In 2021 Russian breweries have not lost their consumers, it even turned out that they started drinking more beer at home and more often. The market has held the high bar of the previous season, yet now it is growing by value and polarizing by price segments. The competition in the market has been determined by Carlsberg Group (that has regained its volumes, having sacrificed the margin) as well by rapidly growing private labels and import. In those conditions, AB InBev Efes and MBC demonstrated a good stability, while Heineken was reluctant to lose profitability and lost some of its share. The regional breweries in the east of the country also yielded their positions.

Reinforcing of unexpected gain

Beer market trends

Import beer market

Beer keeps the consumer

Leading companies and their brands

AB InBev Efes

Baltika, Carlsberg Group

Heineken Russia

Other brewers

Reinforcing of unexpected gain

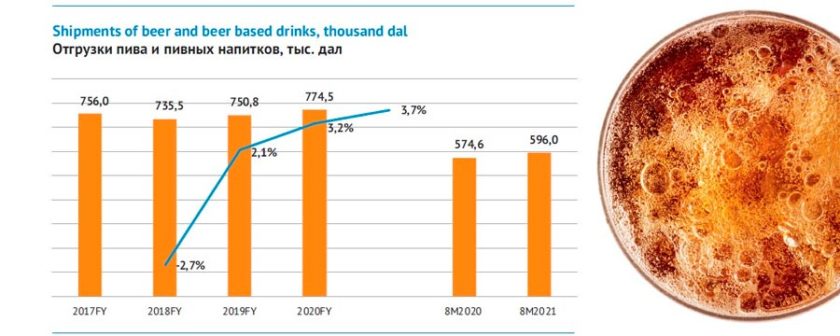

In 2021 there has been a growth of the industry and the beer market. Early in the year, the rates of shipments were very high, which is fully attributed to the low-base effect. In the second year of the pandemic major brewers felt much more confident than at the beginning.

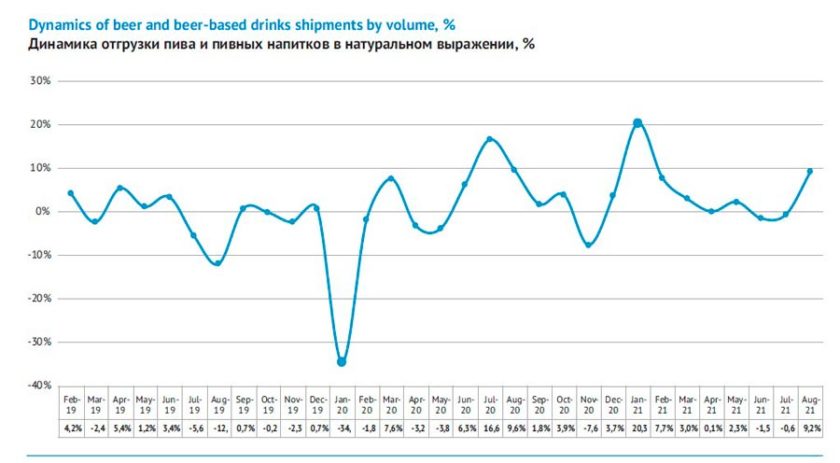

Yet it was more difficult to go through the summer season with the same positive dynamics. The summer of 2020 was hot, and the isolation was another growth factor promoting beer consumption. Beer sales in June-August 2020 were record-breaking over the previous three years having increased by 6.2% as observed by NielsenIQ.

However, in the first 8 months of 2021, according to Rosstat data, the beer and beer drinks shipments sped up by 3.7%. As shipments are prone to non-market fluctuations, the retail audit data by NielsenIQ are more representational. They speak of neutral dynamics of beer sales (+0.9%) in the first half of 2021. However, by the end of the hot season, NielsenIQ announced that the demand for the “summer” products turned out to be higher than that we could have if the temperature was average for the past several years. The sales of seasonal goods started growing actively from early June reached its peak in early July, and by August, they turned downward. Thus, in Moscow the demand for beer was 8% higher than expected in June-August. In Saint Petersburg, the beer sales exceeded the prognosis by more than 9%.

Thus, at the moment of the article preparation, one can say that in 2021 there have been unexpectedly high results of consumption, sales and beer production. By the end of the year, we are likely to see 1-3% dynamics.

By value the retail sales in the first half of 2021 increased by 3.5% according to distributors’ data. Volumes were left behind by money which took place due to increase of the average price for beer. Probably, by the end of 2021, the sales by value will grow further.

Let us analyze the beer market and the price fluctuations in more detail.

Beer market trends

Retailers and brewers in business press reported on bigger volumes of one-time beer purchase, as consumers started to stock up on beer in order to drink at home. As we will show below, since the pandemic start, there has been a polarization in consumers’ attitude to alcohol. Though the number of people who avoid alcohol has been increasing, home consumption has made a part of its lovers more active.

But unlike other consumer goods, even when beer consumption in 2020 rose unexpectedly, the high demand was not accompanied by retail price increase. It was twice slower than the official inflation rate (+6.5%), published by Central Bank. Specialists of the regulator explained that increase by bigger consumer demand. However, because of too much competition at the beer market, it did not comply with laws of demand.

Carlsberg Group’s intention to restore the volumes by promotional activity as well as the growth of private labels mainly led to price fixation. Increase in prices was not observed till 2021. Spring publication data by Nielsen IQ describe the drivers of this change.

On the one hand, the share of beer that is sold with special offers has declined sharply. In the modern trade it amounted 47% over the period March 2020-April 2021 (MAT in the graph), though in the same period last year it grew to 54%.

