Carlsberg Group ranks fifth by the sales volumes in China. The company is referred to as King of the West as it owns the “controlling stake” of the beer market on huge but sparsely-populated territories of the Western China.

In 2015, the national sales of the company reduced by 2% and in our view amount to 21 mln hl. And in the first half of 2016, Carlsberg Group volumes reduced by 3% that is two times better than the industry. Adjusting for the brewery closures, volumes would have declined by an estimated 1%.

In 2015, the national sales of the company reduced by 2% and in our view amount to 21 mln hl. And in the first half of 2016, Carlsberg Group volumes reduced by 3% that is two times better than the industry. Adjusting for the brewery closures, volumes would have declined by an estimated 1%.

Volumes decline is in the first place connected to the company’s efforts to raise profitability by closing a host of ineffective breweries and improving products’ mix. That is why Carlsberg Group strategy includes revision of production effectiveness and SKU profitability of several dozens of regional brands. The comparatively good performance is associated with a dynamic growth of Tuborg brand sales.

History of acquisitions

Carlsberg Group’s focusing on the West China markets though being the choice of the company’s management, also resulted from a number of problems which are already described in management textbooks. Originally East and West coast of China was the top priority for Carlsberg Group.

Carlsberg Group’s focusing on the West China markets though being the choice of the company’s management, also resulted from a number of problems which are already described in management textbooks. Originally East and West coast of China was the top priority for Carlsberg Group.

The company commenced an active expansion as early in 1981 as it launched Carlsberg Brewery Hong Kong and started a licensed production there, including beer manufacturing for export to mainland China. In 1995, the company entered the major markets of China, having acquired Huizhou Brewery in Guangdong Province and invested around US$30 mln Shanghai Brewery, which started production in 1998.

In 2000 Carlsberg Group diverged from the steady development way. The company sold out nearly 75% of Shanghai Brewery stake to its competitor Tsingtao and went in for a big deal which brought the company to the markets of the key countries in the region.

In 2001 most of Carlsberg Breweries’ activities in Asia have been transferred to the joint-venture Carlsberg Asia Holding Ltd. (CAL), of which 50% is held by Carlsberg Group and 50% is held by the Asian Chang Beverage Company (future ThaiBev).

Yet, it was not an easy win. Simultaneously with Carlsberg Group, by complete or partial purchase of local manufacturers (such as for example Guangzhou Zhuajiang Brewery) the southern market got into the focus of other national and transnational companies which were not willing to give it up to competitors.

Unimplemented plans contributed much into disappointment in the partnership and mutual claims between companies. In 2003, CAL business was agreed to divide. However, Carlsberg Group lost $120 mln, which had to be paid off as compensation.

Probably, Carlsberg Group management estimated the competition degree on the coastal markets and considered the entrance fee to be unfairly high. At the same time, very low beer consumption and “catching up” economy development in the West of China made that region very promising for investors. The financially exhausted company also needed the low price of the local assets and hoped for their rapid rate of return due to the virtually monopoly position on the western market.

That started the massive aquisition of breweries. In 2003, Carlsberg acquired the Kunming and Dali breweries in Yunnan province. In 2004, Carlsberg 1) became major shareholder in Lhasa Brewery in Tibet, 2) became major shareholder in Lanzhou Huanghe (Yellow River Brewery) with three breweries and a malthouse in Gansu, 3) acquires 34.5% shareholding in Wusu Brewery (Xinjiang) and 4) together with local partners invests in greenfield brewery in Qinghai.

That started the massive aquisition of breweries. In 2003, Carlsberg acquired the Kunming and Dali breweries in Yunnan province. In 2004, Carlsberg 1) became major shareholder in Lhasa Brewery in Tibet, 2) became major shareholder in Lanzhou Huanghe (Yellow River Brewery) with three breweries and a malthouse in Gansu, 3) acquires 34.5% shareholding in Wusu Brewery (Xinjiang) and 4) together with local partners invests in greenfield brewery in Qinghai.

