In 2016, fast increase of excises and resulting price spike stood in the way of the beer market stabilization. Most of competition (as well as mass sorts) moved to the economy segment of the market. The biggest losses were incurred by the leading three, especially Obolon, which again experienced pressure after reallocation of Efes market share. However, one should already speak of TOP-4. Group Oasis CIS (PPB) became a strong player and competitor to transnational companies. Besides the net sales of many regional medium breweries look rather good and 16-fold cost reduction wholesale trade license for craft brewers opens up a possibility of rapid growth in 2017.

Reasons for decline

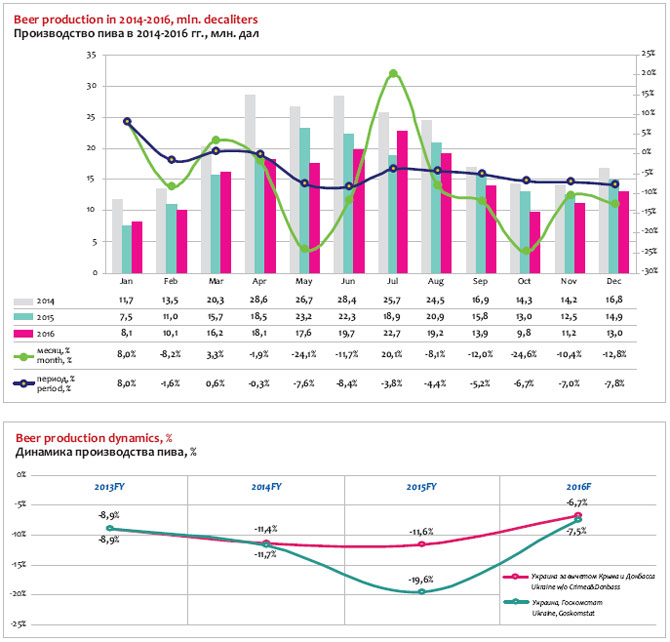

Following the collapse of the Ukrainian brewing industry in 2015, we can see a negative dynamics slowdown, which in our view can be considered a transition to stabilization.

Current data by Ukrainian State Statistics Service speak for a 7.4% beer production decline to 179.8 mln dal in 2016. A year earlier, the decline amounted to 21%.

In 2015, market foreclosures in Eastern Ukraine and the Crimea as well as economic recession deprived Ukrainian brewers of a fifth of the production volume.

Thus, in the territories currently beyond Ukrainian control, … mln dal of beer was produced in 2014. Next year, the volumes fell to … mln dal, and in 2016, there was no official data from those territories. Accordingly, the official data reflect an …% production facilities decline in 2015 and a …% decline in 2016.

However, these figures do not reflect the market situation as beer realization volumes in the territories beyond the control of the Ukrainian authorities exceeded production. In 2015, the official deliveries volumes could have reached nearly … mln dal. Correspondently, by the end of 2016, the negative impact of those territories in the market decline accounted for up to …% and one can say that other market factors turned out to be decisive for the market reduction.

