The market of import beer is rapidly growing and changing. But while in the past years it was growing due to brands variety, in 2019 major and affordable brands from TOP-10 were developing actively. It seems that the fact of a brand origin from far abroad counties, even if it is not well known but has moderate price and good distribution provides for million liters of sales in the territory of Russia. Among distributors AB InBev Efes was far behind, yet the role of Baltika and suppliers of the second row got more important. The boom of German brands was followed by stagnation of import from other traditional regions (and Belarus) instead the supplies from Mexico, Lithuania and Asian countries grew considerably.

Because of the players’ variety and product range wideness we considered only the biggest ten distributors and brands which is less than half of the import. For a more detailed analysis we apply a processed data base by rus-stat.com. You can download the demo version of the database here.

The general situation at the market of import beer in Russia

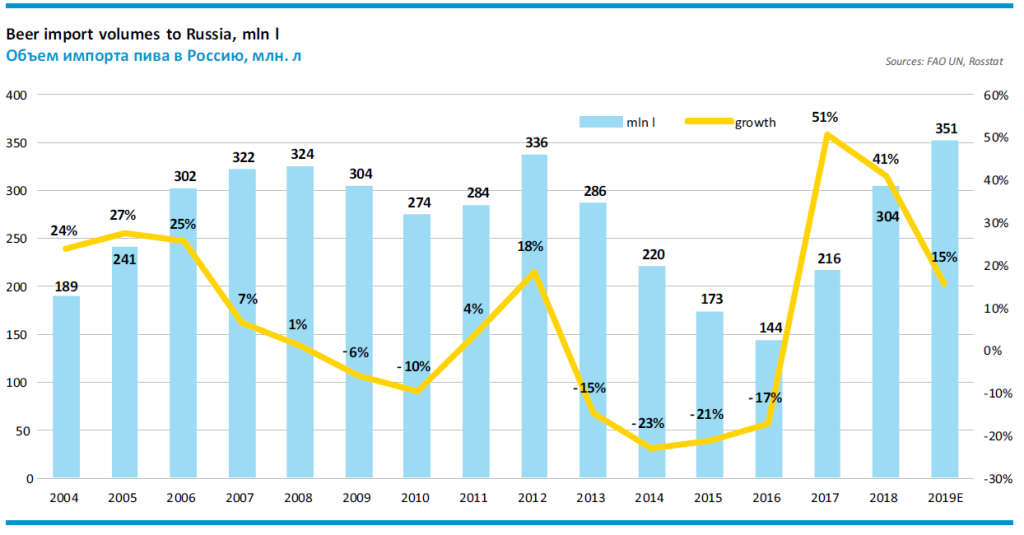

The supplies of import beer in 2019 went on growing by two-digit rates, exceeding the dynamics of other market segments. According to our preliminary assessment the beer import increased by 15% to 351 mln l.

Import brands have long been playing the main role in the premium market segment. Over 2019, the bulk of import beer in the trade balance grew by 0.6 p.p. to 4.6% of beer shipments in Russia.

In 2019, the volumes of foreign supplies reached a historical maximum having broken the previous record of 2008. The dynamics remain high, but lower than in 2016-2018, as import was recovering from a deep decline. Besides, let us note that compared to 2016, the volumes have increased more than twice.

The customs value of import beer in 2019 grew by 10% to $316 mln. Its lagging behind the physical volumes was connected both to shifting focus of major distributors to cheaper brands and to growing share of shipments between related subdivisions of international groups.

Besides, despite lower prices the supplies structure did not so much drift towards the countries of customs union as we could except. In 2019 the beer import from neighboring countries remained approximately the same, instead the supplies from EU countries, Asia and America have grown considerably.

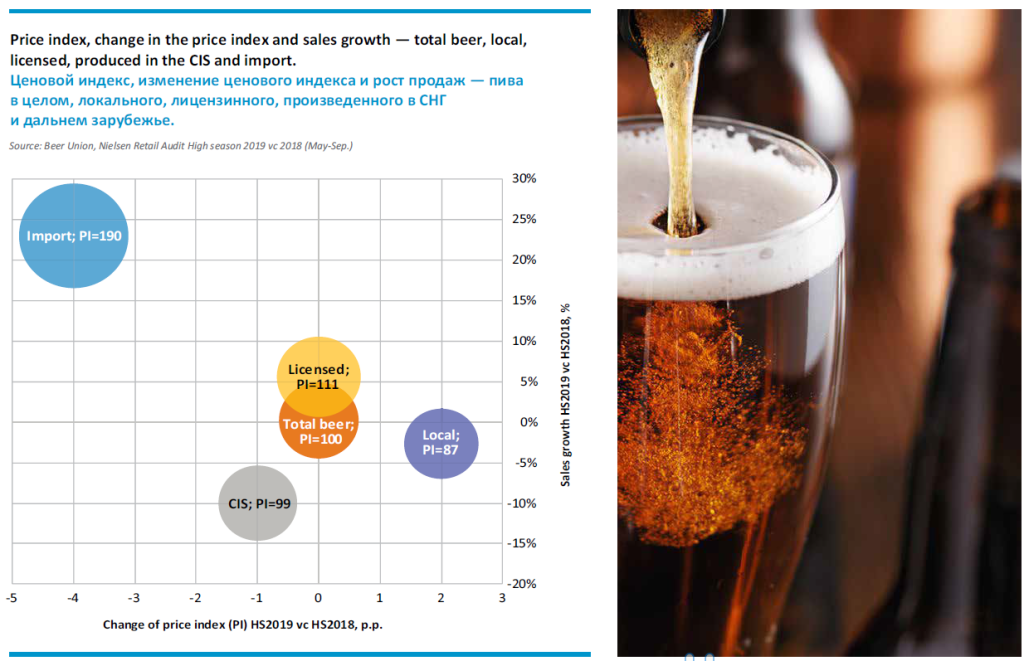

The official statistics approximately correspond to the data of retail audit by Nielsen. The sales of beer from far abroad increased by 23% in the high season of 2019 (May through September). And its share grew by 0.6 p.p. to 3.4%. At the same time, the beer sales brought from the CIS countries declined by 10% though its price is not much higher than the local brands.