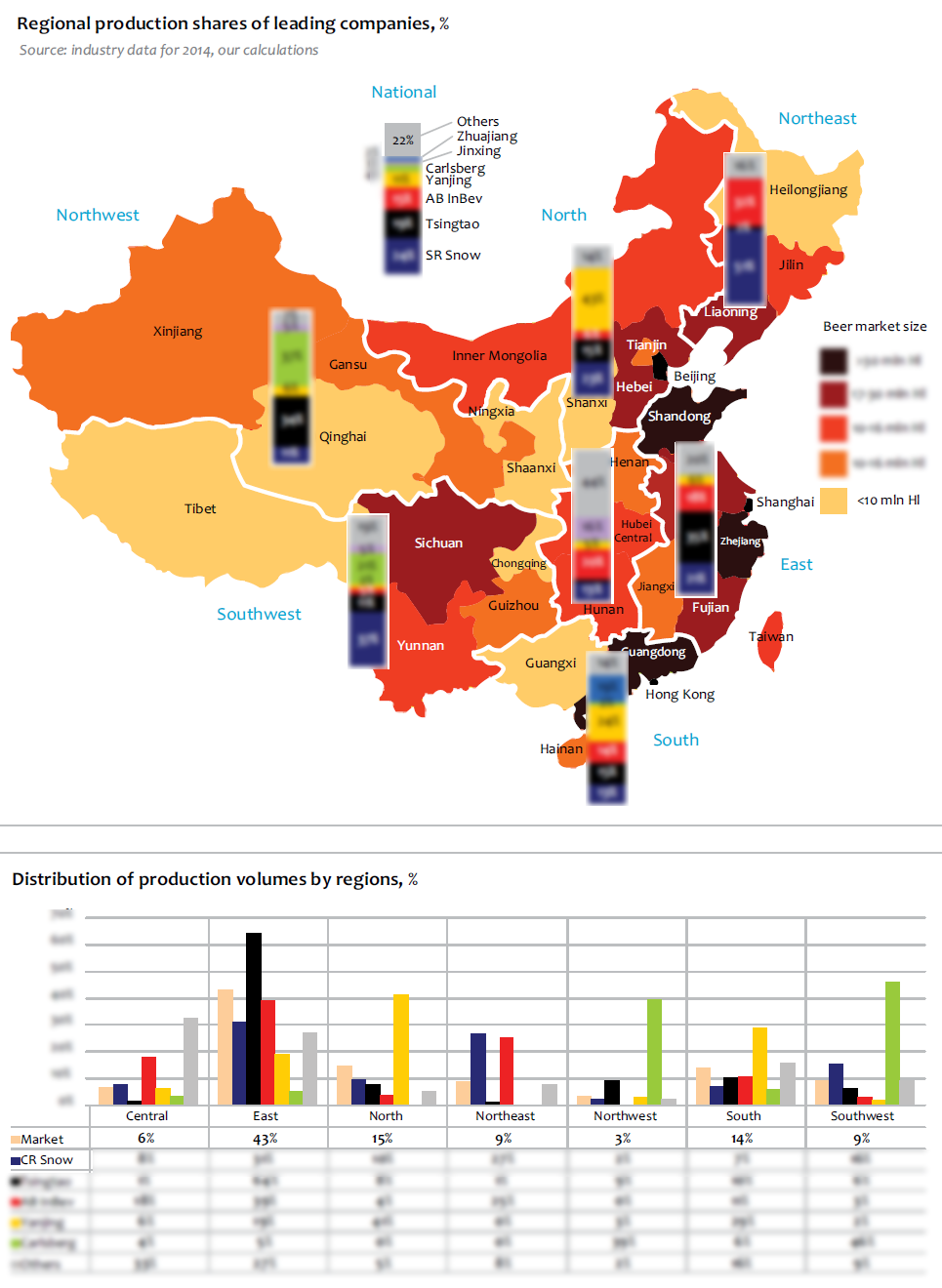

In several years, Carlsberg Group co-owned Chongqing Brewery, which currently sells nearly a half on the company’s beer volumes on the Chinese markets. Chongqing Brewery has nearly 20 trade and production subsidiaries located in Chongqing, Sichuan, Hunan, Guangxi, Guizhou, Zhejiang, and Anhui. In 2011 Carlsberg increased its share to 30% and to 60% in 2016. Other shares belong to small shareholders with less than 3% stake.

