In our review we will analyze:

1) The market positions of the major companies and brands in the first half of 2020;

2) Production structure – from craft to federal breweries;

3) The market segmentation by the price and package.

In 2020, the roles of sale channels have changed especially at the draft beer market. The relations with networks have been determined by brewers’ market share fluctuations. The official production and sales have been growing despite substantial decline in Heineken, Zavod Trekhsosenskiy, Ochakovo, and key regional breweries. Instead, the retail positions of AB InBev, small brewers, import and private labels have reinforced their positions.

On the reasons for the formal growth in 2020

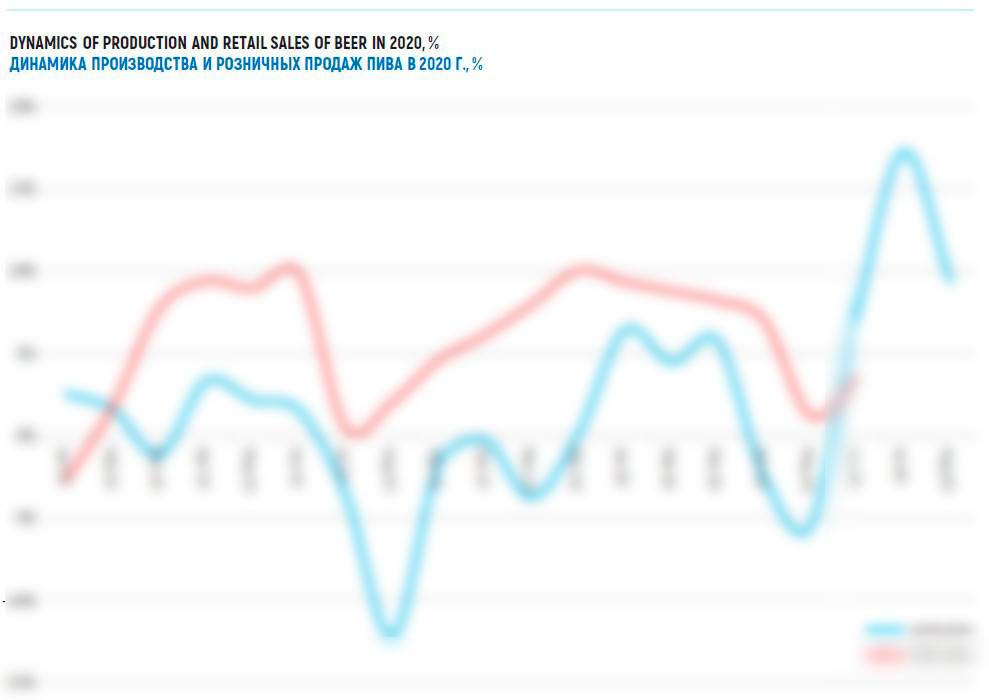

Different estimations agree on the position that the Russian beer market has not suffered from COVID-19, from the point of view of natural volumes.

Thus, in the first half of 2020, Federal Service for Alcohol Market Regulation spoke of a *.*% sales growth and Rosstat registered a *% production growth. Distributors citing retail audit data notice an unprecedented for the recent years *% beer sales growth. Besides, this dynamics coincides with the first half of 2020, as consumers and the industry experienced the worst shocks. If we speak of the high beer season performance (including July-August) the results can be even better judging by Rosstat data.

There appears a reasonable question, whether these figures reflect the actual situation on the market. Currently, many sources say that a part of sales of draft beer shops and probably of HoReCa are out of eyeshot. The Vedomosti, Kommersant and press-services of some companies straightforwardly write about it.

On the one hand, since the epidemic started these channels have suffered most of all. Self-limitations of consumers as well as introduced quarantine measures have played their part there. But special retail got a strong strike from “clean-up” by the regional authorities (find more details on it below in 2GIS statistics).

In other words, in 2020 the official growth of the brewing industry and retail sales is not necessarily connected to actual consumption increase. Possibly, in 2020 there was a redistribution of some part of draft beer into the retail. Let us keep in mind that fact, in order to better understand the market situation.

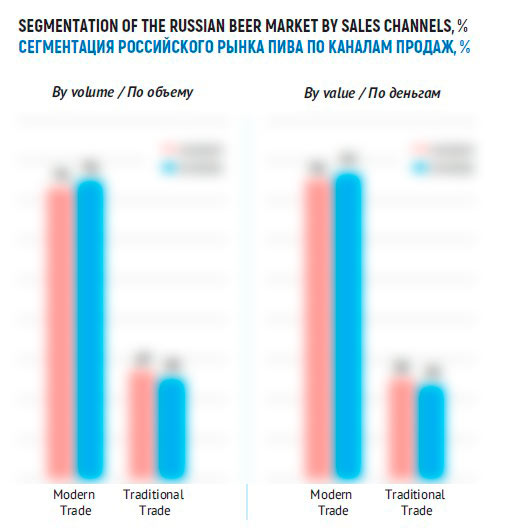

The market segmentation

In segmentation by sales channels the role of the modern trade has grown which one could expect. However, one cannot say that this process was characteristic for 2020. Rather the lineal flow of consumers got an additional impetus and the share of supermarkets went up by * p.p. to **%.

There have also been changes in the price segments.

On the one hand, consumers wanted to save money while shopping and their tastes became simpler. On the other hand, brewers were keeping their prices down and made some international brands more affordable. That is why, we can speak of the beer market polarization.