To some extent the growth of import from far abroad can be explained by 4% reduction of the price index according to Nielsen. Ruble strengthening and importers’ focus shifting to comparatively inexpensive beer helped to control the prices. However, in retail the import beer costs nearly 70% more than the license brands and 2.2 times more than local Russian brands.

As we can see, the difference in loyalty of Russian consumer to Russian and import brands is ever more considerable in favor of import ones. The data of Nielsen allow us to expand this analogy, if we call beer from neighboring countries “local” ones and license beer is “foreign”.

Though craft beer is not taken into consideration, in this segment of the Russian market the competition is getting stronger due to many well known foreign breweries – there appears a lot of small importers of craft breweries products.

The supplies geography

In 2018, the world beer trade unexpectedly sped up (+3%), though prior to that, it was increasing at rather modest rates (nearly +1%). Transborder beer supplies amounted 15.68 bn liters and only 1.9% of their volume falls upon Russia.

Though the Russian share is still not very large, its significance as beer purchaser over the recent years have been increasing. For example, the share of Russia in the global trade has doubled since 2015, and the country has moved from the 26th to 11thposition in the general list of beer importers.

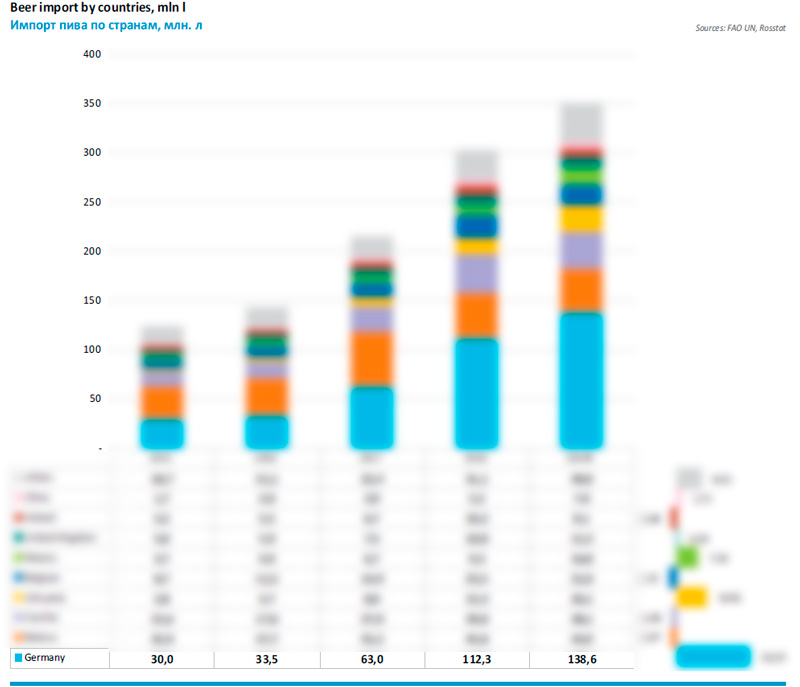

The geography of beer import to Russia has changed in favor of Germany. While in 2015 it accounted for nearly a quarter of Russian import, in 2019 for almost 40%. But we cannot speak of a geographic consolidation, as there are no absolute leaders among other countries – their shares are being blurred.

In general, we can single out three major trends basing on the companies’ specializations:

- In the first place, there has been intensive supplies growth of inexpensive German beer, which is distributed by major importers.

- In the second place, both leaders of the beer market and companies of the second-third tens have been rapidly increasing affordable beer supplies from the Baltic countries.

- For the third place, the import of Asian brands, that are supplied by Russian Far East companies, has expanded considerably,

The positive dynamics in Germany, Lithuania and Mexico is connected to the price competition as increased the import of comparatively inexpensive brands. At the same time supplies of inexpensive beer from Belarus went down (which is in tune with the trend of popularity reduction of local brands). Besides under the pressure of price competition there was a decline in import from the countries well known at the beer map of the world: Czech Republic, Belgium and Ireland.