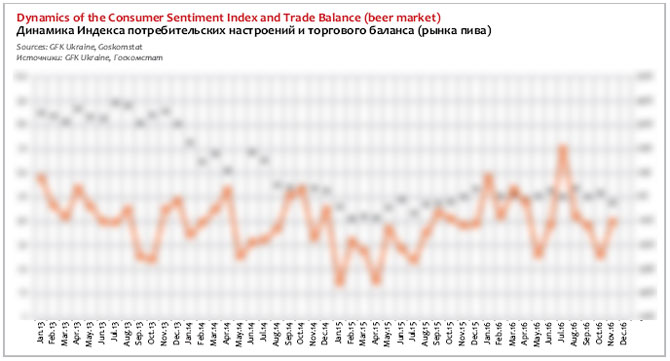

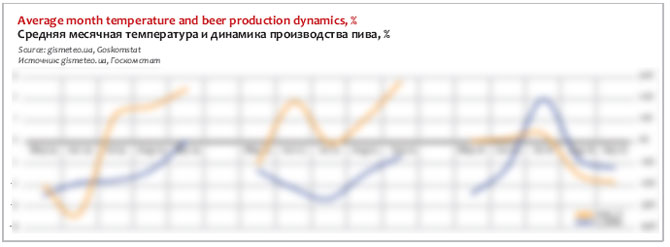

In 2016, social and economic situation in Ukraine was not better than in 2015, yet there were no shocks. The impact can be estimated as we compare the dynamics of consumer sentiment index (CSI) which is calculated by GFK Ukraine, to the beer production dynamics. One can see a distinct link between the two indices during the period from December 2014 to August 2015. That was the time of hryvna against dollar rate collapse and a dramatic inflation upheave. Then the both indices were growing steadily for some time.

Ukrainians got slightly better assessments of their material status and that gave some grounds for prospects of beer market stabilization. Further declines of beer production index took place amid a rather even CSI dynamics. In other words, in 2016, the direct impact of social and economic factors was not the main trigger for the decline. Instead, other specific for the beer market factors came to force.

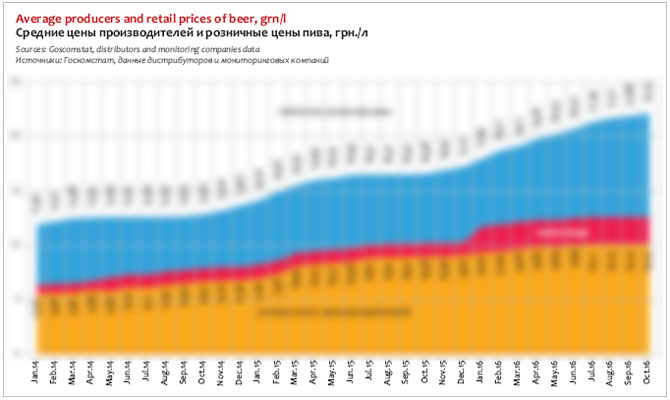

In view of the unprecedented inflation rise and difficulties with budget pumping, the Government took a tough decision. Starting from 1 January 2016, the beer excise has grown twofold from 1.24 to 2.48 hrn per liter. That was followed by an intensive and prolonged retail price growth which could not stay unnoticed by consumers. It lasted from January till July 2016, and then the dynamics slowed down a little. In total, over this period, retail prices increased by … hrn/l to … hrn or by …%. The fast fall of beer affordability played the main part in the beer market decline during the first half of 2016.

During the second year half weather was affecting beer sales. In July 2016, the temperature was much higher than a year earlier*. The prices stabilized by that time and brewers’ production started gaining profit. Yet, the average temperature in August and September was lower due to the high base effect of 2015, when the third quarter was abnormally hot. The difference between month to month average temperatures was very substantial for beer sales, i.e. … degrees in August and … in September. During those months, there was a …% production decline. These figures can be explained if not by weather, then by negative “synergy” with other factors.

* Archive daily data of average temperature in Kiev were estimated.

As we can see, the major negative factors were in 2016 not fundamental. A 12% excise rise is planned for 2017 in accordance to the official inflation rates. Such increase is likely to have a negative impact on the beer market. The weather base of 2016 (average temperatures in sales seasons) can be considered neutral. So, provided the economic situation remains stable, there are preconditions for beer market stabilization in 2017.

Subtle (at such a short time) negative impact is made by the general tendency of reduction of alcohol consumption by Ukrainian population. A slow positive effect is being observed due to young consumer group expansion as the population has passed the demographic “pit” of the 90-ies. These trends have faded over the recent years but can become more significant in case of the market stabilization.

Industry performance in figures

The Ukrainian beer market, as the trade balance result, in 2016 decreased by …% to … mln dal. As we can see, in 2016, the volumes of beer production and market almost evened by their dynamics and sizes due to export reduction.