Thus, the economy segment has increased. Yet its growth resulted from many multidirectional trends.

A big contribution into the positive dynamics has been made by economy brands by AB InBev Efes and private labels. Besides the market share of Zhigulevskoe by several dozens of federal and regional producers went up from *.* to *.*%* and the average retail price for them decreased by *% to **.* RUB for a liter.

* Several sorts of Zhigulevskoe by regional producers belong to the mainstream segment.

That being said, one cannot ignore a considerable decline of “regional” beer in wide meaning of this word. On the one hand, the market share of regional brands by three market leaders has declined from *.* to *.*% (in better times their share had exceeded *%). On the other hand, in the economy retail segment a third part of medium breweries’ volumes as well as almost all output by Zavod Trekhsosrnskiy and Ochakovo that have cut the retail sales.

The share of low mainstream has decreased as many federal brands experienced decline because of the brewers’ wish to keep or even rise their retail prices (for example beer Arsenalnoe or Tri Medevedya). The growth of Stariy Melnik has been a strong factor, yet not enough to offset the general negative situation.

The comparative stability of upper mainstream could be actually connected to our data particularization. On the one hand, we considered the sum of Baltika’s brands that lost their market share as an integral whole that had lost some of its market share. On the other hand, we united sales of many local brewers who on the contrary, expanded their market share.

Besides, many Russian and licensed brands belong to upper mainstream. The share of license brands has been growing while that of Russian ones has been falling, both at federal and regional producers.

Let us note that in general not regarding the price segments the share of licensed beer by volume in the first half of 2020 increased from **.* to **.*%. Russian mass brands had been long squeezed out by foreign brands. Yet, this year the process has gained speed, probably due to check to prices for beer as its average retail price went *% down to ***.** RUB/l.

The popularity growth of foreign brands both of local and foreign origin has been the driver of the premium segment development. This segment includes two major license brands Velkopopovicky Kozel and Bud belonging to the market leader. These two brands showed a good growth in the first half of 2020. The segment growth could have been much higher if not for the share decline of marginal brands by Heineken company.

Superpremium segment has been developing rapidly due to import beer. Its popularity in the retail was a compensation of lower sales in HoReCa and at beer shops, including both foreign and craft beer.

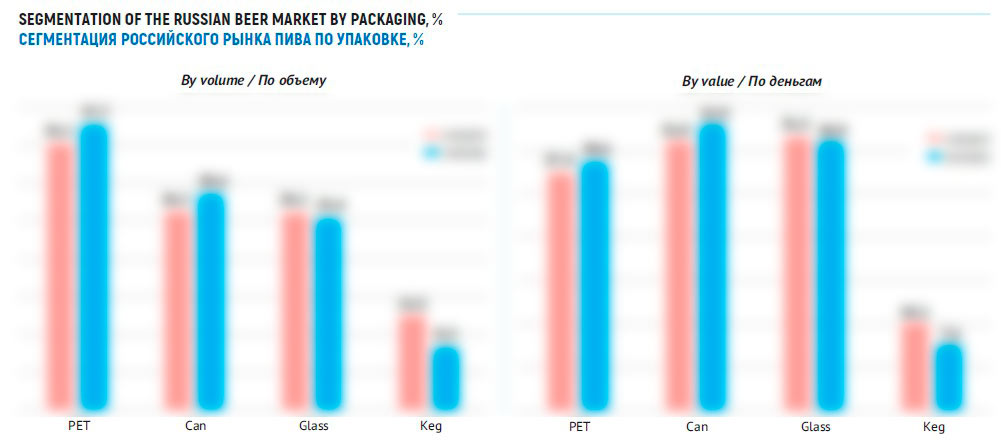

In the sales segmentation by package there have been significant changes. The reduction of keg beer sales was obviously connected to the lock down and reduction in number of beer shops. Besides, we understand that spill-over of clients to supermarkets and their wish to optimize their purchases led to a popularity spike of lighter packages – PET and cans. Glass bottle sales wend down both due to big weight and fragility of that package and because impulse shopping has become less common among Russians.

The industry structure

Before we start dealing with the competitive analysis, it would be interesting to look at the official positions of brewers with various activity scale.

Early in October 2020, Federal tax service published the data on excise payments in 2019. These figures can be translated into a beer equivalent for **** brewers and compared to the previous year. However, ** businesses of international companies are not taken into account. Yet, we took into consideration their data too.