Performance of branches

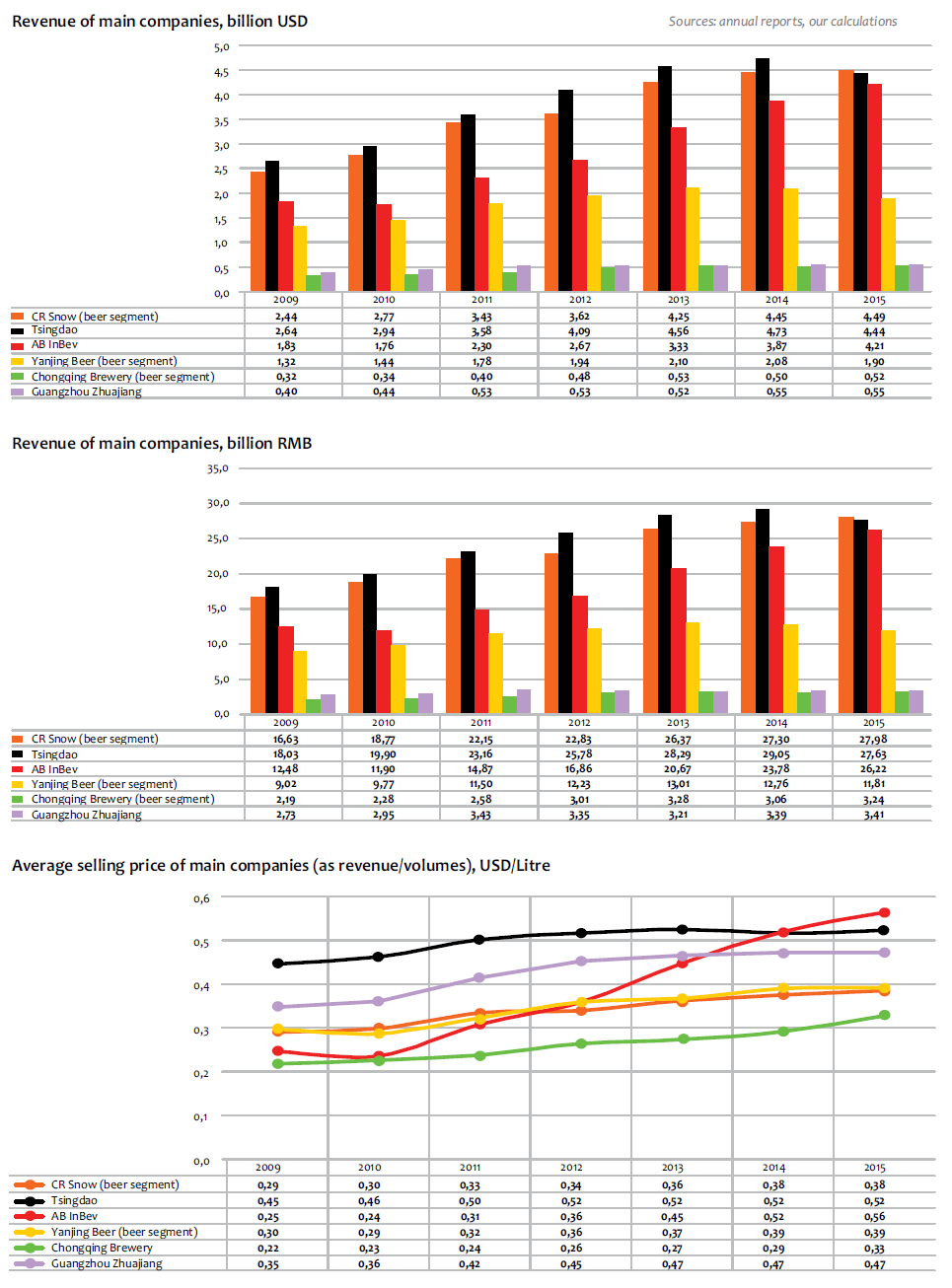

Though in the report for 2015, Carlsberg Group announced sales rise in city of Chongqing, beer production by Chongqing Brewery was on the contrary cut down. According to the report, in 2015 Chongqing Brewery reduced its output by 6% to 9.895 mln hl. Meanwhile, in 2015, the company increased the revenue by 5% to 3.324 bln yuan.

Though in the report for 2015, Carlsberg Group announced sales rise in city of Chongqing, beer production by Chongqing Brewery was on the contrary cut down. According to the report, in 2015 Chongqing Brewery reduced its output by 6% to 9.895 mln hl. Meanwhile, in 2015, the company increased the revenue by 5% to 3.324 bln yuan.

Despite the decline, year 2015 can be called a transition period from decline to stabilization as in 2014 the output dynamics of Chongqing Brewery was much worse (-12.85%). Such performance made Carlsberg Group take decisive steps.