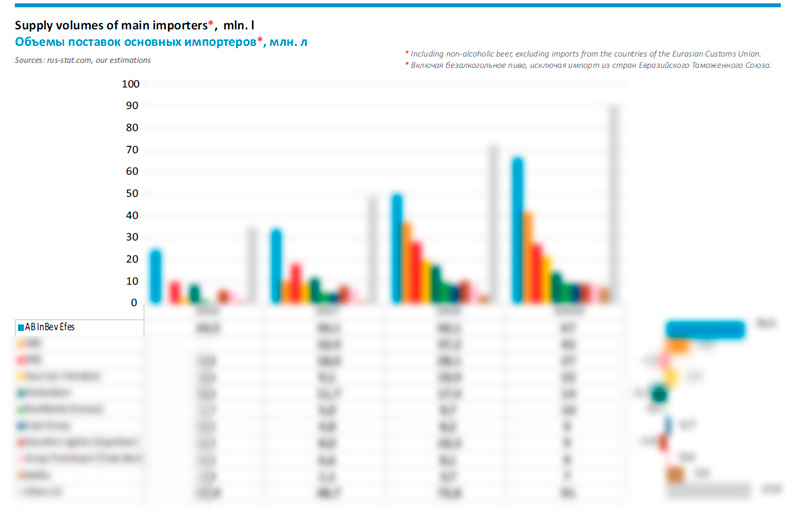

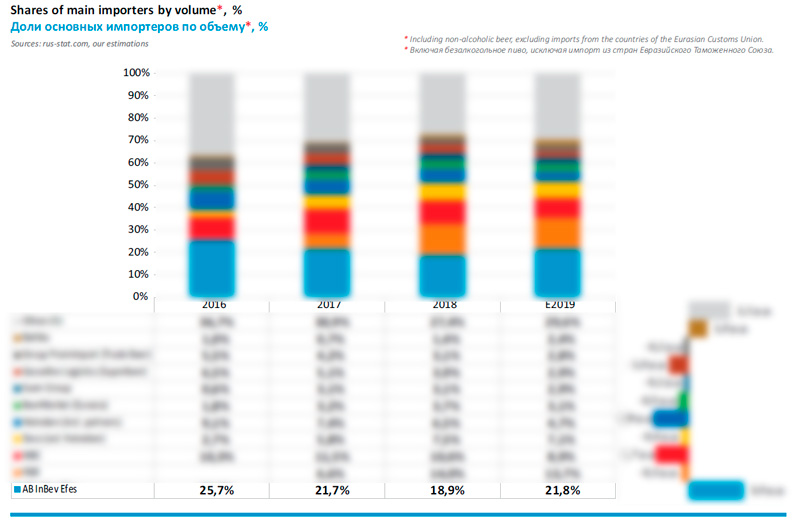

TOP-10 of Russian beer importers

Till recently, among the beer importers, there was a rapid consolidation. It seemed that international brewing groups and big networks as well as a dozen of independent importers would gradually conquer all other companies. Yet in 2019, the share of TOP-10 importers did not grow but declined by … p.p. which speaks for the fiercer competition. The import beer popularity growth, its endless variety of brands and the ruble revaluation attracted the attention of new participants having allowed a range of second row companies to get stronger.

Let us note that over 2016-2019, more than a thousand of businesses imported beer to Russia, but only 80 companies can be called more or less large, that in aggregate brought at least 500 000 l of beer into the country during those 4 years. Some of major suppliers were obviously one-time logistic partners of network distributors. Thus, so that the supplies fluctuations do not look too dramatic, we tried to take into consideration, who was the final recipient, judging by companies’ brands portfolios.

The key importer who mainly provided for the positive dynamics of 2019 is not difficult to determine, this is AB InBev Efes. According to rus-stat.com portal data and our estimations the company has by … increased their supplies from abroad (or by … mln l) to … mln l. By doing so, AB InBev Efes have tightened their grip on the leading position with a …% share of the general import segment* (+… p.p.).

* Here and elsewhere the market shares are cited taking into account alcohol-free beer excluding import from Belarus, Kazakhstan and supplies by Russian companies in Duty Free.

Let us note the that market share of AB InBev Efes is approximately equal to the aggregate share of the three other leading brewing companies – Heineken, MBC and Baltika that also belong to the list of major companies but are much behind the leader.

AB InBev Efes got in the leading position in one leap in 2014, as the import beer market was transiting to a deep crisis stage. At that time, AB InBev Efes reconsidered their strategy in Russia, its focus shifted to marginal brands and profit from every sold hectoliter. The dramatic sales decline even against the total market decrease was followed by the portfolio premiumization. So, the licensed beer at the moment of the alliance with Efes forming accounted for a bigger part of the company’s sales compared to other market leaders. In the current volumes of the joined group sales the import share by our rough estimation reaches …%. Compared to 2018, it has increased to … p.p.

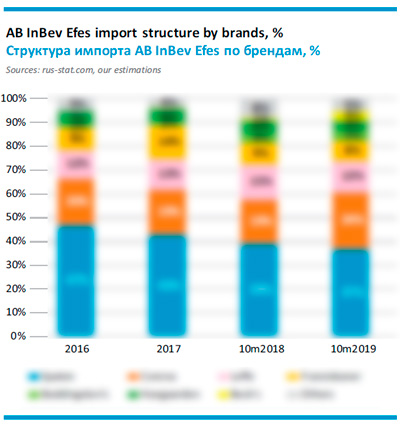

AB InBev Efes is importing more than 10 brands into Russia and virtually all of them gave positive dynamics in 2019. The biggest absolute impact was made by two major and popular brands that had been long known to Russian consumers, namely, German Spaten and Mexican Corona. Together they provided for 2/3 import volume of the company. Among other significant brands, there was a supply increase of Leffe, Franziskaner, …, and … while the supplies of … remained at nearly the same level.

AB InBev Efes is importing more than 10 brands into Russia and virtually all of them gave positive dynamics in 2019. The biggest absolute impact was made by two major and popular brands that had been long known to Russian consumers, namely, German Spaten and Mexican Corona. Together they provided for 2/3 import volume of the company. Among other significant brands, there was a supply increase of Leffe, Franziskaner, …, and … while the supplies of … remained at nearly the same level.

A rapid supply growth of British brand … (belonging to AB InBev) can be obviously explained by the fact that it is at the beginning of its expansion. German … supplies grew from almost zero, and to a large extent were supported by alcohol-free brand version (with blue label). Perhaps, the company have refocused from local production to import as despite the virtual disappearance from the market, Russian consumers still remember it.

Under our estimation, in 2019 alcomarkets network Krasnoe&Beloe (K&B) including its partners took the second position in the list of leading beer importers. This happened though the supplies volumes were growing slower than the import in general – by …% to … mln l. At the same time the group lost some of its share in the general supplies volume – … p.p. to …%.

