 and 2016, we are observing a consumption growth for only few young consumers. The general negative attitude to beer among the youth at the present moment is partially compensated by the increase in the number of new consumers. The dwindling stream of people born in the 90-ies is getting reinforced by the high wave of those born in the noughties. This is a new process, which will improve the previous years’ situation when the youth’s lower interest for beer was coupled with the demographic pit effect. But now it is too early to predict that the expected slow growth of the beer consumption by young people will fully compensate for the decline in the older generations’ consumption.

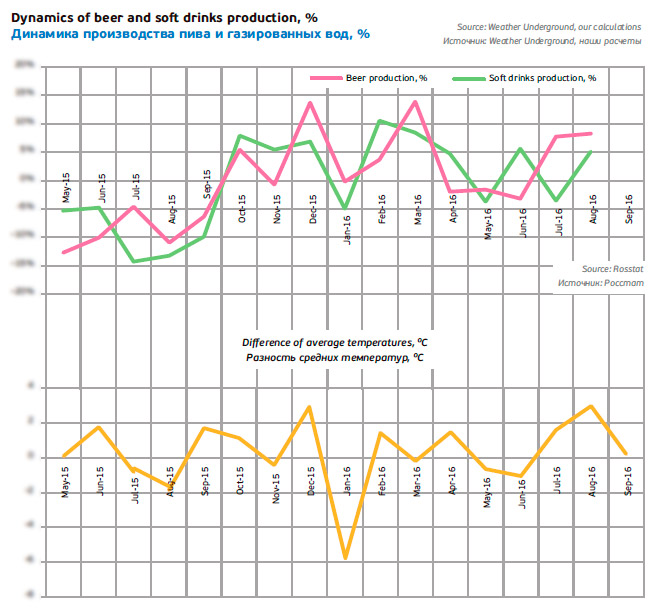

Hot season

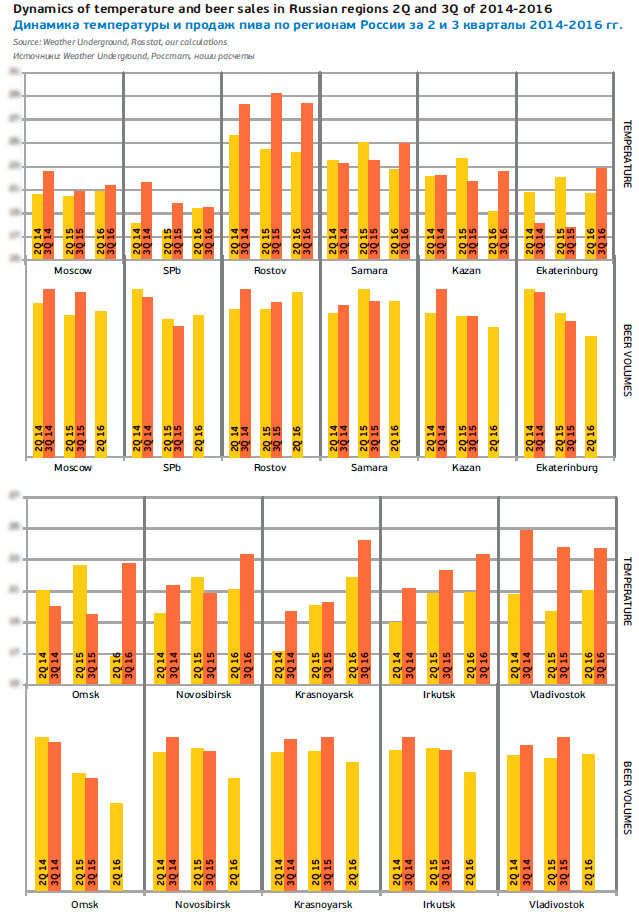

Analyzing the data on weather for 2014-2016 we can see a direct connection between the weather fluctuations and beer sales. This season, the weather was if not the decisive than an important factor of the market.

In order to estimate the weather in Russia’s regions, archive data of weather monitoring in 11 cities were used *. Basing on daily observation the average monthly temperature and its deviations were calculated both by cities and in the average in Russia.

* Moscow, Saint-Petersburg, Krasnoyarsk, Irkutsk, Vladivostok, Omsk, Kazan, Novosibirsk, Samara, Rostov-on-Don, and Yekaterinburg.

In summer 2015, it was rather cool. Certainly, an …% production decline in 2015 cannot be explained by the … degree average temperature decrease. But it should be kept in mind that in Moscow and Saint Petersburg (major cities consuming beer) the temperature in July went … degrees down. Besides there was a considerable temperature fall in other cities with a million-plus population namely, Omsk, Yekaterinburg, and Samara.

At the moment of the article preparation, the official sales data for QII2016 are known. Yet, in that period the average temperature was even lower than in 2015, except for Moscow and Saint Petersburg, where the low–base effect came to force and beer sales increased.

From now forward, due to the low base effect, one could expect a sales increase, but summer of 2016 was hot anyway. The Russian average temperature in August grew by … degrees, and the beer volumes did not take long to follow them up. Kazan, Samara, and Yekaterinburg had a particularly hot summer, with the average temperature … degrees higher against 2015. In Moscow the temperature was also higher but not that much. Apparently it was these regions that provided the beer volume increase. Early autumn was not so kind to brewers especially in Moscow and Saint Petersburg, where it was cool.

For the first time since 2008, we can observe such a positive weather impact on beer production. By the way, the sales dynamics of non-alcoholic drinks, which is more dependent on the weather, also grew considerably in August amounting to …%.

To get the full version of this article propose you to buy it ($40) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.