The beer export decreased by …% to … mln dal by preliminary data. Previously there was a more rapid decline. Yet, we can be sure that the export will stabilize as the volumes of beer deliveries to the major consumers are constantly changing. As far back as in 2014, the bulk was delivered to Russia. In 2015, Belarus became the leader and Poland received a considerable volume. By the end of 2016, Moldova became the biggest consumer of Ukrainian beer and Poland cut its purchases, yet Lithuania is increasing the volumes.

Beer import in 2016, decreased by …% to … mln dal. Virtually all of it is supplied by far abroad countries and belongs to premium and superpremium segment. The list of the leading suppliers remains traditional: Belgium, Mexico, Germany, and Czech Republic.

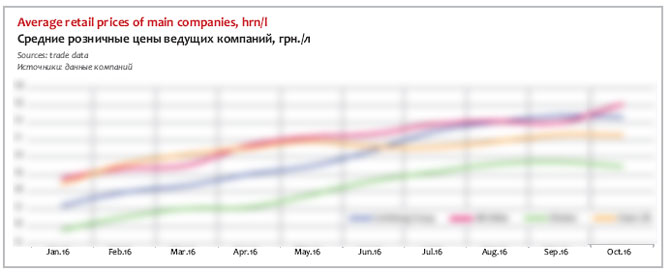

Weighted average prices of producers excluding VAT and excises grew by …% amounting to nearly … hrn for a decaliter in 2016. Most rapidly the prices were rising during the first half of 2015 as well as in the first half of 2016. The second half year of 2015-2016 was the period of some stabilization. By the end of 2016, beer cost about … hrn for a decaliter.

If we add the excise size to this cost, the manufacturer’s price in 2016 grew by …% to … hrn per decaliter.

In dollar expression, because of the continued hryvna devaluation, the weighted producer’s price in 2016 remained the same i.e. $… for a beer decaliter. Including the excise, the manufacturer’s price rose …% to $… for beer decaliter.

Knowing the beer output volumes and the average producer’s prices, we can calculate the volume of their revenue from beer realization. If we take into account the manufacturer’s price without excises, the revenues in 2016, grew …% to … bn hrn (in 2015 it increased by …%).

The State Statistics Service of Ukraine publishes direct data on volumes of sold production by activity categories, which seem undervalued but reflect the dynamics. In 2016 the sales volume by category “Beer production” grew …% to … bn hrn (a year earlier the growth amounted to …%).

In dollar expression the producer’s revenue in 2016 went on decreasing, though at quite lower rates i.e. by …% to nearly $… mln (by …% in 2015).

Inflation and twofold rise of excise incited a very rapid growth of retail prices in 2015-2016. Accordingly, the beer market by value was also growing despite natural volumes falling. In our view, in 2016, it increased by …% to … bn hrn. In dollar expression the growth reached …% to $… bn.

Inflation and twofold rise of excise incited a very rapid growth of retail prices in 2015-2016. Accordingly, the beer market by value was also growing despite natural volumes falling. In our view, in 2016, it increased by …% to … bn hrn. In dollar expression the growth reached …% to $… bn.

Thus, summing the results of 2016, one can say that after the excise rise, consumers started drinking less, but paid more for the consumed beer. The growth of manufacturer’s and retail prices set off the decrease of the natural volumes, excluding one index, that is, dollar revenue of producers.

Let us notice that because of the hryvna devaluation and beer output reduction, since 2013, the brewers’ revenue has decreased by … times. Obviously, such changes made the Ukrainian beer market not too much attractive for the international companies that had to convert hryvna revenue into other currency. That was one of the triggers for their market reduction.