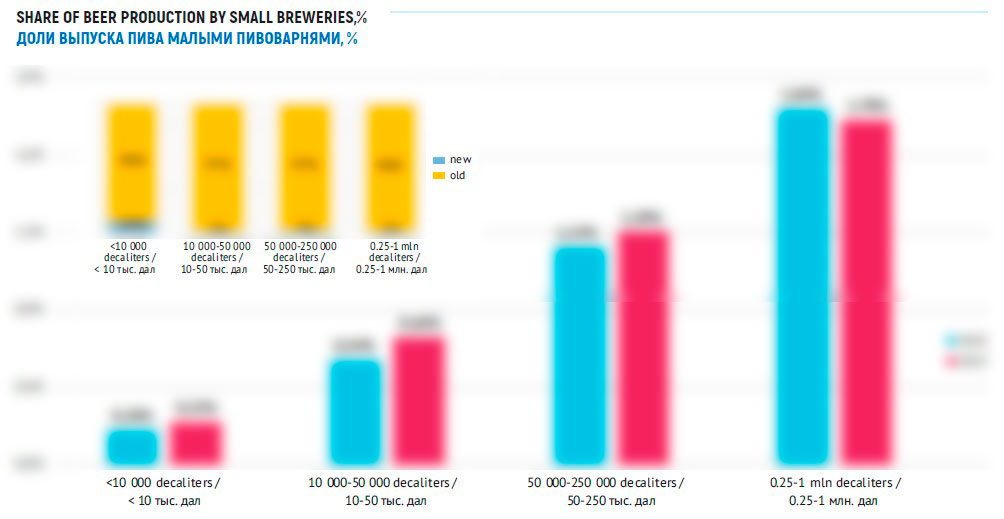

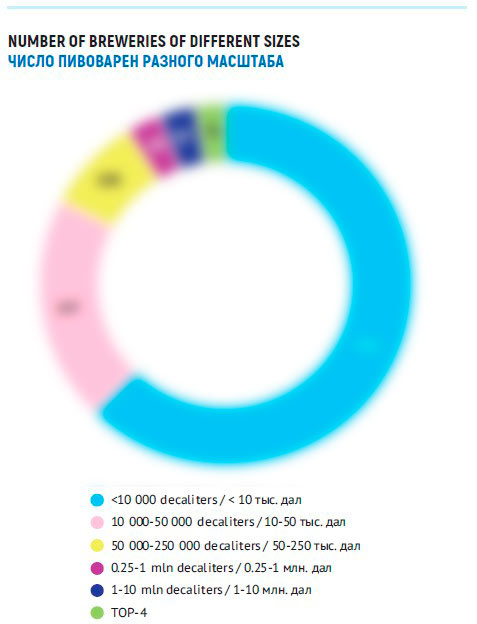

1. Microbreweries

The bulk of brewers (**%) have quite a small brewery officially outputting less than ** thousand decaliters (*.* thousand decaliters at the average). Normally these are small craft breweries belonging to enthusiasts and restaurants. They accounted for *.**% of the net output of Russian beer by the end of 2019. Over the year, the volumes of microbreweries have increased by **% and the output share has gone up by *.** p.p. Let us note that **% of the positive performance was contributed by new breweries or those who made their first accounting.

2. Minibreweries

Nearly a fifth part of Russian brewers consists of minibreweries outputting **-** thousand decaliters per year (**.* thousand decaliters at the average). Quite often, they are successful craft breweries as well breweries of well-known restaurants. That group contributed the biggest part in the net growth of small brewers, in 2019 its volumes grew by **%.

3. Industrial minibreweries

The biggest group (*.*% of the output) of small producers includes a hundred of industrial minibreweries having volumes of **-*** thousand decaliters (** thousand decaliters at the average). Most of them are located far from supercities and frequently play an important role in the local market near its populated area. Industrial minibreweries in 2019 were growing … times slower than craft breweries.

4. Major industrial minibreweries and small regional breweries.

This is a small number of region-scale producers outputting *.**-* mln decaliters (*** thousand decaliters at the average). Normally they produce draft and packed relatively cheap beer operating on the same competitive field with big companies (except for Vasileostrovskaya pivovarnia). In 2019 the output volumes of that group declined by *%, and the market share amounted to *.*%.

5. Medium and big regional breweries.

The most powerful group of independent brewers consists of ** medium regional breweries outputting from * to ** mln decaliters of beer per year*. In 2019, regional brewers declined their volumes by *%. Their share decreased by *.* p.p. to **.*%.

* We also included big brewery Tomskoe pivo as it is focused at the Siberian region.

6. Federal producers

The global threesome (AB InBev, Carlsberg, Heineken) as well as MBC, Zavod Trekhsosenskiy and Ochakovo are considered to be federal ones. These companies’ performances differ, but in general their net market share grew by * p.p. to **.*% in 2019.

In general one can say that basing on Federal Tax Service there has been reinforcement of federal brewers at the account of regional ones. However, small brewers, mainly craft ones, have also expanded their volumes. However, their market weight is still not big at all.