The second trend, which has not yet stopped and positively effects prices is change in the structure of beer sales by origin. Thus, import beer demonstrated the highest growth rates. Over the considered period, its sales have increased by more than 30% and the import share in the general structure has gained 4.6%. The development of the import segment will be considered a bit later.

According to Nielsen IQ, canned beer volumes went on increasing having pressed out glass bottle and PET.

According to messages from AB InBev, Carlsberg Group and Heineken, in 2020 and in the first half of 2021, there has been a further growth of market share of non-alcoholic beer, fruit-flavored beers (Essa, Seth&Riley’s Garage, Dr. Diesel Mix etc.) as well as many special sorts.

Bigger home consuming of beer instead of going to a restaurant has become an obvious trend among Russians. According to assessment done by Carlsberg Group over 2020 HoReCa segment in Russian went 36% down. However, even prior to the pandemic or quarantine, the share of beer sales in bar and restaurant segment had been estimated by many market players at 3-5%.

The beer market fragmentation according to Nielsen IQ has been growing in the long-time trend. Major producers still lead the market by sales, however there have recently appeared a lot of players. As for the product range, the share of the major brands (that are mostly owned by leaders) has been constantly shrinking.

In our estimation based on distributors’ data, further growth of superpremium beer (mostly import one) has become the main trend of price segmentation of the beer market. However, even such a sharp growth of superpremium beer has not strongly influenced the market due to its low absolute figures.

As there has been the biggest sagging in the middle-price segment, one can speak of market polarization trend in beer consumption given the comparative stability of economy and premium segments.

Thus, the economy segment by volume remained at nearly the same level in the first half of 2021. Yet by value, it lost … p.p. of sales. We consider beer costing up to 85 RUB/l to belong to the economy segment.

Inside the segment, brands with “spread” attribution are taking the lead. Thus, the vast mass of regional and national brands was much squeezed by chains’ private brands. The average price for private labels is lower than most of economy brands. Their share increased by … p.p. over the year.

Chains enjoyed a big growth at the pandemic start and this was a driver for private labels increase. This is because consumers came to supermarkets instead of making impulsive purchases. However, then, during 2020, the demand shifted to chain and non-chain shops “near home” and the share of big chains (hypermarkets) started decreasing.

Besides, as one could expect the market share of those few brands that made the best offer has grown.

In the first place, it is the most popular version of … by …which is even cheaper now and has reinforced its number 2 brand position (after …). Certain regional brewers have also managed to increase their market share.

The economy segment remained at the same level as the “winners” took sales from other economy brands by AB InBev Efes, Heineken, Carlsberg Group, Trekhsosenskiy and Ochakovo as well as from regional breweries.

Besides in the first half of 2021, the mainstream segment sagged by …%. This is where we place beer costing 85-110 RUB/l in retail.

As always, let us note that narrowing of the mainstream is connected to years-long decline in consumers’ loyalty to federal brands. They win back from time to time. Yet, if we look at the long-term trend, we will clearly see deterioration of prior and present megabrands.

The mainstream would have dropped much more if not for share recovery at the biggest Russian brand … (it has grown … p.p.). This can be explained by promotional activity by the company reacting to a riot growth at many competing brands by … in the previous season.

Some big license brands that were gradually shifted by the market leaders (e.g. title … and …) into the mainstream segment in order to support sales are losing their shares, which certainly raised a red flag when we look at the mainstream segment development. Besides, even for modest growth license brands need a sharp price cut like for example … beer which from premium has become virtually mainstream.

A negative impact into mainstream segment was made by regional breweries (… p.p.). … of their production can be now fitted into the diapason 85-110 RUB/l. There was a time when regional brewers felt at home in the market of cheap beer but currently they are being pressed out of there by the market or private labels. For comparison – the share of regional players in the economy segment of retail declined by … p.p. though it had not been very high.

In this context one can understand the conflict between the “Union of Russian brewers” that joins regional brewers and the market leaders who founded “Association of beer producers”. Many breweries with Russian capital lobby for introduction of fixed minimal retail price (MRP) for beer and international companies are for market price regulation.

The market leaders admit that their beer cost price can be lower due to big output volumes. So, they can offer consumers more attractive prices. But they warn that MRP will make consumers pay more for the product which will affect the demand and the industry dynamics. The state budget will suffer if the excise inflow goes down.

The market share of the premium segment is at the level of …% for the third year running though there are considerable fluctuations of many brands’ shares going inside. We consider beer costing 111-160 RUB/l to be premium. For the most part the segment is formed by license beer of Russian origin, or to be more exact by a part of it as license beer is growing more separated by price levels.

The share of … premium beer has been increasing at stable rate, yet this company does not play a major role in the market of expensive beer. That role is taken by …, which though made the main contribution into the segment dynamics, but some its premium brands on the contrary had their market share declined. Russian subdivision of … also had a very uneven sales dynamics. The shares of some brands have skyrocketed against the distribution or drop in prices while other brands experienced decline, yet the final balance was negative. The brands by regional and craft breweries are ever more outstanding in the market of premium beer.

Superpremium segment of the market proved to be the most dynamic both in absolute and relative figures. We consider brands costing more than 160 RUB/l (with the average price exceeding 180 RUB/l) to be superpremium. In the first half of 2021, the segment gained … p.p. by volume, yet by value it grew more than twice and nearly reached …% of the market.

The superpremium segment is in general formed by import beer, though there has been a slow expansion of Russian craft brewers to supermarkets.

On the regular basis about a third of retail sales of import beer is accounted by AB InBev Efes, that owns major import brands. The leader relies on its mighty distribution network and does not intend to yield the share to other providers. However, there is a growth of diversity both in importers and product range.