As there appeared an alliance of (K&B) networks, Bristol and Diksi, the list of their suppliers widened. Besides, at different times (K&B) were getting beer from various companies. According to our estimation, now company Orbita is dominating with a …% share in the total volume having received the functions of Odyssey company (the both come from Chelyabinsk region). In order to estimate the alliance supplies dynamics one has to account the volumes of … affiliated independent logistic partners. Including BRL (connected to Bristol network) and Diksi Yug.

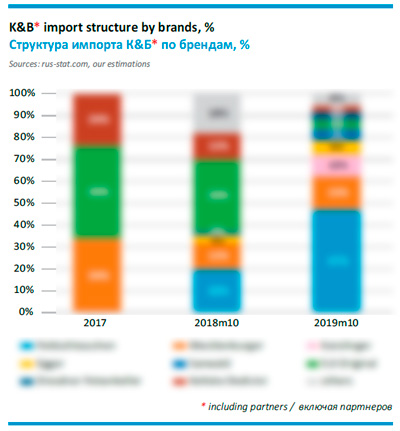

The import brands structure in 2018-2019 was much different. Perhaps, such changes resulted from marketing policy and the key brands rotation as the consumers’ interest to them goes down. For instance, in 2018 the bulk of import accrued to German beer 5.0 Original and Czech Keltske Dedictvi, yet in 2019 they decreased in … and … accordingly. Interestingly, almost all supplies volumes in 2019 of 5.0 Original was accounted not by partner firm K&B but by … that is obviously associated with the same-name network.

The import brands structure in 2018-2019 was much different. Perhaps, such changes resulted from marketing policy and the key brands rotation as the consumers’ interest to them goes down. For instance, in 2018 the bulk of import accrued to German beer 5.0 Original and Czech Keltske Dedictvi, yet in 2019 they decreased in … and … accordingly. Interestingly, almost all supplies volumes in 2019 of 5.0 Original was accounted not by partner firm K&B but by … that is obviously associated with the same-name network.

For K&B instead of 5.0 Original in 2019 a substantial volume of German beer Feldschlosschen was brought in, and the product range import increased almost … and the brand became the major one in the supplies structure. The supplies of German Mecklenburger, the second import brand by significance, continued growing. Two more brands were actively gaining weight in 2019, yet it is still unclear what are their growth prospects, they are German … and Austrian ….

Bristol network attracted attention by launching a private trademark Karolinger from Germany at the Russian market. OeTtinger, a well known for its expert focus company was chosen. In Karolinger there are no experiments and took the well-tried strategy employing the sights of German city and a sex-appealing female image, similar to other well-known private beer Prazacka.

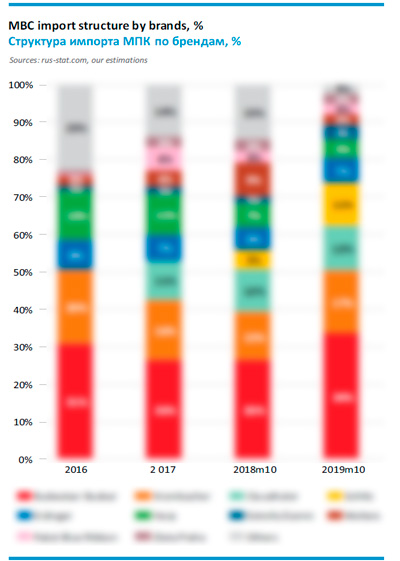

According to our estimation the import volumes of Moscow Brewing Company (MBC) in 2019 declined by several percent having amounted … mln l (and prior to that, there was a long period of dynamic growth). This meant that the company’s share in the general volume of supplies declined by … p.p. to …%.

MBC stands out among other importers by a very wide product range, under our estimation in 2019 the company imported at least … brands including … in the volume of more than 100 000 liters. Despite the big variety, the makeup of the key brands is quite stable.

MBC originally based its development strategy on creating a portfolio of authentic brands with a story, and focused on the premium segment. So, no wonder that the share of import in the total volume of the company’s sales is higher than that of other market leaders. Under our rough estimation in 2019, it … p.p. and amounted to nearly …%.

MBC originally based its development strategy on creating a portfolio of authentic brands with a story, and focused on the premium segment. So, no wonder that the share of import in the total volume of the company’s sales is higher than that of other market leaders. Under our rough estimation in 2019, it … p.p. and amounted to nearly …%.

The biggest and one of the oldest brands in MBC portfolio is still Budweiser Budvar. Its share at the market and in the company’s portfolio is fluctuating, yet according to the results of 2019, its supplies increased by …% having exceeded … mln liters. Besides, supplies of German beer Krombacher increased by nearly …% to … mln l. Exclusive rights for its distribution were received by MBC as far back as in 2015. The volumes of these brands were rapidly growing along with the import market recovery.

As for less significant brands, the supplies of German … that had been included into the company portfolio, reduced, and beer … lost a big part of its supplies. At the same time, there was a growth of … beer by partner in license production, namely American brewery …. Interestingly, beer by a famous British brewery BrewDog got the company’s portfolio, though its supplies are still not large.

