Anheuser-Busch InBev company has disclosed 1Q2016 performance results and has shared expectations for the further year.

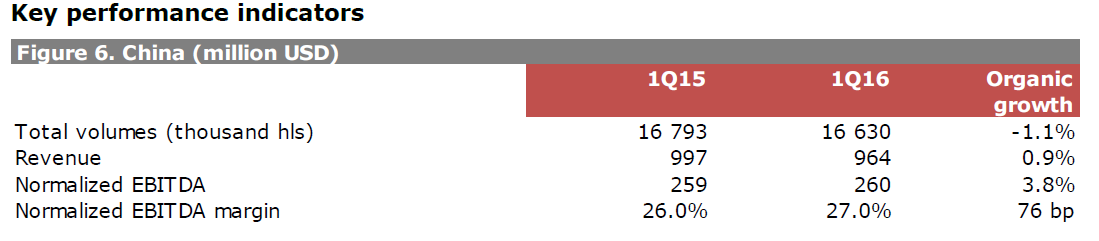

According to the quarter report, industry volumes in China remain under pressure. However, AB InBev volumes continue to perform ahead of the industry, declining by 1.1% in the quarter, helped by the focus on the Core Plus, Premium and Super Premium segments.

According to the report, China beer industry volumes declined by approximately 4% in the quarter, due to economic headwinds. Company beer volumes faced a tough comparable, declining by 1.1% compared to a growth of 4.7% in 1Q15. AB InBev market share increased by approximately 45 bps, reaching an average of 19.0% in the quarter.

China EBITDA grew by 3.8% and EBITDA margin improved by 76 bps to 27.0% in 1Q16.

In 2016 financial year, company’s experts expect industry volumes to remain under pressure. Meanwhile AB InBev expects its own volumes to perform better than the industry, driven by the premium and super premium brands.

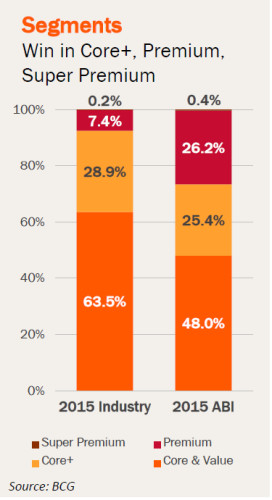

AB InBev management continues to believe the Core Plus, Premium and Super Premium segments have the greatest long term growth potential in the industry. Company’s brands in these segments represent more than 50% of their total China volumes, and are well positioned, with strong brand health metrics.

Revenue per hl grew by 2.1% in the quarter, with the benefit of favorable brand mix being partly offset by unfavorable regional mix driven by poor weather and industry weakness, particularly in the south and east of the country.