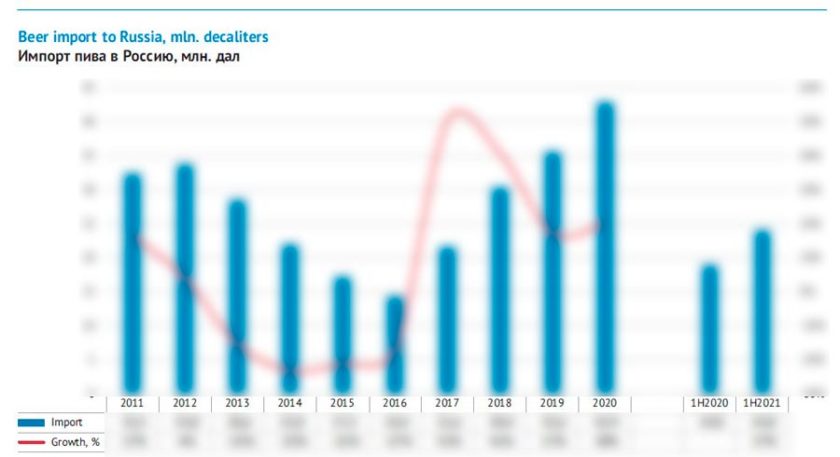

Import beer market

According to Federal Customs service, the growth of alcoholic beer import in the first half of 2021 sped up and reached …%. However, the growth rates had been two-digit before for 4 years (starting from the moment when Ukrainian beer shipments were banned). The import increased its market share from … in 2016 to …% basing on the trade balance on beer.

High demand for beer brewed abroad is confirmed by retailers, importers and the market leaders that were polled by RBC (see below).

According to NielsenIQ representative, Pavel Funtikov the sales of import beer are growing, as the consumers on the one hand have higher demand for niche local products which are considered as more “qualitative”, on the other hand, because now there are more such brands in retail.

Thus in “Ashan” this trend was reflected in the product range of Moscow hypermarkets as there appeared “Beer boutiques” with more than 200 import sorts.

The pandemic-related restrictions led to a demand jump for the import beer category on 2020, as Andrey Gubka, head of Russian Association of beer producers says. He reminds: during the COVID years, bars and restaurants in many Russian regions did not work for some time or worked with restrictions so people who had preferred to drink import beer at bars, were buying it in retail.

The sales in bars had started to decline even before the lockdown and in March there was a panic as “nobody was coming around”, Vladimir Postnichenko, co-owner of a range of Belgian pubs Kwaklnn in Petersburg said. “People who understood much about beer, had nowhere to drink it, so they were buying it at beer stores as they probably thought that it was safer”.

One more reason is a sharp decline of tourist trip abroad among Russians in 2020, as Alexey Vorobiev, representative of Russian office of Heineken thinks.

The price policy of foreign brewers could have been another growth factor of demand for foreign beer in 2020 according to RBC speakers. Due to the lockdown local brewers were in difficult situation: restaurants and bars were closed, there were no tourists, so “they were happy with any sales and offered favorable terms at export prices” RBC source in the brewing branch noted. In 2020 expensive import became more affordable due to flexible price policy of brewers, Oraz Durdyied, AB InBev Efes representative confirms.