Companies and brands

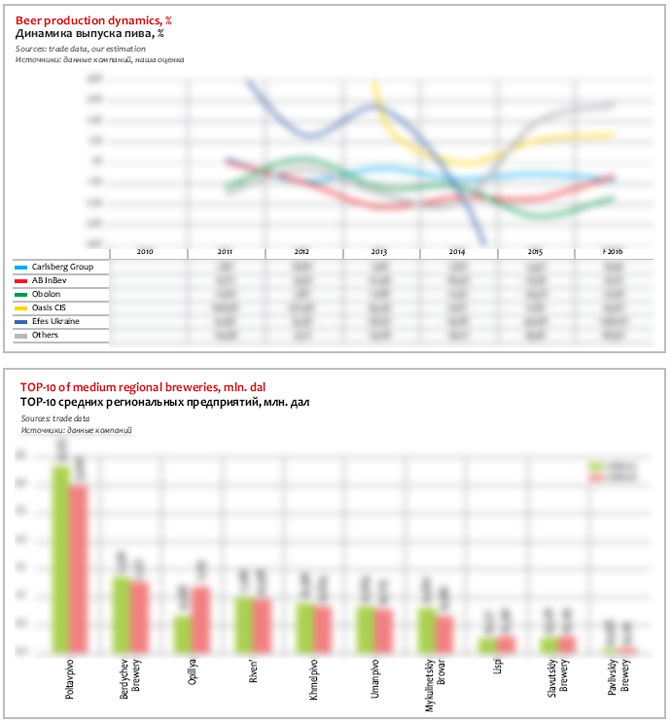

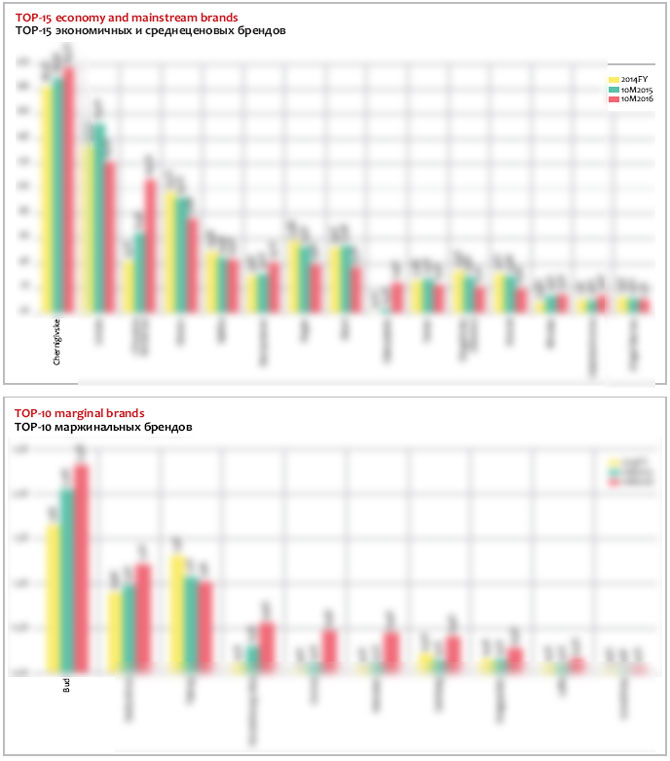

Since 2013, the leading three Ukrainian brewers have been gradually reducing their output volumes. The production dynamics of the major companies over this period reflects a slow steady reduction of Carlsberg Group market share, stabilization following decline at AB InBev, and the second downsurge of Obolon sales. Efes has practically left the Ukrainian market. Instead, Oasis (PPB) and rest of the producers in general demonstrate a good performance amid the falling market.

The leading ten regional producers have by preliminary data decreased the beer output by …%. Accordingly, their share has grown considerably despite the falling market.

Small producers’ sales in 2016 have grown judging by collateral data, yet it is difficult to estimate that growth as current statistics includes only middle and big businesses. In 2017, one can expect a considerable increase in number and volumes of minibreweries output. Brewers with a yearly output volume of maximum 300 thousand liters were exempt from back-breaking half-million price for wholesale license. Now they have to pay 30 thousand hryvnas for a wholesale license. As we know, for many entrepreneurs it was that clampdown that formed the main barrier for business development.

Carlsberg Group

Under our assessment, in 2016, the production of Carlsberg Group decreased by …% amounting to … mln dal, that is, the negative dynamics sped up a little. The share in the total output volume declined by … p.p. to …%. However, the company holds the first place in the market which was won as far back as in 2014.