In 2016 number of SKU was cut and 6 beer breweries, half of which belonged to Chongqing Brewery, were closed. There was a shutdown of unprofitable breweries located close to each other, and operating on old equipment. By the way, in 2016 two half-completed production sites were sold off.

Another big brewery of the company, Lanzhou Huanghe (Yellow River Brewery) in Gansu showed not a particular good performance by the end of 2015. Revenues from beer production fell by 15.6% to 0.44 billion yuan. Given this figure and the regional statistics, the volumes were also decreasing by double-digit rates, having went lower than 4 mln hl. The revenues from malt sales fell by 26.3% to 0.11 billion yuan due to higher prices for raw materials.

Wusu Brewery (Urumqi, Xinjiang) is a joint venture between Carlsberg Group and Xinjiang Hops Company. Recently, the company has been faced with fierce competition from international companies. However, Xinjiang Hops Company informed of sales rise in 2015 by 7.2% to 3.251 mln hl, and the beer sales revenues increased by 8% to 1.131 bln yuan.

Wusu Brewery (Urumqi, Xinjiang) is a joint venture between Carlsberg Group and Xinjiang Hops Company. Recently, the company has been faced with fierce competition from international companies. However, Xinjiang Hops Company informed of sales rise in 2015 by 7.2% to 3.251 mln hl, and the beer sales revenues increased by 8% to 1.131 bln yuan.

Besides, judging by the regional statistics data, sales of Carlsberg Group in Yunnan province could have experienced some growth.