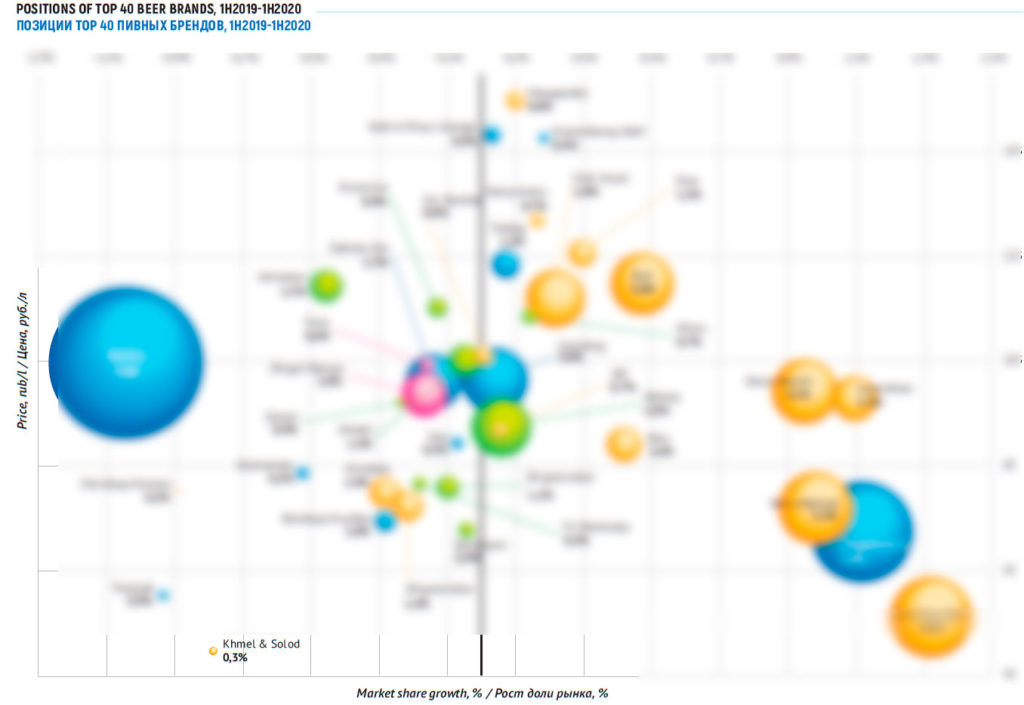

Companies and brands 2020

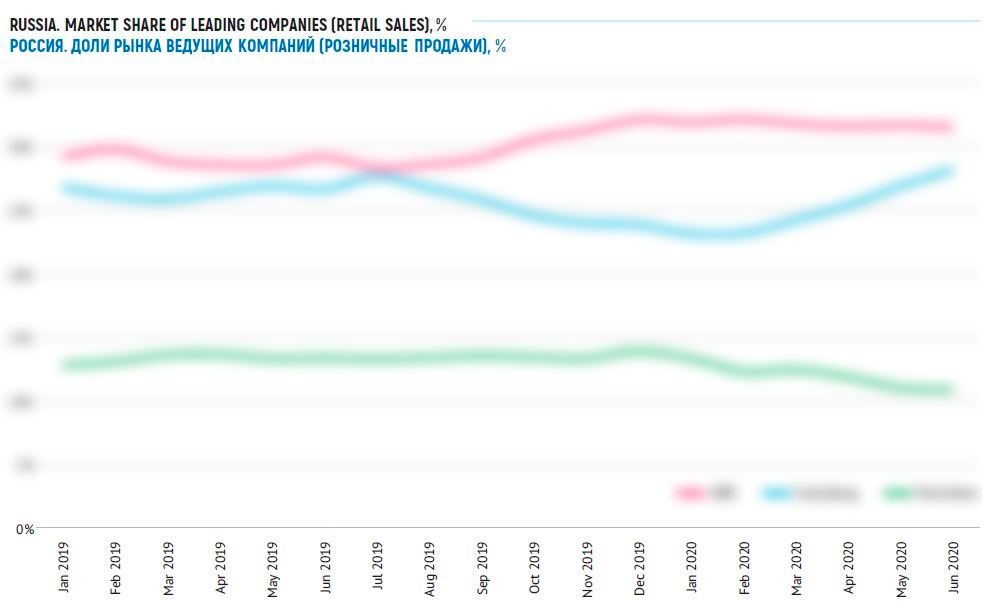

The situation at the retail beer market in the first half of 2020 can be briefly described so:

The federal companies have lost *.* p.p. of their net share. The decline took place due to sales drop at Heineken, Zavod Trekhsosenskiy and Ochakovo. On the contrary, for AB InBev Efes this period was rather positive. Carlsberg positions were multivalued as the market share that had fallen very low has almost returned to the previous level.

The regional brewers’ share in retail has reduced. Most of them kept or even expanded their volumes. Yet, negative impact was made by sales drop at a dozen of key brewers mostly in the Siberia and the Volga region. The situation has started to gradually deteriorate since February 2020. If that trend does not change, the performance will be even worse.

Though consumers in 2020 were likely to economize, the positions of import beer have improved considerably in 2020. There were higher sales of major European brands in the market leaders’ portfolios, as well as independent import distributors’ sales.

In 2019 private labels for the first time yielded their market share to economy brands that belong to brewers. But even before the epidemic, private labels of networks started winning back their positions and most probably will keep their performance by the year end.

Yet, patchy mixture of craft and small regional breweries have achieved the best performance in 2020. There has been a retail sales growth of both bright and expensive and affordable small sorts known only in their home region. Obviously, their growth in the traditional retail resulted from the lockdown and restrictions as beer lovers did not get to HoReCa or specialized retail. But even before the coronavirus, small brewers started working actively with networks.