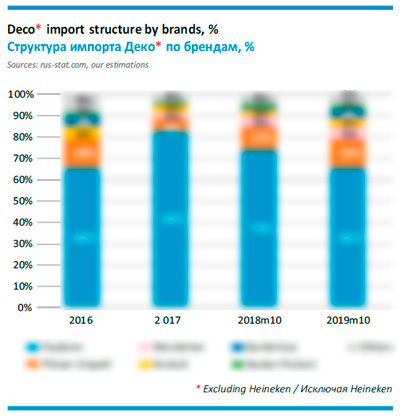

Company Deko is formally the second by supplies volume beer importer to Russia as by the end of 2019 they amounted to nearly … mln l. Yet, almost half of beer was meant for Heineken company and if we deduct these volumes, Deko will be on the fourth place with … mln l. However, even that beer could be imported by the company only as by a logistic and service operator (from Customs Federal service to Alcohol market regulation registration) selling ready-for sale production to final distributors of import beer.

Thus, under our estimation, in 2019 supplies of Deko went …% up to … mln l, and the share in the total import volume decreased by …p.p. to …%.

… of the volume (nearly …mln l) accrues to well-known German brand Paulaner and Deko is obviously the exclusive supplier of only packed beer as Paulaner in kegs is imported by another firm. The import of Paulaner …. At the same time, supplies of … beer went up, but its share in the total volume is still not large.

… of the volume (nearly …mln l) accrues to well-known German brand Paulaner and Deko is obviously the exclusive supplier of only packed beer as Paulaner in kegs is imported by another firm. The import of Paulaner …. At the same time, supplies of … beer went up, but its share in the total volume is still not large.

Along with production by independent German breweries, Deko is producing a range of famous European brands by Asahi company that used to belong to SABMiller. In the order of decreasing volumes they are Pilsner Urquell, …, …, … and title Asahi. All of these brands demonstrated a good growth in 2019. And in this case too one can speak of exclusive or priority rights for supplies, if we speak of the European part of Russia.

Interestingly, Deko went on accumulating the import of … German beer … despite the launch of license production at Heineken capacity.

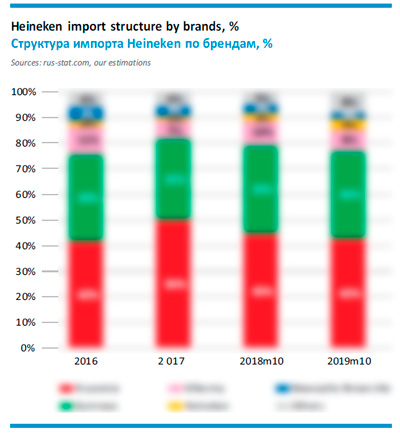

Russian division of Heineken in 2019 saw a substantial reduction in import beer output by nearly …% to … mln l according to our estimation. The reduction took place following a hike in supplies in 2018 and obviously, these drops are connected to preparation and launching of local production of foreign brands.

Against the two-digit rates of beer import growth in 2019, an abrupt reduction of Heineken supplies resulted in its share reduction by … p.p., to …%.

Heineken imports the bulk of beer not directly but through logistic partners. Till 2018, company … was involved in all aspects of import beer. Yet, in 2019 under our estimation, almost all outside supplies went to … company (it sent nearly …% of import Heineken to Russia).

Heineken imports the bulk of beer not directly but through logistic partners. Till 2018, company … was involved in all aspects of import beer. Yet, in 2019 under our estimation, almost all outside supplies went to … company (it sent nearly …% of import Heineken to Russia).

Supplies of draft beer is dealt by trade company BeerMarket, that is operating rather independently on the market, so, these volumes are accounted separately (see further).

There was a substantial decline in import volumes of the three leading key brands including those that are produced in Russia under the license. Beer Krusovice lost under our estimation …%, for instance sorts Imperial and Cerne that are still delivered from Czech Republic. Besides, the supplies of …, represented in import by … in kegs, fell by …%. Another … brand, … saw a …decline.

It is surprising that the narrowing of the import segment was taking place despite the mighty strengthening of the company’s positions in the premium segment of the Russian market, as in 2019 the sales of license title brand, besides, they got a license for production of Staropramen and Miller brands.

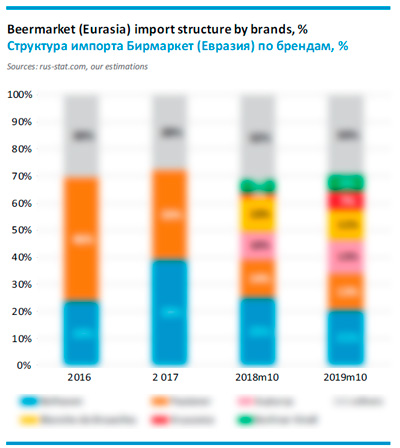

Company Beermarket (Eurasia) in 2019 kept its supplies volume at nearly the level of the previous year – about … mln l. according to our estimation. Nearly 100 sorts from many countries including expensive and special ones belong to the company’s product range. Beermarket is focused on supplies of draft beer (nearly …% of the total volume in 2019), developing partner’s chain in Russia.

Company Beermarket (Eurasia) in 2019 kept its supplies volume at nearly the level of the previous year – about … mln l. according to our estimation. Nearly 100 sorts from many countries including expensive and special ones belong to the company’s product range. Beermarket is focused on supplies of draft beer (nearly …% of the total volume in 2019), developing partner’s chain in Russia.

In 2019, the brand supplies dynamics in the company’s portfolio was multidirectional (which resulted in the general neutral dynamics). For instance, the supplies of famous brands by European breweries, namely, Scottish …, German … and Belgian …. At the same time, supplies of key import brands belonging to … went up. These are Czech Krusovice and British Newcastle Brown Ale. Let us remind that here we are speaking of draft beer.

Against the general growth of import to Russia, the share of Beermarket in its volume decreased by … p.p., to …%.

