The standard line when it comes to Japanese consumer companies making acquisitions overseas is that they’re trying to escape the demographic decline at home. So what to make of Asahi’s reported interest in eastern Europe?

The Super Dry brewer may spend as much as 5 billion pounds ($7.2 billion) buying SABMiller’s brands in the Czech Republic, Hungary, Poland, Romania and Slovakia, London’s Sunday Times reported, without saying where it got the information.

That’s a lot of money to spend in one of the few regions whose demographics look even worse than Japan’s.

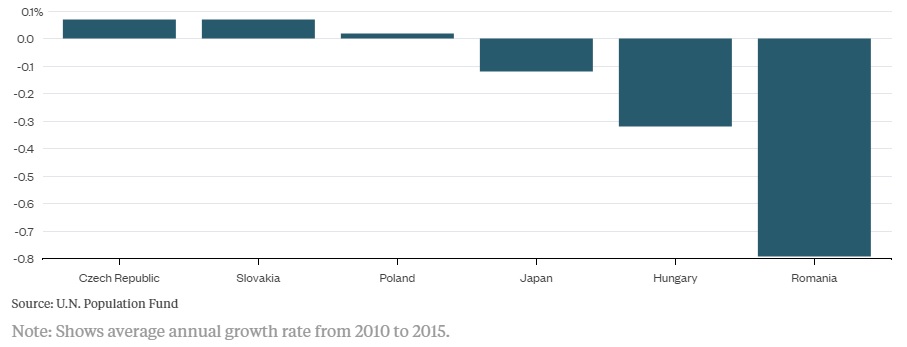

That Sinking Feeling

Japan’s negative population growth rate doesn’t look so bad next to some central and eastern European countries

Beer is mostly drunk by workers winding down after a hard day, so it makes sense to see the brewery trade as a play on population growth. Exposure to thirsty African beer markets is driving Anheuser-Busch InBev’s $107 billion takeover of SABMiller, the deal that those eastern European brands are being spun out of.

But if Japan’s 0.12 percent-a-year rate of population decline looks worrying, check out Hungary, whose population is falling at 0.32 percent. That’s not even the worst among SABMiller’s Eastern Europe assets: Among countries with more than five million residents, only Syria posted a more rapid rate of decline from 2010 to 2015 than Romania’s 0.79 percent.

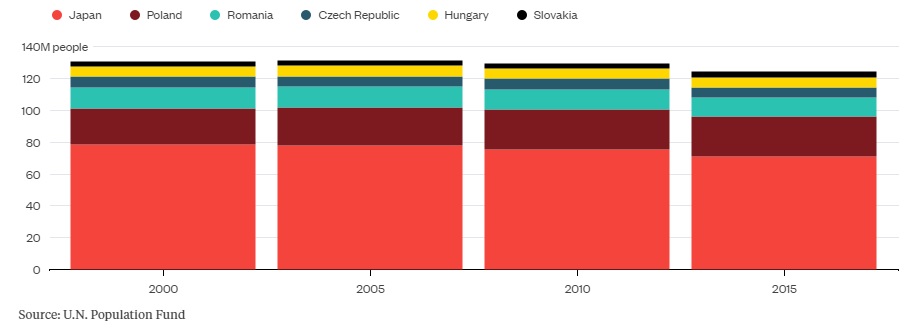

Populate or Perish

Japan’s working-age population is declining. Those in Eastern Europe are barely growing.

Asahi’s President Akiyoshi Koji told Reuters last month that the company wasn’t interested in buying SABMiller’s eastern European assets, so shareholders should hope the latest report is wide of the mark. Even so, the fact such a deal could be credible is an indication of how incoherent Asahi’s strategy has become.

Brewers wanting to maintain growth have two choices – either expand into high-growth niches at home, or find emerging economies where beer drinking is set to grow. Asahi has already passed up opportunities in the former category, ignoring the burgeoning female workforce targeted by Kirin’s cider offerings and Suntory’s whisky highballs.

It doesn’t look much better in developing markets, where most of the obvious candidates are already taken. The AB Inbev-SABMiller behemoth has a lock on swathes of Africa and Latin America; Heineken has strategic stakes in the owners of Nigeria’s Star lager, Indonesia’s Bintang and India’s Kingfisher; and Kirin has beaten its domestic rival to stakes in Tsingtao and San Miguel, the No. 2 and No. 1 brands in China and the Philippines respectively.

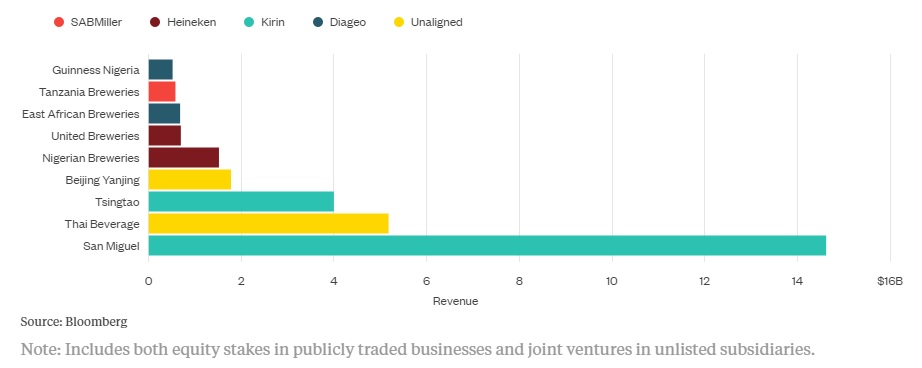

Last Orders

Of the nine listed brewers in emerging Asia and Africa with more than $500 million in annual sales, all but two have struck alliances with other big beverage companies

What’s left? Asia Brewery, the beverage arm of Philippine billionaire Lucio Tan’s LT Group, signed a distribution deal for Super Dry three years ago and was openly angling for a deeper partnership. Its premium-focused portfolio would have made a decent fit with Asahi but the overtures went nowhere and last month it instead formed a joint venture with, you guessed it, Heineken.

Thai Beverage is probably too big for Asahi to take on, except in a merger of equals that would risk controlling shareholder Charoen Sirivadhanabhakdi, a renowned tough negotiator, holding all the chips. (Its five-year relationship with Carlsberg ended in lawsuits and bitter disputes over assets.)

Beijing Yanjing Brewery, owner of China’s No. 3 beer brand, put a 20 percent stake up for sale last year but, as the low-ball price paid for SABMiller’s stake in best-seller Snow Beer indicated, that country’s drinkers aren’t much more appealing to investors than Japan’s.

One obvious opportunity is left: Diageo. The London-based firm ought to spin off Guinness and its other brewing assets, Gadfly’s Brooke Sutherland argued, a business that Bernstein estimates could be worth 7.4 billion pounds.

Even if Diageo isn’t prepared to say goodbye, a joint venture with Asahi would give the Japanese company a brand with enviable positions in both Europe and Africa, while allowing the U.K. group to focus more on its role as the world’s biggest publicly traded distiller. That would seem a much better use of Asahi’s money than a foray in eastern Europe.