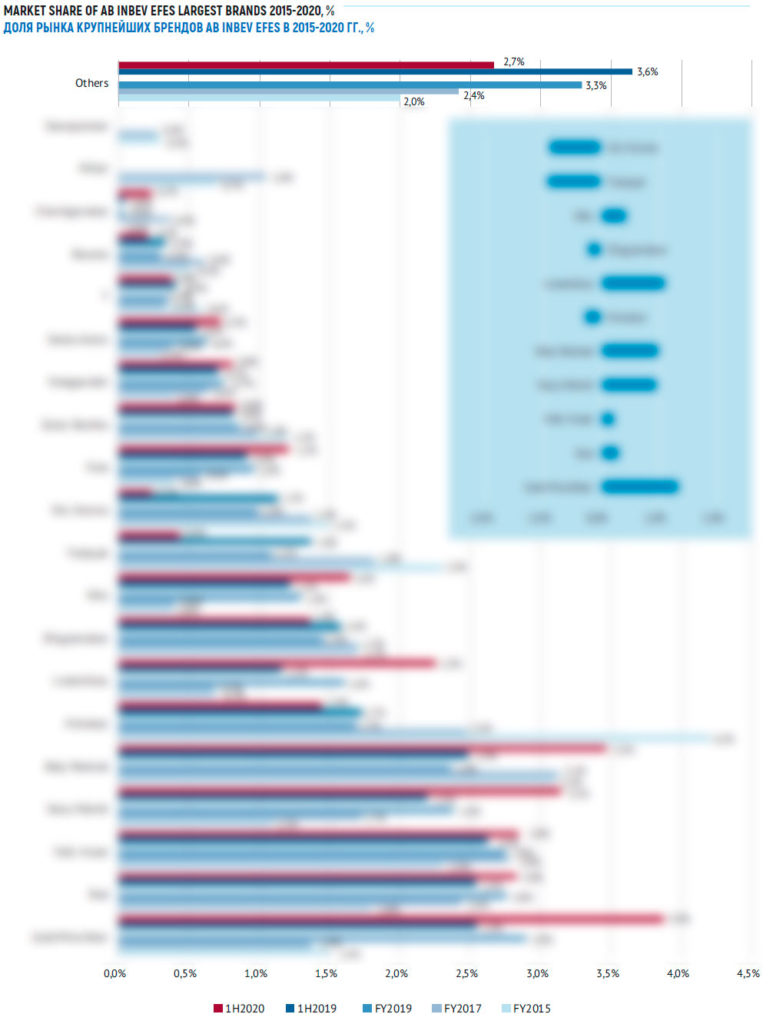

AB InBev Efes

AB InBev Efes has become a leader soon after the alliance forming. After that, for several years, the company increase their pullaway from Carlsberg Group. Yet, in the second half of 2019, AB InBev Efes extended their share in one stroke, having gained about * p.p. that is why in the second half of 2020, the performance is likely to be not so impressing due to the low base effect.

We cannot speak of any geographic priorities of the company because the market share growth took place almost all over Russia. Besides it is not possible to say that AB InBev Efes staked on rebalancing of brand portfolio or sacrificed a margin for the sake of volumes. As the growth was observed along the whole price range.

More likely active work with the modern trade has resulted in the success. When the coronavirus epidemic started, and the consumers went to supermarkets, the market share in networks had a multiplying effect on AB InBev Efes sales.

In general, the positive results were linked to major economy brands that used to belong to Efes. And many brands belonging to AB InBev, went on following the steady downward trend.

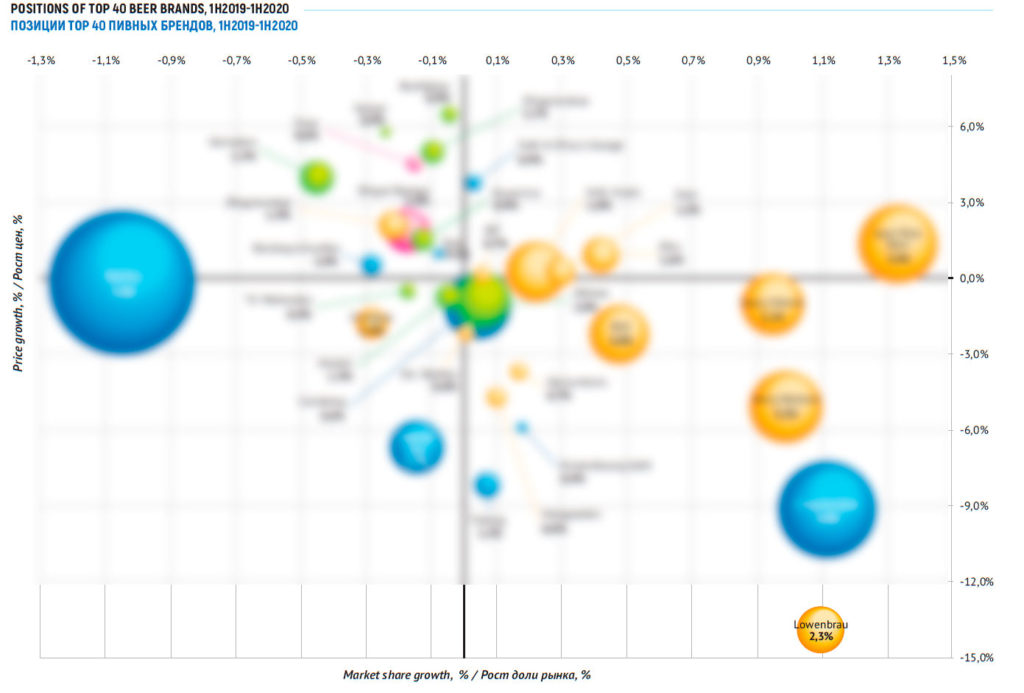

In particular, the market share of Gold Mine Beer and Beliy Medved made a leap. Besides, the share of Tolstyak that got a price rise and still can be attributed to discount brands, has decreased. The same happened to Klinskoe that had its price cut. Currently, the share of these former superbrands is so small, they hardly influence the company’s positions in the economy segment.

In the mainstream segment all key brands by the company have been growing. In particular Stary Melnik has increased its positions considerably (and not by price changing), and Lowenbrau has become much cheaper. Besides, Efes beer share has grown considerably. A modest (resulting from low market weight) yet positive contribution has been made by Zolotaya Bochka and *** beer.