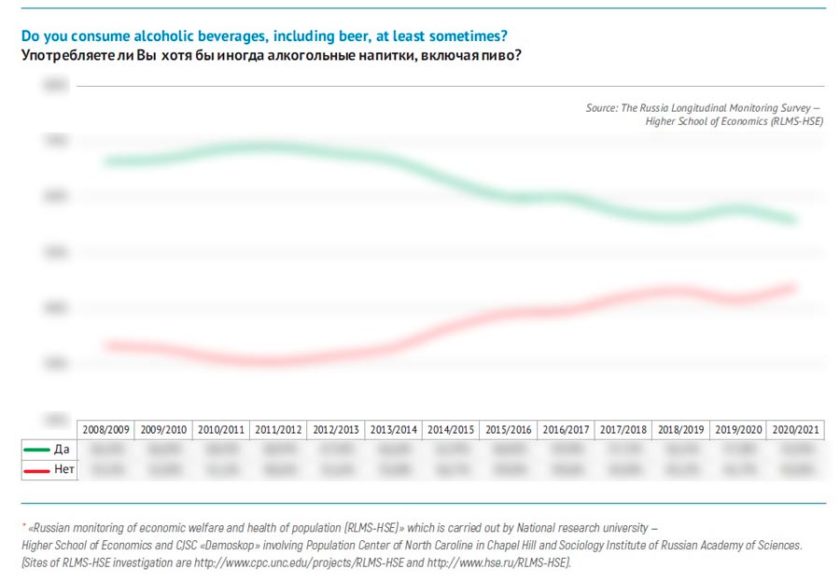

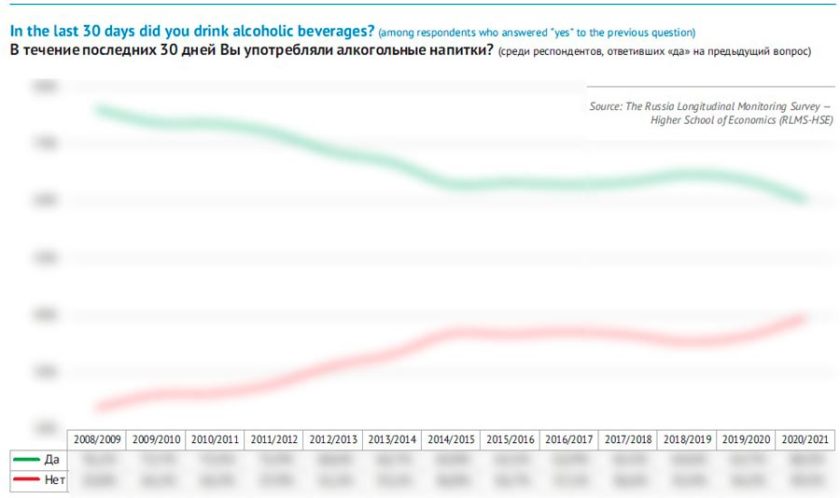

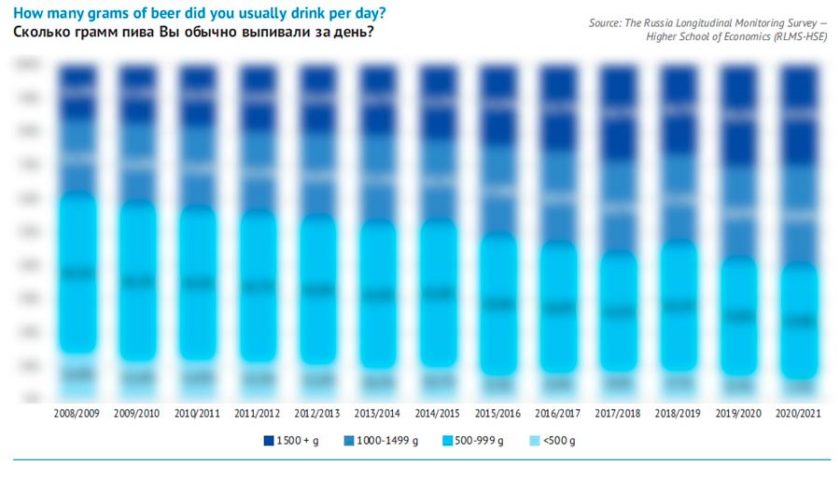

Beer keeps the consumer

Unexpectedly high sales in 2020 that were at least retained in 2021, are connected to change in consumer’s behavior caused by pandemic, remote working and introduction of restrictions.

Which exactly changes in the consumer’s behavior took place we can learn from annual survey data RLMS-HSE*.

* “Russian monitoring of economic welfare and health of population (RLMS-HSE)” which is carried out by National research university – Higher School of Economics and CJSC “Demoskop” involving Population Center of North Caroline in Chapel Hill and Sociology Institute of Russian Academy of Sciences. (Sites of RLMS-HSE investigation are http://www.cpc.unc.edu/projects/RLMS-HSE and http://www.hse.ru/RLMS-HSE).

The latest stage of surveys was carried out at the end 2020 in the low season like all previous surveys. The number of respondents who unambiguously answered questions on beer consumption amounted to 10 286 people. The respondents who admitted consuming alcohol (…% of the total number) were then asked if they drank anything alcoholic within 30 days. And after that, those who positively answered to this, were asked what exactly they drank, how often and how much.

The growth in number of people who do not drink alcohol at all was a mighty trend that had been active until a recent time. Their share in 2011 was …% and reached …% in 2018. The reasons for such a drastic change have been analyzed in prior issues. In measurable figures there was a decline in consumers as loss of elderly generation is ever weaker compensated by the youth.

“Decreases in adolescent weekly alcohol use in Europe and North America: evidence from 28 countries from 2002 to 2010” Published by Oxford University Press on behalf of the European Public Health Association. Eur J Public Health. 2015 Apr;25 Suppl 2:69-72. doi: 10.1093/eurpub/ckv031.

The authors based on sociological research (Health Behaviour in School-Aged Children). It was noted that even in countries of Eastern Europe, where over the period 2002-2006 there was a stable growth trend of alcohol use among school children, in 2006-2010 weekly consumption of alcohol declined from 12.3 to 10.1%.

The role of alcohol as a means of communication was becoming less important, they got alternative psychological stimulators (computer games, social media etc.). Besides, a certain role is played by healthy lifestyle popularization and the notion that alcohol affects the social standing.

Covid-19 has seemingly ruined that trend. The changes in people’s lifestyles have for the first time in many years led to smaller number of those who reported not drinking at all. And that reduction could not be explained by a sampling error. By 2021, the share of not drinking people did increase, but did not reach the level that could be expected by extrapolation of then existing trend.

Yet if we do not look so technically, we will see only a place swap of similar groups. Apart from people who do not drink at all, RLMS has a subgroup of people who do not turn down alcohol completely but have not drunk it for 30 days by the moment of the survey. The share of this subgroup among “drinkers” had been practically the same for a long time, but among all respondents it was declining along with “drinkers”. However, as the pandemic developed, the number of “non-drinking but non- abstainers” grew sharply. In the essence, this trend took place of the growth in abstainers’ number.