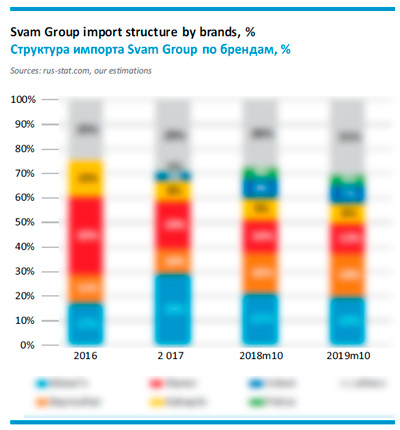

Svam Group is an independent and rather big player of the Russian market that appeared as far back as in 2005, resulting from joining of several distributors of draft beer. At its time, the company brought Staropramen and Krusovice to the Russian consumer, and in 2010 it became the distributor of glass by Sahm company, while in 2012 it launched a beer production of its own.

Svam Group is an independent and rather big player of the Russian market that appeared as far back as in 2005, resulting from joining of several distributors of draft beer. At its time, the company brought Staropramen and Krusovice to the Russian consumer, and in 2010 it became the distributor of glass by Sahm company, while in 2012 it launched a beer production of its own.

Svam Group’s variety is very big. The company declares 250 SKU of beer in its catalogue for 2019. Under our estimation, over the year it imported more than 40 brands by a host of European breweries, most of which belong to superpremium segment.

Most of brands have more or less increased by volume. Under our estimation in 2019 the general beer import volumes of Svam Group increased by …% and amounted to about … mln l. The company’s share in the general supplies volume remained at nearly the same level, that is, …%.

It is difficult to name the dominating brands with a big market share in the sales structure. There are three German brands with supplies volumes ranging 100 000 liters, namely …, … and … (… was growing especially dynamically). Though …% of sales are accounted by German brands, supplies and sales of Belgian, Czech and Lithuanian beer are rapidly growing too.

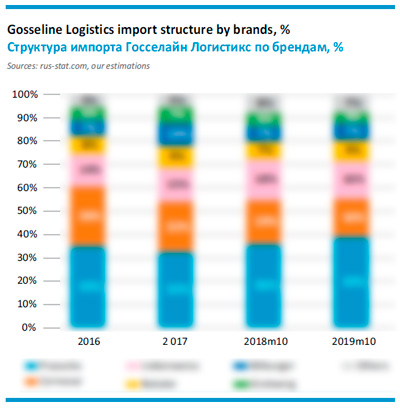

Gosseline Logistics (Superbeer) used to be known as state concern Russian tradition. Starting from 2000, the company was focused exclusively on supplies of import brands and quite successfully, having become a market leader in several years. Russian tradition became known as a pioneer of private import brands Prazacka and Cernovar from Czech Republic as well as Liebenweiss and Grotwerg from Germany. Besides in 2011 there started supplies of private brands of Bakalar beer from the company’s own brewery in Czech Republic Tradicni Pivovar v Rakovniku.

Gosseline Logistics (Superbeer) used to be known as state concern Russian tradition. Starting from 2000, the company was focused exclusively on supplies of import brands and quite successfully, having become a market leader in several years. Russian tradition became known as a pioneer of private import brands Prazacka and Cernovar from Czech Republic as well as Liebenweiss and Grotwerg from Germany. Besides in 2011 there started supplies of private brands of Bakalar beer from the company’s own brewery in Czech Republic Tradicni Pivovar v Rakovniku.

According to our estimation in 2019 the company decreased supplies of all their import brands considerably. That affected mostly …, … and …; …, suffered less and … remained at the same level. As the company focuses on its own private brands, the total decline amounted to about …% to … mln l according to our estimation. That also took the company’s market share …p.p. down, …%.

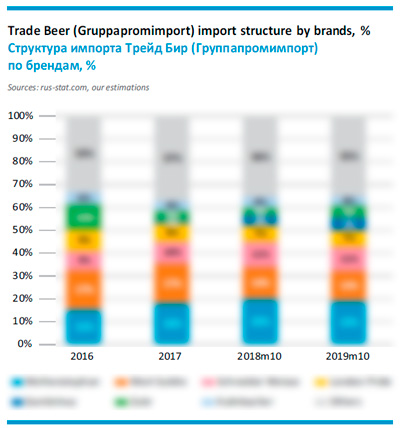

Trade Beer (Gruppapromimport, Group Promimport). Though we do not have data on any founder’s relations between the three companies, in 2019 Group Promimport stopped supplying many brands, while Trade Beer started, and before that a part of supplies was taken by company Gruppapromimport. Basing on this we will consider these supplies connected.

Trade Beer (Gruppapromimport, Group Promimport). Though we do not have data on any founder’s relations between the three companies, in 2019 Group Promimport stopped supplying many brands, while Trade Beer started, and before that a part of supplies was taken by company Gruppapromimport. Basing on this we will consider these supplies connected.

In 2019, under our estimation, the supplies volume of these companies went …% up to … mln l. Due to the exceeding import growth in general, the companies’ share declined by … p.p. to …%.

The product range of Trade Beer and Gruppapromimport is very wide and includes at least 30 brands of well known European breweries (German, Czech and Belgian brands in fine proportion).

The share of three key brands having nearly million liters, namely German … and … as well as Belgian … remained nearly at the level of 2018. In the … family the supplies of …grew while …on the contrary fell (in general +…%). There was a considerable increase of comparatively small by volume Czech brands …, … and ….