In the premium segment the company’s positions have been not so certain. Losing Staropramen and Miller that moved to a competitor’s portfolio could not impact the performance of 2020. Yet, it led to new “vacancy”. It was obviously decided to fill it by moving Sibirskaya Korona to the premium segment. This brand had been long losing its market share and shifting the emphasis to special sorts. But price rise by almost **% led to a sharp market share fall. The decline of Sibirskaya Korona was not able to offset the growth of Bud brand which received additional impetus as sort Bud Light was launched.

Excellent performance has been achieved by import brands by AB InBev Efes. The company has been long a major distributor of foreign beer in Russia owing to its developed supply network. The import segment leader is German beer Spaten. Besides, sales of Mexican beer Corona have grown, despite the negative connotations and news of its production halt.

Carlsberg Group

The reduction of Carlsberg Group market share is obviously connected to the market share growth of the major competitor as they are in antiphase. The decline started in summer 2019 and reached a local minimum only by 2020. But then, the company started restoring their positions and almost returned to the starting point in summer 2020. By the way, they were winning share not from AB InBev Efes but from Heineken and regional producers.

Judging by the sales geography, Carlsberg Group volumes have been falling considerably in Far East region slightly declining in Southern region. However, due to different market sizes, the negative effects were nearly the same. At the same time, the company succeeded in the Siberia and kept its market positions in other regions of Russia.

In the economy segment Carlsberg Group managed to keep their market positions due to multidirectional dynamics of brand sales. On the one hand, the market share of Zhigulevskoe grew by *.* p.p., which brought the brand on the steady second place in the company’s brand portfolio. At the same time, the share of federal economy brands Bolshaya Kruzhka and Arsenalnoe went down. However, for Arsenalnoe the decline can be explained by the fact that the brand became more expensive and moved from the economy segment to low mainstream. Besides, almost all regional economy sorts by the company lost some of their market share.

In the low mainstream segment due the price reduction the share of Zatecky Gus has stabilized. There has also been some growth of new brands, namely Gorkovskoe and Peterhof, as well as licensed Carlsberg that is becoming a more and more affordable and significant brand in the company’s portfolio. Naturally, the company’s positions strengthened due to Arsenalnoe, but that was not an organic growth.

Certainly, Baltika most of all triggered the company’s positions fluctuations. It was its share that fell and has not fully recovered yet. However, we can speak of long standing downward trend. More affordable sorts by Baltika have experienced the biggest pressure and their market share reduced dramatically; that is why the average brand price already corresponds the upper mainstream segment of the beer market. At the same time, in the upper mainstream segment the share of Tuborg stabilized after a long downslide, and Seth & Riley`s Garage share stabilized after a growth. Holsten brand went on losing the market share.

Among high-margin brands one should pay attention to further sales growth of Kronenbourg ****.

The market share decrease took place in the first half of 2020 due to the high-base effect. The company’s sales volumes in retail almost stopped growing unlike the market. But since the market share decline of Carlsberg Group happened in the low season 2019-2020, its influence on sales will be close to neutral by the end of 2020 (if the company does not spoil its positions).

As for negative results – in the first half of 2020, the sales structure of the company shifted to the economy segment more than at other companies and the average price for sold beer fell by *%.