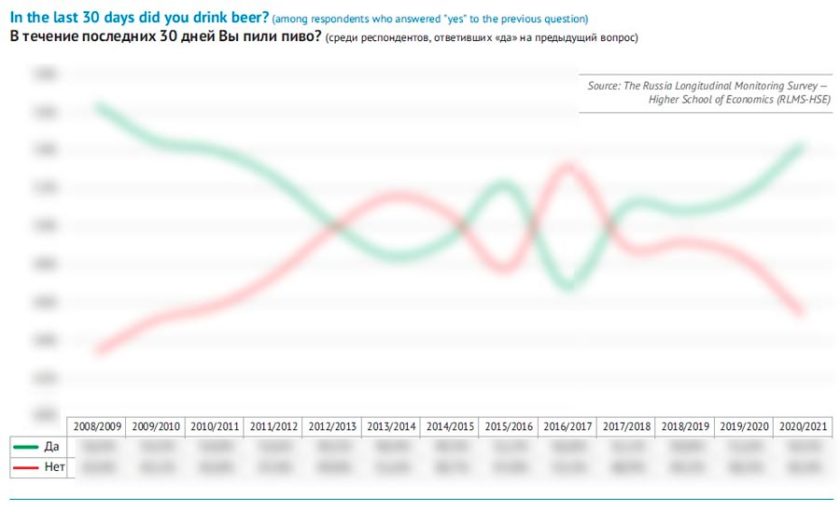

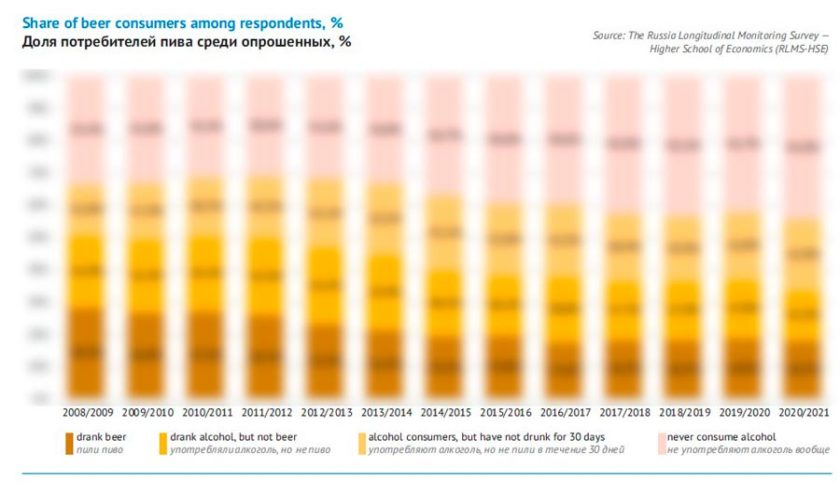

So, by the start of 2021, the number of people who have not used alcohol increased. Yet why has the beer market remained at a rather high level of the previous year? That is because the number of people who have drunk beer fell less than of those who have drunk any type of alcohol (any other alcoholic drinks).

However, if the reduction in number of those who drink beer took place, why don’t we see a decline in beer sales in 2021? RLMS can answer this question too, if we analyze how often and how much of beer people consumed. These changes brought about by the pandemic favored brewers.

Obviously, the volume of consumed beer is a simple figure obtained by frequency of consumption multiplied by a one-time volume of consumption. These data are certainly not absolutely correct, as they are registered basing on personal estimations of respondents. Yet such data were sufficient to reflect the previous fluctuations on the beer market (for example, the turning and decline before 2008).

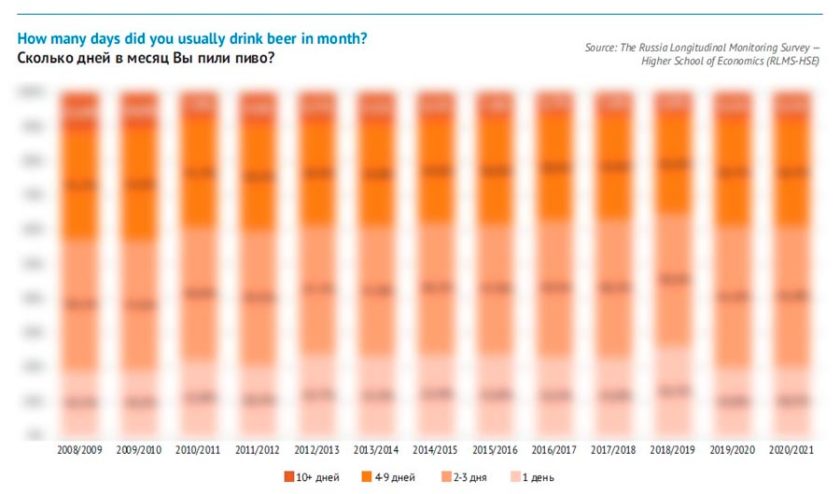

Though there has been a decline in number of alcohol-drinkers, at the same time, the core of “heavy” drinkers who drink a lot at a time has become more obvious. These are the consumers who raise weight of natural volumes of the market. The process of consumer number decline and the core “crystallization” was most active in 2014-2018.

At the end of 2018, according to the survey the share of nondrinkers or those drinking little grew unexpectedly. But in 2020-2021 the structure of consumption restored – people started drinking more at a time.

As for the frequency of beer consumption, until recently, one could clearly see a downward trend. It reached the lowest point in 2018/2019. At that time, the share of people who drank beer only once over that month reached a … of all consumers. Besides, all other groups of people drinking comparatively seldom or often decreased too.

The coronavirus pandemic start curbed that trend as the frequency of beer consumption started growing. The share of those who drank beer once a month fell to a level unseen for 10 years. The share of all other groups who drank beer more often rose. Yet, certainly, the share of active beer consumers is not as big as 10 years ago.

