Unless you are a modern day Rip Van Winkle and have been asleep for the last 20 years, you know that there is a revolution going on in American beer. Americans are migrating to more distinctive, flavorful and carefully made products in many food and beverage segments (e.g. bread, wine, ice cream, coffee), and it is no different in beer. This is evident in craft beer’s unprecedented gains in share in recent years.

Since 2001, craft beer has grown at a compound annual growth rate (CAGR) of 7.9 percent, whereas imports have grown at an annual rate of 1.3 percent. and domestics have declined at a rate of .7 percent. Craft has even accelerated in the last five years to an annual rate of 10.1 percent while both domestics and imports have slowed [see Exhibit 1].

Exhibit 1

| Barrels | Domestic | Import | Craft |

| 5 Yr CAGR | -1.1% | -3.2% | 10.1% |

| 10 Yr CAGR | -0.7% | 1.3% | 7.9% |

| Market Share ‘01 | 86.5% | 10.8% | 2.6% |

| Market Share ‘11 | 80.7% | 13.7% | 5.7% |

Sources: Beer Institute, Brewers Almanac

The Power of the Millennials

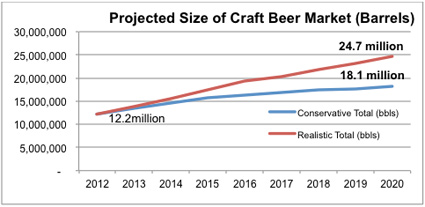

Many industry analysts project that these trends will continue for some time. I believe that the craft category will grow to roughly 25 million barrels by 2020. Craft drinking Millennials outnumber their older Gen X counterparts two to one.1

According to a March issue of Time Magazine, approximately 10,000 Millennials turn 21 every day in America. If the consumption of craft beer remains flat per drinker, the increase in the craft drinking population alone will grow craft to 18 million barrels by 2020; with 2.5 million of the 6 million incremental barrels coming from Millennials.

Craft’s share of Millennials total beer consumption, however, has increased over the years. Last year, for example, 33 percent of Millennials drank more craft than in the previous year as well as 18 percent of those belonging to other generations.2

If consumption of craft amongst all generations continues to increase at modest rates (4 percent per annum), the category will grow to 25 million barrels by 2020. I feel this is the more realistic projection [see Exhibit 2].

Exhibit 2

Pressures from Big Beer

However, in spite of the groundswell of consumer interest in craft beer, there are powerful forces working against the interests of most breweries that make up the category. These forces are primarily the big foreign-owned corporate breweries that see craft as encroaching on their interests with distributors, retailers and consumers.

The duopoly players (ABI and SAB/Miller) who control 77 percent of the U.S. beer market are working to beat down competition from craft brands. In pursuit of this objective they do four things:

- Pressure the independent distributor tier to focus on their own products to the exclusion of others (e.g., ABI’s 100 percent share of mind and anchor distributor programs).

- Create faux craft brands (e.g., Blue Moon and Shock Top).

- Buy and assimilate craft brands and exert strong pressure on craft at retail—sometimes through their positions as category captains. At the retail tier, for example, they assert to chain buyers that there are too many craft SKUs and that craft is over-spaced.

- They have asserted that many crafts should be placed on the warm shelf along with wine and merchandised by style rather than by brand.3

The Brewers Association (BA) Market Development Committee,which is represented by eleven craft brewers, has taken a deep interest in fighting the assertions that craft is over-spaced in the chains and has, therefore, commissioned this article.

Craft is Under-Spaced

The punch line of the following paragraphs is that craft is under-spaced and retailers should strongly resist moving craft brands to the warm shelf.

We reached our conclusion by analyzing all of the major chains individually in five key regions: Northern California, Southern California, Chicago Area, Northwest and the Northeast. For each chain we looked at all the segments (craft, premium, super premium, sub-premium, imports, PAB and cider) and measured the physical space allocated to them in each of their account classifications (e.g., affluent, expanded affluent, ethnic, mainstream).

We then juxtaposed the allocated space with the gross profit (GP)4, incremental GP (meaning the change in GP vs. a year ago) and expected incremental GP in 20165 generated by each of these segments.

Within each chain, we weighted this data by their own account classifications and then rolled this all up to the regional level by weighting each chain according to their relative volume. The major chains in these regions represent between 42 -78 percent of off-trade beer volume of their respective regions.