Under our assessment, in 2016, the production of Carlsberg Group decreased by …% amounting to … mln dal, that is, the negative dynamics sped up a little. The share in the total output volume declined by … p.p. to …%. However, the company holds the first place in the market which was won as far back as in 2014.

The average manufacturer’s prices for Carlsberg Group in autumn 2016 reached … hrn for beer decaliter* which is …% higher than the average Ukrainian prices and considerably higher than that of competitors. Such difference can be connected to control over price formation. The realization volumes of Carlsberg Group beer, calculated basing on manufacturer’s prices of breweries in 2016 amounted to about … bln hrn.

* Inclusive of VAT and excises

The official revenue of the Ukrainian subdivision of Carlsberg Group from product realization* in 2015 amounted to … bn hrn (+…%). By the end of 2016, it can also grow at … rates due to price rises, premiumization, and non-beer category development.

* Exclusive of VAT and excises

By the end of 2016, Carlsberg Group almost came up with their major competitors, company AB InBev by the average retail prices. That was connected both to increasing manufacturer’s prices for beer and to refocusing on marginal sorts development. As a result, the sales of cheap beer were falling faster than the sales of expensive beer. These processes can be considered company’s reaction to the beer marker reduction.

To the fullest extent, the changes were connected to the key brand development. By autumn 2015, Lvovskoe brand reached the peak of its market share. At that time, its lagging behind the biggest brand – beer Chernigovskoe amounted to several percent. In 2016, the market share of Lvovskoe was fluctuating but the general trend during the peak of the sales season was obviously negative.

Under our estimation, this results from priority change, i.e. “wedging in” of more expensive sorts Robert Dorms into the main product range of economy brand Lvovskoe. The package and subbrand positioning have little in common with other Lvovskoe sorts. And Robert Dorms was stable during 2016, standing at 2% of the Ukrainian market. Well known inexpensive sorts 1715 and Svetloe kept relative stability against 2015, slowly decreasing their market share. The key sort is still 1715 which is immediately associated with Lvovskoe brand. Instead, other sorts became redundant in the new strategy of the brand development.

In May 2016, it became obvious that Ukrainian brewers had been too optimistic, and the market was developing by a negative scenario. At that time, amid the rapid price rise, the average retail price for Lvovskoe 1715 on the contrary went down, which excellently stimulated its sales. This reduction was largely conditioned by package offer profitable for consumers. But subsequent fast rise of Lvovskoe 1715 retail price immediately changed the growth trend into negative.

Baltika brand under our estimation has not increased sales but secured its position on the market at approximately the level of 2015. It is still the second biggest brand in the Ukrainian portfolio of the company. Inside the product range, there was a growth of … sort, while … went on decreasing in 2016.

Arsenal brand was a weak spot for the company and made a substantial contribution into its market share reduction. By autumn 2016, … sort was almost impossible to spot in retail. The remaining … has also considerably decreased due to competitors’’ higher activity in the strong beer sector, in the first place, … recently output by Oasis CIS.

Instead, in 2106, Minskoe Zhugulevskoe, an unusual for Ukrainian market beer, continued enjoying popularity growth. Its market share stabilized at nearly 1.5%. Thanks to positive image of Belarusian products, and distancing from economy sorts, this version of Zhigulevskoe looks like an interesting alternative product, which allows its positioning in the mainstream segment.

One of the important events of the past season is a sharp fall of title Carlsberg price. Early in 2016, as beer prices started rising rapidly, its retail price on the contrary fell by nearly … hrn per bottle. Beer Carlsberg cost approximately at the level with …, that is, the brand moved from the premium to the mainstream segment. The consumers positively reacted to that step and wider distribution and thus the brand market share by several times and today amounts to nearly …% of the market.

By essence, Carlsberg has now become the most affordable among well-known licensed brands rivaled by only Obolon’s Carling, though Carling was originally positioned as an affordable brand with much humble distribution and popularity level.

Carlsberg Group is gradually tackling beer joint drink groups. This is taking place both due to wider distribution and shelf space of non-beer categories and increase of sort number.