Leading companies and their brands

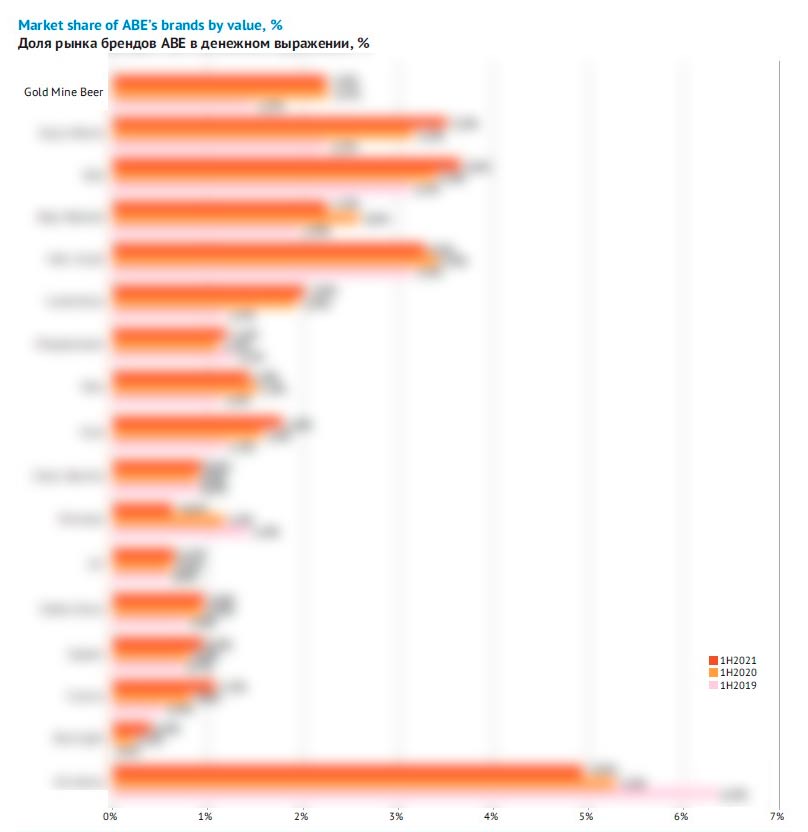

AB InBev Efes

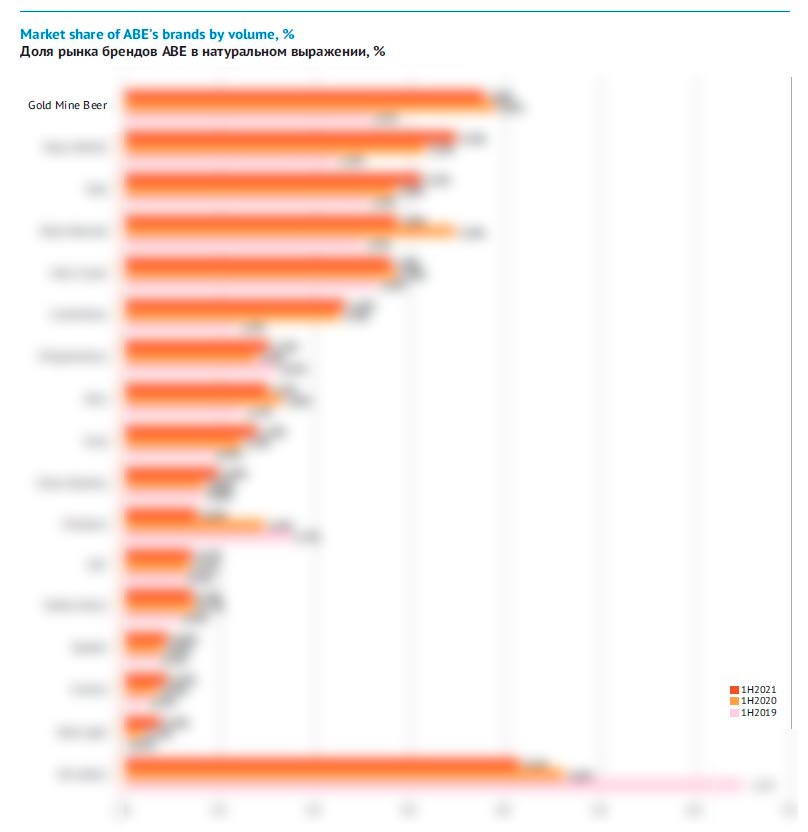

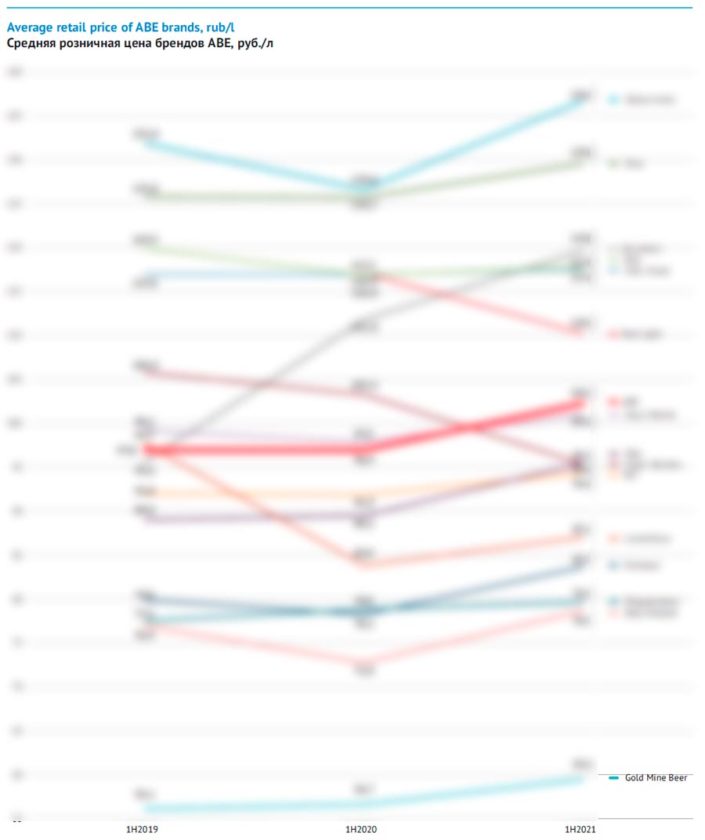

The performance of AB InBev Efes over the first half of 2021 can be called neutral and one can assume that the company has reinforced the result got in 2020. The volume growth during 2016-2020 was to a big extent achieved by lower retail price for beer (because of price competition and activity in the economy segment). So, the share by value did not grow until 2020.