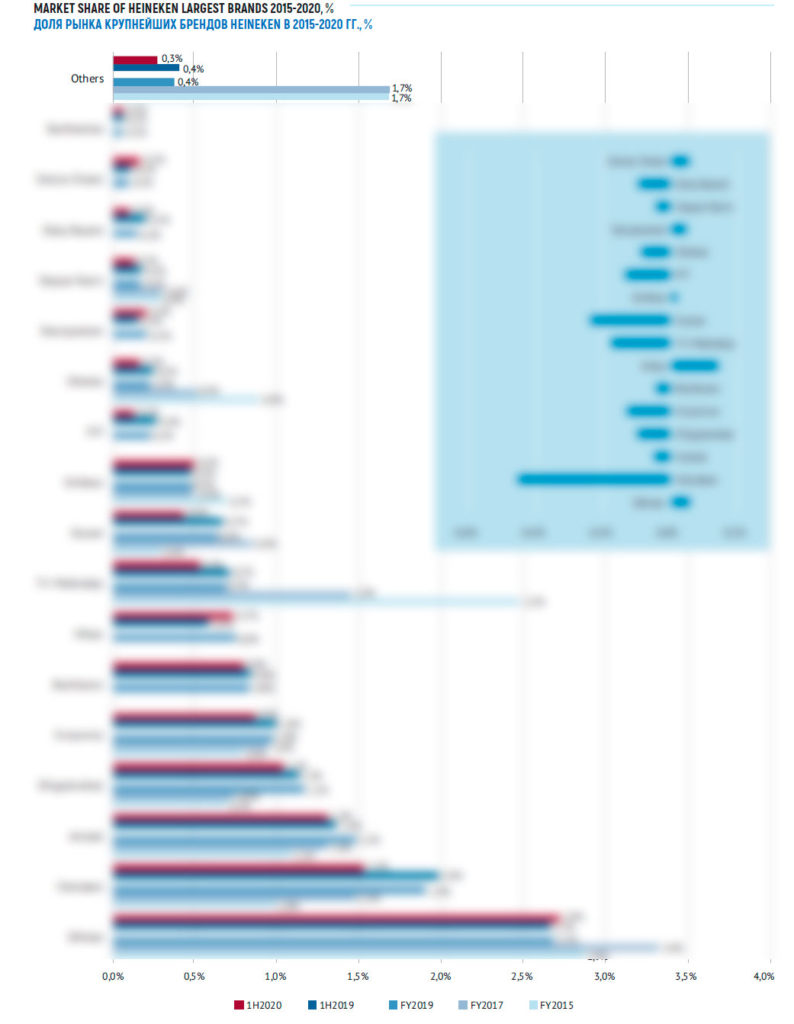

Heineken

Over 2019, the position of Heineken company was virtually unshakable despite the expansion by AB InBev Efes. However, in 2020, restoration of Carlsberg Group and some other producers took place at the account of Heineken’s market share deterioration. The company yielded about * p.p. and is not likely to stop at that.

One of the obvious reasons for the volume reduction is a rather strict policy towards affordable brands. Though competitors were reducing average prices by shifting the gravitation point to the economy segment, Heineken, on the contrary, increased its average selling prices for beer by *% in the first half-year 2020. At the same time, regional brands by the company moved from the economy to low mainstream segment.

Another less obvious but more important reason could have been deterioration of relations with the modern trade. This is proved by the fact that the market share went from stability to decline exactly early in 2020, as the contracts were being revised. The reduction was taking place simultaneously in many regions and for a range of brands.

In Autumn, there appeared publications saying that Heineken demanded one of the supermarket chains to increase the number of SKU products on the shelves in exchange of their contract extension in 2019. And as a result, the chain called the conditions discriminatory and the contract was cancelled.

Possibly, the situation was not so clear-cut and Heineken was not willing to obey the network dictate unlike their competitors. One way or another, the inflexible position against the risen due to quarantine power of the modern trade, could have become the reason for representation reduction. Naturally, this could led to negative synergy for the company’s sales against the flow of consumers to supermarkets.

Heineken volumes have been most adversely impacted by sales decline in Central region of Russia and in the Volga region (though in that region the company had been always very strong). Besides, the volumes in the Siberia and North-West region. A certain growth in the Ural and Far East could not substantially improve the performance of the half-year.

The company has substantially dropped their positions in the economy segment, which is probably connected to intention not to take part in the price competition. The market share decline of federal brand Tri Medvedia was the most significant (starting from 2015 it has decreased by * times). But the sales of some key brands have Bochkarev, PIT also fell dramatically (the last one decreased to the point of disappearance in the retail).

Comparatively stable positions of Zhigulevskoe beer have become a rare exception in the Siberian region despite its retail price growth. To some extent we mean a local brand that competes with regional producers on the Siberian and the Far East markets as in other regions its sales are rather small.

In the low mainstream segment , in the first half of 2020, the company temporary kept their positions due to checking prices for key brand Okhota. Its average price in the retail decreased by *% and the market share in response grew. However, by summer, the price effect exhausted and sales went into a pronouncedly negative trend. Besides, the local achievement in spring was outweighed by the market share reduction of license beer Glosser that got more expensive.

In the big family of license marginal brands Heineken, Amstel and Krusovice market share reduction also was partially slowed by price regulation. In this connection positioning of major international brands by Heineken shifted to the border between upper mainstream and premium segment which, however did not help them to keep their sales.

Let us note that early in 2019, at the level of retail beer Staropramen and Miller virtually flowed from AB InBev Efes to Heineken portfolio. in the aggregate these brands account for less than *% of the beer market. The net positive result of all of redistributing volumes by */* was achieved in 2019 and accordingly by */* was achieved in in the first half of 2020.

However, in spring 2020, a rapid and simultaneous market share decline of the key license brands led to such a negative result that exceeded remaining positive impact made by Staropramen and Miller by several times. As a result, in the first half of 2020, the company substantially yielded their positions in the marginal segments of the beer market.

If we consider the current market share of the company to be at the minimum and not likely to fall lower, the second half of 2020 will be linked to further deterioration of figures owing to the high base effect of 2019. One could speak of positive structural changes in Heineken portfolio, but the market share of economy brands is rather small now and its reduction does not have a strong impact on the sales. Furthermore, the international license brands dropped the market share even more.

2GIS about a tern in development of special beer retail

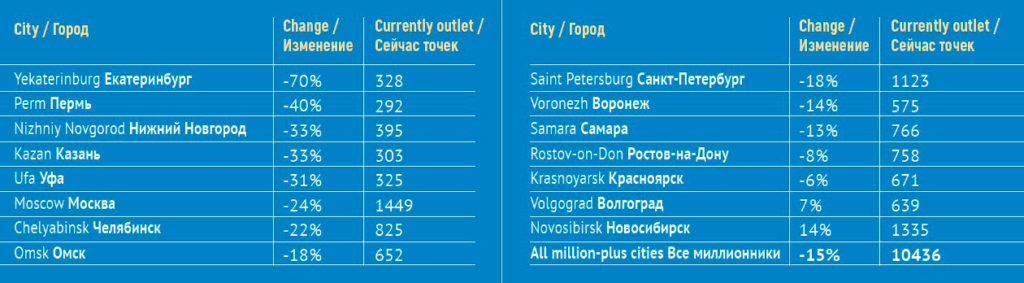

For once in * years, in major Russian cities the number of draft beer shops went down.