Share of Space Vs. Gross Profit

The data in Exhibit 3 shows that in terms of share of space vs. current share of gross profit, craft is under-spaced in Northern California, the Northwest and the Chicago Area, and is appropriately spaced in the Northeast. It is over-spaced based on this metric in Southern California. In terms of domestic beer, super premiums are over-spaced in three of five regions and premiums are slightly under-spaced in three of five regions.6

Share of GP vs. share of space, however, is often not the right metric for retailers to use when making space decisions, especially when the craft category is growing so rapidly. While craft is over-spaced in Southern California according to that metric, if we compare the amount of incremental GP it generates, it is actually under-spaced there, too. In terms of incremental GP, craft performs far better than all other segments.

On this dimension, craft is the most powerful category adding over 60 percent of the incremental GP in three of the five markets. This performance by craft far outstrips all the other segments. Conversely, on this measure imports are weak and premiums are very weak—actually generating significantly less GP for retailers in 2012 than in 2011.

In Chicago, for example, if we look at the change in retailer GP by adding the declining and the growing segments together, premiums contribute a whopping negative 93 percent of the change in GP! No doubt, this is a difficult concept to get your mind around. Simply put, it’s BAD; they are reducing GP for the retailers! [See Exhibit 4].

It is important to note that in any market where craft is in its early stages of development, its share of space will always exceed its share of GP. This is because there can be no growth without it first being on the shelf. As craft grows, its share of GP will match, then exceed, its share of space. Following this logic, look in Exhibit 3 at the amount of GP that craft will generate in 2016 assuming the segments continue to grow at their current pace. The ratio of craft’s share of GP to its share of space in 2016 is far better than any other segment [see Exhibit 5].

Exhibit 3

Quantities and Organization

While this post demonstrates that craft is under-spaced in off-premise chains, what about the number of craft SKUs that should occupy the shelf space allocated to craft? Secondly, how should the sets be merchandised?

The first of these questions is difficult and I’ll not attempt to answer here. I will say that this will vary according to the strategy of the particular chain. Regarding the second question, I share the position of the BA Market Development Committee, which was that expressed by Jessica Jones of Ninkasi Brewery in the last BA Insider. She laid out a compelling case that chain sets should be organized by brand versus by style for various reasons, including that it reduces confusion for shoppers and is far more attractive to them. Consumers come to trust certain brands and don’t want to hunt for them while shopping for a particular style.

Cooler Vs. Warm Shelf

Finally, contrary to the stance being pushed by the large corporate beer companies, retailers should avoid moving crafts from the cooler to the warm shelf. In contrast to mass-produced, domestic lagers, craft beers tend to contain more high-quality and expensive ingredients (e.g., aroma hops and two row barley) and are largely not pasteurized. Given this, their flavor deteriorates faster at warm temperatures than those of pasteurized macro-lagers (see Exhibit 6).

Retailers should consider dedicating more refrigerated space for craft brands so their customers have every opportunity to enjoy the flavor quality of American craft beer. Do the chains really need to merchandise all the myriad of package and container sizes of the same domestic lagers in the cold box? Surely not! If anything they should be moved to the warm shelf.

Exhibit 6

In summary, while the future should be very bright for craft beer in the U.S. given changing consumer preferences, the powerful duopoly is working hard to undermine this movement. While they are applying pressure on many fronts, their assertions that craft is over spaced in the chains are plainly wrong. Craft is under-spaced!

Photo © Todd Dwyer via Flickr CC

1. Mintel Group, Craft Beer Report US, November 2012

2. Mintel, 2012

3. ABI’s Nov 2012 Sales and Marketing Communications meeting in Chicago; and various discussions with chain buyers and distributors

4. Calculated assuming GP margins: craft=28%; imports=25%; premium=18%; super premium 25%; sub-premium=20%; PAB/cider=28%

5. To get 2016 GP we assume that the segments continue trending at their current rates

6. Nor Cal: 4 chains = 78% beer 77% craft; So Cal: 4 chains = 62% b/81%c; Chicago: 4 chains = 69%b/76%c; Northeast: 6 chains = 42%b/43%c; Northwest: 4 chains = 73%b/71%c

Prior to the four years he has been at Lagunitas Brewing Co, Todd Stevenson held various senior roles in marketing, strategy and general management in his 14 years at Diageo in the U.S., Japan and South Africa. In addition, Todd ran the global marketing for Nokia’s Lifestyle Division, based in London. He holds an MBA from Dartmouth and a BA from Tufts University.

Prior to the four years he has been at Lagunitas Brewing Co, Todd Stevenson held various senior roles in marketing, strategy and general management in his 14 years at Diageo in the U.S., Japan and South Africa. In addition, Todd ran the global marketing for Nokia’s Lifestyle Division, based in London. He holds an MBA from Dartmouth and a BA from Tufts University.

Brewers Association