Brands’ performance

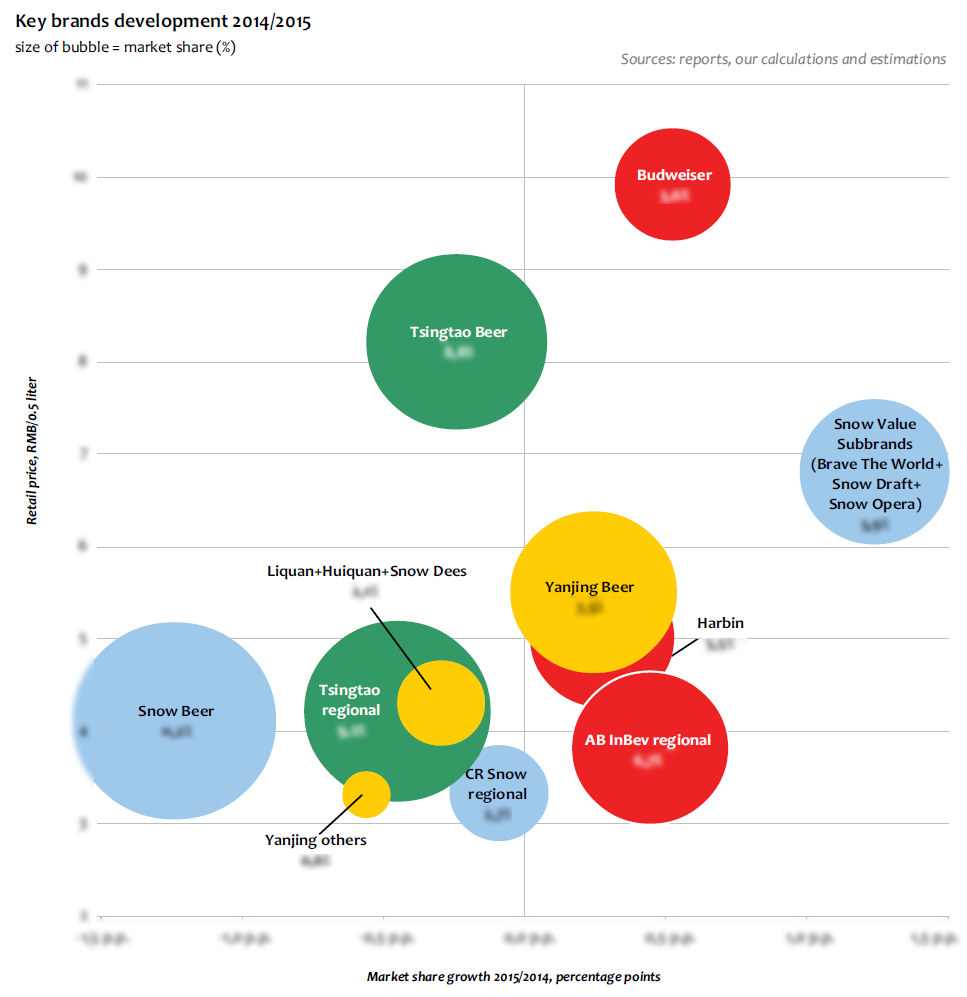

During conference call on the performance of 1H2016 Carlsberg President and CEO, Cees ‘t Hart said: “We remain optimistic on the value opportunities as mix premiumization continues fast, particularly as a growing middle class starts trading up into international premium brands. These now deliver one-third of our China revenues, led by Tuborg. It is now a clear number two international premium brand, more than twice the size of the next competitor. Super premium specialty sales also increased at over 50%, led by 1664 Blanc. The cost reductions and premium growth led to a strong GPaL margin improvement that, we believe, we can continue”.

Like many other companies, Carlsberg Group gets more than half of its sales volumes from economy regional brands, though the average price per beer liter is higher compared to competitors’. Here remoteness of the western markets and domination on them come into play.

Big regional brands, namely, ChongQing and Shancheng 1958 are popular mainly in Chongqing and its neighboring areas. Recently both of them have changed the names and package, and by essence we can say that Shancheng is a subbrand of ChongQing. Probably for this reason, Chongqing Brewery report for 2015 cites a 363% volume growth of ChongQing to 4.68 mln hl. and Shancheng volumes decline by 63% to 2.59 mln hl. Their net volume fell by 13% to 7.37 mln hl.

Big regional brands, namely, ChongQing and Shancheng 1958 are popular mainly in Chongqing and its neighboring areas. Recently both of them have changed the names and package, and by essence we can say that Shancheng is a subbrand of ChongQing. Probably for this reason, Chongqing Brewery report for 2015 cites a 363% volume growth of ChongQing to 4.68 mln hl. and Shancheng volumes decline by 63% to 2.59 mln hl. Their net volume fell by 13% to 7.37 mln hl.

Premium brand Carlsberg has been brewed in China for 20 years. Its sorts, despite the localization were never able to secure the output volumes stability and improve the price mix of the company. For example, Chongqing Brewery according to the report cut the sales of Carlsberg brand. The decline amounted to 13% to 0.173 mln hl. Such dynamics can result from reallocation of output depending on the place of consumption, or from the competition growth.

Carlsberg Group attributes the decrease in volumes of the regional brands to the sharp increase of brand Tuborg. Chongqing Brewery increased its sales by 65% to 1.479 mln hl. As we can see, this figure coincides with the results cited at conference call of Carlsberg Group. Though the 20%* share in the sales structure was obviously achieved in 2016.

* According to 1Q2016 conference call

Tuborg was launched into the Chinese market in spring 2012. In accordance to the global positioning strategy, this brand targets youth audience. The package design also completely corresponds to the international image, that is, inclines round logo, and unusual for the Chinese market “ring-pull” cap. The distribution and the market support of the brand is provided by Chongqing Brewery according to the report.

Carlsberg Group remoteness from other outlet markets, that is, big cities in the east of China, has probably deterred the brand from getting a fast start due to high costs of transport and problems in organizing distribution. Whereas, as far as we know, the main sales channel for Tuborg was the network retail. Essentially, the fast sales growth did not start before 2014.

One of the key growth drivers for Tuborg is price positioning on the border between mainstream and premium segment. For example, at supermarkets, a 0.5 l. can of Budweiser costs about 9 yuan and the same volume of Tuborg costs 6.8 yuan. Thus, keeping attributes of international beer Tuborg distances itself from Carlsberg brand, which is also comparatively democratic in China.

One of the key growth drivers for Tuborg is price positioning on the border between mainstream and premium segment. For example, at supermarkets, a 0.5 l. can of Budweiser costs about 9 yuan and the same volume of Tuborg costs 6.8 yuan. Thus, keeping attributes of international beer Tuborg distances itself from Carlsberg brand, which is also comparatively democratic in China.

The strategy of the lower segment border blurring made it possible for the brand to grow rapidly in the Eastern Europe 10 years ago or in India 5 years ago competing with license international brands. In China the main target of Tuborg’s price attack will in our opinion be Budweiser, as the premium market leader, as well as national brands with youth positioning. Tuborg promotion is mostly based on supporting youth music events, club parties, and festivals.

To get the full article “Analysis of beer market in China” in pdf (60 pages, 65 diagrams) propose you to buy it ($45) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.