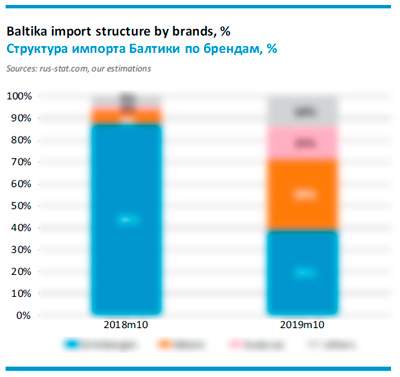

Company Baltika, that in 2019 attracted attention by considerable increase of import supplies, rounds out the leading ten. Under our estimation, these supplies grew … reaching …mln l of beer. Accordingly, the market share of the company increased by … p.p., to …%.

Company Baltika, that in 2019 attracted attention by considerable increase of import supplies, rounds out the leading ten. Under our estimation, these supplies grew … reaching …mln l of beer. Accordingly, the market share of the company increased by … p.p., to …%.

The biggest brand in the company’s import portfolio with a share of …% is still beer …. However, its supplies compared to 2018 remained almost the same. This brand appeared at the Russian market 6 years ago and strengthened the company’s positions against the popularity of Belgian abbey beer.

There was an unexpectedly rapid growth of Latvian Aldaris (…) and Lithuanian Svyturys (…) – by breweries that also belong to Carlsberg Group. Until now a lot of independent importers were dealing with distribution of affordable beer from the Baltics with a success (for example LSV Trade company).

Obviously, the growth of this segment attracted Baltika that currently badly needs stronger portfolio due to sales decline of mass brands. Baltika took up a similar tactics with brand Minskoe Zhigulevske, that in its day gained a considerable market growth, due to the interest to Belarus products and nostalgic sentiments.

Let us note that among the market leaders, Baltika has the smallest share in the sales structure. In 2019, it grew by … p.p., to …%.

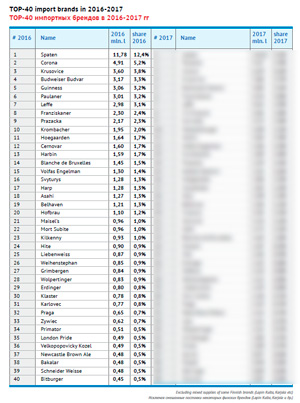

TOP-10 import brands

In this chapter we will turn over our analysis, looking at the import beer market from the point of view of the key brands. In the first dozen, four brands belong to AB InBev Efes, which is still ahead of its competitors.

Besides, the better half of places in TOP-10 is taken by brands from Germany, yet even basing on this short list one can tell that more expensive “monastery” brands are behind less expensive ones.

At the same time, the aggregate share of updated TOP-10 in 2019 increased by … p.p. to …%, not taking into consideration the brands of customs union and accounting alcohol-free brands. This took place in spite of market share decrease trends of the leading importers.

Brand #1 Spaten

Brand #1 Spaten

In 2019: the supplies volume~… mln l; growth +…%; share …% (+… p.p.)

Country of origin – Germany; producer – Spaten-Franziskaner-Brau (AB InBev).

Distributor: AB InBev Efes.

In 2014 AB InBev company got exclusive rights for Bavarian beer Spaten distribution in Russia. It had been familiar to Russian consumer, yet employing a powerful distribution network and rather affordable price allowed the brand to become the leader in 2015. These stages were a logical result of one of the biggest breweries, namely, Spaten-Franziskaner-Brau GmbH, being a part of AB InBev. In 2019, Spaten resisted new competitors from Germany that were even more affordable by price, went on exceeding the import in general and increasing its market share.

Brand #2 Feldschlosschen

In 2019: the supplies volume~… mln l; growth: … times; share …% (+… p.p.).

Country of origin – Germany; producer – Feldschlosschen AG.

Distributor: Krasnoe&Beloe

Until 2018, virtually nobody in Russia saw German beer Feldschlosschen by same name brewery. But the wave of its supplies was gaining impetus, at the end of 2018 it took the fifth position and in 2019 moved to the second place. At the same time there was a sharp decline of 5.0 Original brand (by OeTtinger group), that also in short time transited from complete absence at the market to the third position in the leaders’ list. By essence, one powerful import flow turned into another one. Obviously, that change is connected to rotation of the key import brand in the major chain of alcomarkets Krasnoe&Beloe. Unlike other foreign brands, Feldschlosschen is well represented everywhere in Russia.

Brand #3 Paulaner

In 2019: the supplies volume~… mln l; decrease: …%; share …% …p.p.).

Country of origin – Germany; producer – Paulaner Group (Brau Holding International).

Distributors: Deko (…%), BeerMarket/Eurasia (…%).

Paulaner is one of the oldest and most famous import brands at the Russian beer market. It’s promoted by 13 Paulaner restaurants opened by franchise in different Russian regions. Here consumers can get to know the draft version of the brand (sometimes, brewed at the restaurant brewery). However, comparatively high retail price of Paulaner makes it vulnerable to competitive activity of the key importers in the German beer subsegment. Following a substantial growth in 2017-2018, the brand’s supplies volume and market share went down considerably. Paulaner’s key distributors have specialization, the bulk of beer is delivered in can or glass bottle by …, and a minor volume is imported in kegs by ….

Brand #4 Corona

In 2019: the supplies volume~… mln l; growth: +…%; share …% (+…p.p.).

Country of origin – Mexico; producer – Compania Cervecera Del Tropico (AB InBev).

Distributor: AB InBev Efes

Corona Extra is an export-oriented brand, that until recently was produced only in Mexico. Corona belongs to TOP-5 most sold beer sorts in the world and it is currently the most intensively growing beer among the three global brands by AB InBev (there are also Bud and Stella Artois). The brand has got these privileges due to wide distribution, marketing support and price control. Unlike most other import brands, Corona’s market share is rather evenly allocated among regions, for example, the shares in Moscow and Yekaterinburg do not differ much. All that resulted in a long standing growth trend of import supplies.