In 2016, the sales volumes of non-alcoholic drinks grew by nearly …% and amounted to about … mln dal. The share of non-alcohol drinks in the total realization volume has risen from … to …% under our estimation. Almost all volume accrues to Kvas Taras, which has rapidly gained the lead in the kvass market. However, the revenue from selling one kvass decaliter is almost … less than from selling one beer decaliter (net of VAT and excises). That is why the development of kvass direction is in the first place connected to set off the beer sales decline.

Besides Carlsberg Group has rapidly entered cider category and took … of this market with its key brand Somersby. Its retail price as well as its producer’s price is approximately …% higher than the average beer price. In the company’s sales structure cider accounts for as much as …% under our estimation.

AB InBev

Under our estimation, in 2016, production of AB InBev beer was decreasing much slower than the market, that is, by …% to … mln dal. Despite the negative dynamics, this is still the best result among the leading three. And this is much better than the previous four years, when AB InBev was losing its positions rapidly. In 2016, its share in the total output volume grew … p.p. to …%. The company’s branding activity was the main driver of the dynamics change.

Due to major regional license brands in the company portfolio, its average retail prices have been until recently running ahead of those of competitors. However, after the spring price leap, due to excise rise which affected all companies, AB InBev was more restrained than Carlsberg Group. The average prices trajectory was changing along with the prices of smaller competitors – Obolon and Oasis. The control over of average prices was for the most part taking place through affordable brands.

The Ukrainian market leader, brand Chernigovskoe is still accounting for about a … of all AB InBev sales. Yet the company’s positions deterioration was to a large extent connected to the dependence on Chernigovskoe, likewise the dynamics improvement over the recent years can be attributed to the brand market share stabilization and its weight decrease.

Until recently, the consumers’ loyalty to mainstream was running out because of this segment borders blurring, by for example brand Lvovskoe. The economic problems and the stricter rationalizing of consumers made it more obvious that it was more profitable to develop the mass major brands in the cheap segments rather than in the mainstream. As a result of brand positioning, AB InBev has changed significantly over a short period of time.

Transition of the basic brand from the mainstream into the economy segment which started as early as at the end of 2014, became an important event for the beer market. To be more exact, key sort Chernigovskoe Svetloe which accounted for nearly …% of the Ukrainian market in 2016, became cheaper compared to the mainstream brands. It’s become the most affordable in AB InBev range, and one of the most affordable brands in retail.

This process was drawn by controlling prices for Chernigovskoe Svetloe, while prices for the company’s economy brands were growing rapidly. Special sorts of Chernigovskoe became more expensive than Svetloe and they can be still attributed to mainstream. Yet, the market share of Beloe, Belaya Noch, Krepkoe, and others together amount to about …%, that is, … less than the main sort.

Alongside with the major sort transformation, the company’s second biggest brand by the sales volumes, Rogan, is getting more status and expensive. Its price against average market prices has reached its peak in spring 2015 and the market share amounted to …%. Yet, when Rogan approached the highest border of the economy segment and the brand’s average price exceeded the price of other mass sorts, the market share started decreasing at a high rate. It was quite reasonable, not even by consumers; rationalism, as Rogan had been long years positioned as cheap beer and has got a certain image.

The company tried to overcome the negative trend by two ways – by decreasing the retail price for Rogan at the end of 2015, and a deep restyling of the brand, which resulted in a mainstream image for Rogan while it still retained brand awareness. Since May 2016, the image and retail price of 2016, have looked balanced taking into account the market conditions. Rogan market share stabilized at approximately …%.

Although AB InBev has yielded its positions in economy and mainstream segments compared to 2015, the marginal brands, on the contrary, saw their market share increase.

An advertising campaign featuring Prague legends stirred interest to beer Staropramen which was then followed by a limited collection rollout. Besides there have been specialties – wheat and dark beer sorts, that draw consumers’ attention. In 2016, Staropramen market share increased by … p.p. and as of now amounts to nearly …%.