According to information of 2GIS, that regularly updates the list of operation organizations in cities such reduction is being observed for the first time in five years: since 2015, the number or draft beer had been increasing by **-**% per year. The peak number was achieved in October 2019 – at that time 2GIS maps depicted ** *** shops selling beer on tap in million-plus cities. In October 2020 there appeared ** *** – by **.*% less than a year before (equal * *** outlets).

The biggest reduction of outlet number is registered in Yekaterinburg as their number decreased by **%. In Moscow they reduced by **% and by **% in Saint-Petersburg.

This dynamics was influenced along with other factors by closure of beer departments in Krasnoe&Beloe network that is widely represented in many cities. In 2019, the company excluded the draft production out of its portfolio. This decision was taken due to sales growth of illegal production (without excise and taxes payment and so on). Compared to it, the beer Krasnoe&Beloe was selling was uncompetitive.

Only in two out of ** million-plus cities the number of shops has grown over the recent years – namely in Novosibirsk and Volgograd. Among other reasons is the fact that in these cities the format of small food shops near the house often having a special draft beer department is still popular. Nearly **% of draft beer outlets in Volgograd and Novosibirsk are located in such shops. At the same time, in other cities (in Moscow, for example) the format of beer “near the house” does not enjoy popularity and the number of such outlets decreases.

According to 2GIS by October 2020 the biggest number of specialized draft beer outlets is located in Moscow and Novosibirsk while in Kazan and Perm their number is the smallest.

Other companies

Moscow brewing company in the first half of 2020, kept its sales nearly at the same level, which against the market growth meant some market share reduction to the company. At the same time, MBC unlike big competitors mainly kept or even rose the prices for its brands.

Keeping in mind that the focus of MBC is shifted to premium, and the sales geography is oriented to Moscow one can speak of some polarization in the sales structure.

Thus, by launching Motor brand and the growth of Kruzhechka Cheshskogo share, the company has strengthened its positions in the economy segment. In the upper mainstream the market share of Zhiguli was relatively stable, but reduced at Faxe. And in the premium segment the popularity of craft Volkovskaya Pivovarnia range as well as Khamovniki brand has increased considerably.

Besides, there was an interesting regional rebalancing of the MBC priorities that is reflected in expansion. The volumes increased in the Siberia in the South of Russia and, at the same time, they decreased in the North-Western region.

Zavod Trekhsosenskiy over the accounting period has lost some of its retail sales volume and the market share. So far, it is too early to speak of a negative trend, there rather was a local decline that started late in 2019 and finished in spring 2020.

Probably the reasons lie in the relations with the major partner, big network of alcohol supermarkets Krasnoe&Beloe. The fundamental reason is connected to the alconetwork’s refusal to sell draft beer. Another reason is temporal sale termination of two biggest brands namely Venskoe and Varim Suslo that are packed in PET and used to be the key ones for partners. The share of those brands started falling in spring 2019, and decreased almost to zero in December-January. Then the sales have begun restoring but they are still far from the previous year level.

Ochakovo company suffered most of all federal scale brewers. Its retail sales declined by nearly a quarter. The reduction could be observed all over the country but the final performance was mostly influenced in the Central region. The market share and volumes were decreased at all major brands except for beer Narodnoe

One of the reasons for the negative changes lies on the surface. Ochakovo more than other federal producers is focused on traditional rather than modern trade. A big role was played by stronger competition in the economy segment.

Regional producers in general have lost market share in retail from **.* to **.*% by the end of 2020. These data are confirmed by Federal Service for Alcohol Market Regulation concerning beer shipments.

Let us note that most of regional breweries have increased their output volumes and the market share. But there is no contradiction as the decline has influenced big breweries that determine the final figures.

Among ** breweries that yielded the most negative results by volume a half is situated in the Siberia, they are Tomskoe pivo, Barnaulskiy pivzavod, Ayan, Borikhinskiy pivzavod and Osha. Obviously they are to a big extent focused on the draft beer market that has significantly suffered due to lockdown of specialized retail.

The regional producers’ share was also negatively impacted by brewers from the Volga region. We mean holding Buket Chuvashii – Bulgarpivo and Dzerzhinskiy Pivazavod as well as Deka being in the state of the owner transition for subjective reasons.

However, one can list a dozen of substantial businesses that managed to attenuate the negative trend. In the Siberia itself, in the first half of 2020, Bochkarevskiy pivzavod, Udacha brewery, Pivovarnia Kozhevnikovo and Shulginskiy pivzavod improved their performance.

Certainly, twofold output growth of brewery Beliy Kreml stands by itself (officially to * mln decaliters in the half year), Beliy Kreml being a new and systemic project.

If we speak of a situation in general, by the end of 2020, one can expect a further deterioration of the market share of regional brewers. Over the accounting period, it was following the downward trend which taking into consideration the high base effect of the last year does not give much grounds for optimism.

The market share of many brands by small brewers increased in the first half of 2020.

In absolute figures minibreweries and small regional breweries showed maximal growth among all groups of brewers. Their volumes extended by almost **%. This, probably, can be explained not by organic growth but by reallocation of sales from beer shops and HoReCa to networks.

In particular, in most of Russia regions the share of small breweries amounts to *% but in the South it exceeds *% and approaches *% in the Siberia.

To get the full article in pdf (28 pages, 27 diagrams) propose you to buy it ($40) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.