Brand #5 Leffe

In 2019: the supplies volume~… mln l; growth: +…%; share …% (+… p.p.).

Country of origin – Belgium; producer – Brouwerij Artois (AB InBev).

Distributor: AB InBev Efes.

Leffe brand is the biggest abbey-originated sort sold in Russia. Though the sort can be attributed as superpremium and niche, due to the popularity wave of such beer, its sales were growing notably. Blonde and brune Leffe sorts are imported to Russia, in nearly equal proportion. Following a sharp supplies growth in 2018, during the past season, they were growing a little faster than the import in general. In Moscow and Saint-Petersburg, Leffe’s market share equals nearly …% and it is much lower at the regional markets. The bulk of beer is sold in supermarkets, though nearly …% is delivered in draft obviously to HoReCa. By the way, in order to support all Belgian brands, AB InBev Efes opened restaurant Leffe Café in Moscow in 2019.

Brand #6 Volfas Engelman

In 2019: the supplies volume~… mln l; growth: +…%; share …% (+…p.p.).

Country of origin – Lithuania; producer – Volfas Engelman (Olvi).

Distributors: LSV Trade (…%), Pintaclub (…%), Sommelier (…%), Lithuanian Khleb (…%) .

Volfas Engelman is the title brand by same name Lithuanian brewery. The title brand, eye-catching package design with protective lid from tin on the can, as well as a big range of classical and original tastes attracted lovers of import beer. Pyaterochka chain provided for the distribution as it introduced the brand into its list 4-5 years ago. Though the retail price for Volfas Engelman was not low (except for frequent promotional offers) its popularity was growing very rapidly and in 2019 the rates of supplies went on twofold exceeding the average ones. About ten companies are involved in Volfas Engelman import, yet there are not many large companies among them: … delivers the bulk of packed beer to retail networks, while … and … import beer in kegs.

Brand #7 Budweiser Budvar

In 2019: the supplies volume~… mln l; growth: +…%; share …% (-… p.p.).

Country of origin – Czech Republic, producer – Budějovický Budvar (state enterprise).

Distributor: Moscow Brewing Company

Budweiser Budvar is well known as an export-oriented state Czech beer producer. But in Russia this brewery is especially well-known due to deep historical roots. Obviously, the brand of “national Czech flag colors” is mostly preferred by older generation, that associates the image of Czech beer to Budweiser Budvar. At the beginning of the noughties, a company connected to MBC was its key importer, later, MBC became its exclusive importer. Accordingly, Budweiser Budvar, is best represented in Moscow, and the Central region of Russia. The brand supplies volume was rapidly recovering after crisis 2015 and reached the peak in 2018, at that time Budweiser Budvar became the leader among Czech import brands. In 2019, one could speak of stabilization of the supplies dynamics.

Brand #8 Krusovice

In 2019: the supplies volume~…mln l; growth: -…%; share …% (… p.p.).

Country of origin – Czech Republic, producer – Heineken Česká republika (Heineken).

Distributor: Heineken Russia

Only ten years ago, Krusovice was not only the most popular Czech beer in Russia, but also left far behind other leaders of import brands list. However, as license production was started, “royal” beer settled into a new orbit which became a logical result of the Czech brewery entering Heineken Group. As of now …% of Krusovice sales is accounted by beer of local production and only several special sorts are imported: Imperial, Cerne, Rizna 10 and Kralovska 10. They are comparatively well represented all over Russia completing the main lager, but …. Let us note that such mix of license and import sorts of one brand is rather unusual for the Russian market and is not used so widely (except for alcohol-free versions of the main brand).

Brand #9 Mecklenburger

In 2019: the supplies volume~… mln l; growth: -…%; share …% (… p.p.).

Country of origin – Germany, producer – Darguner Brauerei (Harboes Bryggeri).

Distributor: Krasnoe&Beloe

Beer Mecklenburger is packed at export-oriented brewery Darguner, which belongs to Dutch group Harboes Bryggeri. In Russia alcomarkets chain Krasnoe&Beloe represented this beer to its clients in 2017. Mecklenburger is currently delivered only in can in three sorts. Immediately after launching due to low price and wide distribution the brand got into the first dozen, but it is not growing as intensively as 5.0 Original, which appeared at nearly the same time. Yet judging by further supplies growth, in 2019 Mecklenburger is still a promising market player.

Brand #10 Franziskaner

In 2019: the supplies volume~6mln l; growth: +…%; share …% (… p.p.).

Country of origin – Germany, producer – Spaten-Franziskaner-Brau (AB InBev).

Distributor: AB InBev Efes.

Franziskaner is the third by size import brand which appeals to church images and exclusively delivered by AB InBev Efes. In the company’s import product range, it resides on the top price floor, distancing from a more popular Spaten, so despite a comparable distribution level, Franziskaner’s market share is much lower. Obviously, due to the growing competition in the German subsegment the growth rates of Franziskaner supplies were moderate, though exceeding import in general.

To get the full article “The market of import beer in Russia” in pdf and database in xlxs (14 pages, 15 diagrams, 2 tables, 139 344 records in database) propose you to buy it ($50) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.

The article materials were prepared using statistics of import supplies provided by rus-stat.com portal. Data from Food and Agriculture Organization of the United Nations as well as national statistics service Rosstat were also used in the article. A number of estimations are based on info provided by importers, beer producers and research companies.

The data on beer import volumes in 2019 are calculated basing on statistics for the first 10-11 months of the year. Data interpretations are our assessment based on the current trends in case the source has not been named.

We do not claim the given information to be absolutely correct, though it is based on data obtained from reliable sources. The article content should not be fully relied on to the prejudice of your own analysis.