In the first half of 2021, a minor correction of natural volumes took place against neutral dynamics by value. The company did not decrease the average retail price of the key brands as their main competitor, but on the contrary raised it. Besides, the stake on the superpremium brand and import brands has obviously been reasonable. Though we cannot say that the marketing focus of the company shifted towards expensive beer.

Besides, the optimization process of the brand portfolio, which the company received after the merging, is almost complete, so outsiders’ share decline does not much affect the final performance.

In the first half of 2021, AB InBev Efes share sagged considerably in the … segment of the market. While … was declining prices and chains’ private labels were expanding rather actively, AB InBev Efes on the contrary followed the inflation.

The company increased the retail price for its biggest and very affordable brand … as well the price for brands with borderline positioning, namely … and …. All mentioned brands lost some of their shares, though … due to uniquely generous offer almost kept its share. Let us add that the share of … has been declining for a long time – one can hardly notice the former mainstream leader on retail shelves.

At the same time, AB InBev Efes raised the price for … very carefully, as that sort became the sales engine for …and currently sets the price level and the difference in prices is becoming ever more obvious. Such tactics gave results as only … has grown in the economy part of … portfolio.

Unlike cheap beer, most of mainstream brands of the company have increased their market shares. And that happened not due to special offers as the growth by value was not slower than that by volume.

For example brand … went on growing steadily, mainly due to the most popular brand …. This development was not stopped by its main competitor’s enforcement in the mainstream segment.

The share of licensed Lowenbrau had some growth and there was a considerable contribution from the alcohol-free version of the sort. In general one can say that … has stabilized its positions after a sharp cut in the price in 2020 which led to its market share doubling. This brand may have been filling the niche which became vacant after … left the portfolio. Yet title beer … experienced competition in the niche of licensed beer. A minor decline in its share was compensated by some growth of brands … and ….

In the premium segment the development of brands by AB InBev Efes was uneven but in general positive. The company currently accounts for more than … of sales of premium Russian beer.

Having a rather reasonable price policy and obvious strategic focus, the share of key global brand beer … was still increasing. In 2020 it became the leader at the marginal beer market. Accordingly, the shelf neighbor beer …in 2020 stopped being the major license brand and in 2021 it has even lost some of its market share.

Bud Light that appeared on the shelves in March 2020, has crossed … mark by mid 2021. This beer is positioned as an independent product but not a light version of the favorite. According to the company’s estimation in the USA Bud Light is the absolute leader having up to 28% if the market.

In Russia the brand is focused on nearly 28% of the expressive youth audience and bases its promotion on humor and cyber sport. Possibly unusual design, global popularity and recognizable name multiplied by major distributing network of the company will be preconditions for further growth of the new product. Besides, the average retail price of Bud Light has been rather democratic for a license beer (lower than for … beer at the border with the …).

… beer … showed a good growth in the first half of 2021 to some extend due to alcohol-free sort. And the positive dynamics has been observed for several years and corresponds to the general trend of sales growth of beer and other alcoholic drinks with unusual taste and flavor. Finally, for …finding stability was a good performance though the brand moved closer to superpremium.

In the most expensive, superpremium market segment AB InBev Efes became a leader a long ago and has been reinforcing the leading positions thanks to the portfolio of popular import brands. The company has managed to keep its share though the import beer market is growing fast, being very fragmented and expending (though it degenerates into rotation).

In the first half 2021, … out of ten leading brands belonged to AB InBev Efes including #1 and #2.

Mexican beer Corona, a major import brand has continued increasing sales rapidly, despite a considerable growth of retail price. In the first half of 2021 the share of Corona exceeded …% by volume and …% by value which is a very good performance for superpremium brand from far abroad.

It seemed that negative associations were supposed to cause sales decline of beer Corona. At the beginning of the pandemic, 38% of respondents in the USA said that they would never buy this brand. However, the results of 2020 showed quite an opposite picture. Sales all over the world increased by 17% and in the rating of Brand Finances Beer 50 over 2020 it became brand #1 in the world.

For example, sales of beer Corona in Great Britain soared by 40% which made it not only one of the fastest-growing alcohol brands but even among other categories of products. In Russia the growth reached …%. Beverage market analysts link this to higher recognizability of the brand that had been strong even before, as well as to growth of search inquiries when Google users turned to topics of beer and coronavirus.

Certainly, riot growth of Russian sales of Corona can be called non-organic or incidental. Yet the share of other market leaders of AB InBev Efes, German beer … was growing at equally dynamic rates. The positions of two major import brands almost equaled in the first half in 2021. Though because of much more restrained price growth when estimated by value, … has yielded its positions to Corona in this season.

The portfolio optimization of AB InBev Efes that formed after merging led to disappearing of many affordable federal and regional brands. If we look at the dynamics of “…” brands that we are considering together we will see not only its sharp decline in 2020 but also a share much exceeding by … than by …. Thus, the company defined a space on the shelves having excluded cannibalization and better positioning the selected brands.