Brand Bud seems to have attained full growth in 2016 on the Ukrainian market. Its market share was rapidly growing at the end of 2015 having increased by … p.p. to nearly …% by issuing a limited collection. Presently, Bud is one of the most expensive premium licensed brands, so such performance can be considered as good.

Obolon

By the end of 2016, the production decline at Obolon has slowed down, yet, it was still lower than that of the competitors. The decline amounted to …%, to roughly … mln dal.

The sustained decline can be considered in terms of deliveries to the inner market and export. While in 2014, the greatest impact on the negative dynamics was made by the ban on supplies to Russia, since 2015, main problems of Obolon have been connected to the inner market. Under our rough estimation, in 2016 export grew …% to … mln dal and the negative dynamics of supplies to the inner market slowed a little having amounted to – …%, or … mln dal.

From the marketing point of view, the company sales reduction resulted from its being gradually squeezed to the economy segment. After mass brands Lvovskoe, Chernigovskoe, Zakarpatskoe, and others entered it, pressure on Obolon grew sharply. And lagging of average prices of Obolon against two major players was growing during 2016 and by autumn the difference reached about … hryvnas per beer liter.

Currently, the structure of main sales of Obolon doesn’t seem very complicated. More than … is accounted by brand Zibert and about …% by Zhigulevskoe. The remaining brands correspondently give approximately …% of sales.

The retail price of the main three brands is considerably lower than the average prices of Ukrainian beer. They can be allocated on the economy segment spectrum where the border with mainstream segment is taken by the main brand, Zhigulevskoe is positioned in the middle and Zibert is located at the very bottom.

Logically, in the economy segment the brands market share fluctuations mostly depended on the dynamics of retail price against each other and competitors. The rapid reduction of the market share started first in summer 2015, when the company tried to simultaneously raise prices for three key brands in order to maintain their positioning. Then they managed to stabilize the market share of beer Obolon and Zhigulevskoe, though it shrank against 2015. That took place through controlling the retail prices for the brands during the period of beer prices rising after the excise increase. Yet Zibert market share was still declining during 2016.

Not better was the competitive situation for strong beer Desant which in 2015 started experiencing a severe pressure from other strong beer brands, including Teterev by Oasis which enjoyed a fast growing popularity.

Oasis CIS

Sales of Oasis CIS (Persha pryvatna brovarnia) increased despite the common negative picture and now we should speak not of three but four market leaders. Under our rough estimation, in 2016, the increase amounted to 14% to nearly 19 mln dal of beer. And the share of Oasis CIS in the total output volume grew by almost 2 p.p. and amounted to 10.4%.

The company’s sales growth was attained due to the fast position enforcement of a range of brands in various price segments, economy, mainstream and premium.

The main increase in the volume terms was provided by economy brand Zakarpatskoe, which entered the national market a couple of years ago. The fast distribution growth in the eastern direction, interest to national theme and rather low price allowed edging out not only economy brands, but also mainstream mass lagers. It will not be exaggeration to say that Zakarpatskoe became the breakthrough of 2015-2016 on the Ukrainian beer market.

Sort Svezhiy Rozliv is rapidly gaining popularity and making a good contribution to the basic range though it has made the main brand PPB less premium. In 2016, its market share … and reached nearly …%.

Besides, there has been a further market share growth of subbrand Teterev, which has become one of the most popular brands in the strong beer segment. That segment has not for long seen any impressing specialties and PPB diverted from the routine patterns. Teterev was actively gaining weight in 2015, and in 2016, there continued a gradual growth of the market share. It was taken from Arsenal and Desant.

In the premium market segment the company secured its growth by licensed filling of Heineken, which was launched in 2015. Before that, during several years, Oasis had been the exclusive distributor of the brand, which was positioned in the superpremium segment. The licensed version was much more affordable and located roughly in the same price segment as Stella Artois. The explosive expansion of distribution all over Ukraine, and the brand popularity made it possible for Heineken to instantly capture …% of the beer market.

To get the full version of this article propose you to buy it ($35) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.