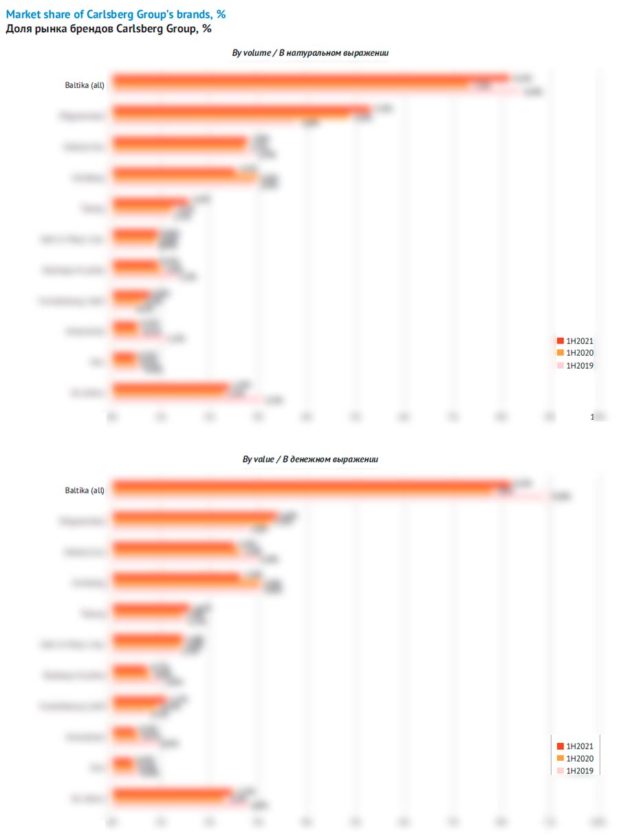

Baltika, Carlsberg Group

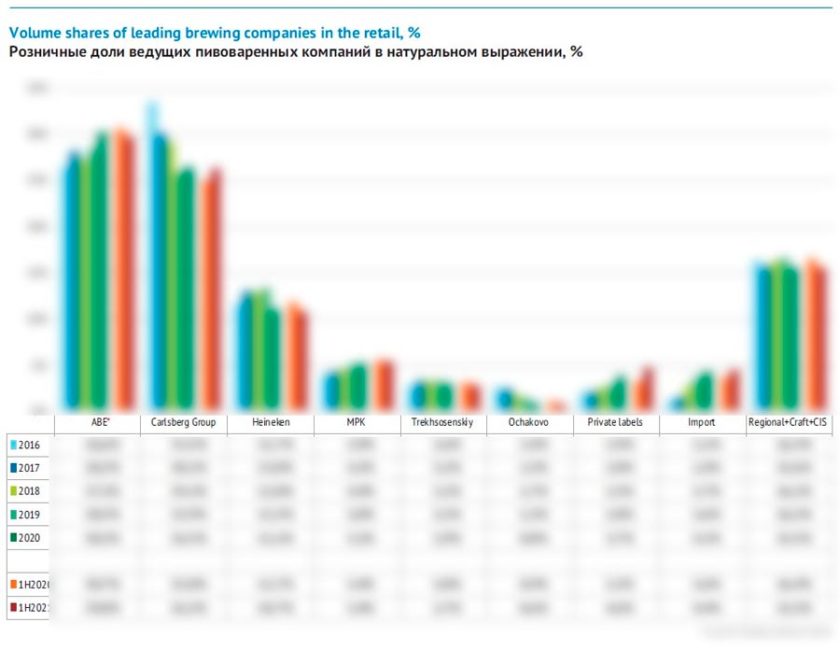

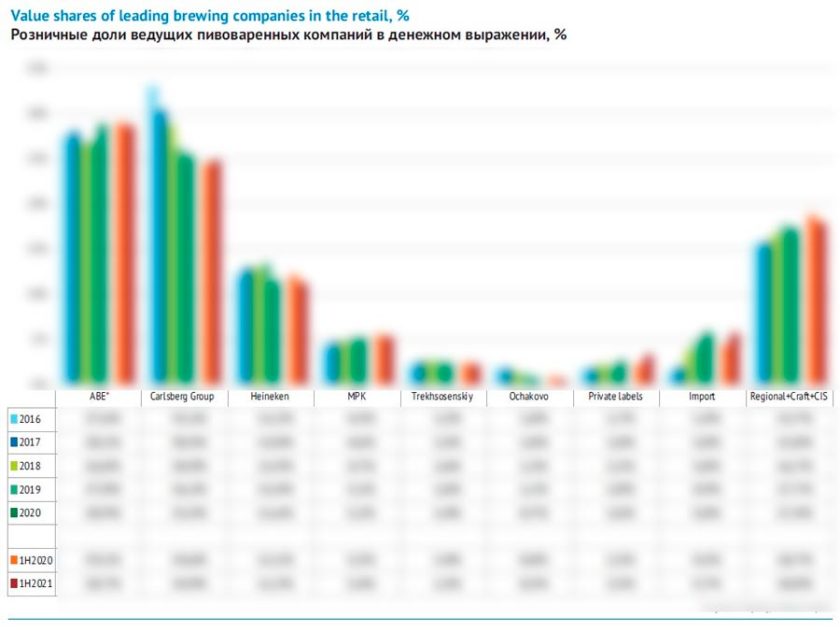

Company Carlsberg Group though occupying the second place in the Russian market has been the major player in 2021.

Thus, in the first half of 2021, the market share increased by … p.p. by volume at the moment when competitors either cut down the share or kept it at the same level. By value the performance was much lower, the growth amounted … p.p. Thus, the second reason, why Carlsberg Group influenced the whole market so much is absolutely obvious. The growth of sales and share followed the current decline of average retail price for beer without much attention to competitors.

Such activity of the company was connected to problems that accumulated over the previous years. From 2016 to 2019, the market share in Russia was rapidly decreasing that can be explained by general popularity drop of mainstream Russian brands and focus on sales profitability. 2019 was especially stressful when Baltika lost more than … p.p.

In 2020 the management of Carlsberg Group told about high competition pressure at the market so powerful promotional activity was started in order to keep the volumes and improve the market share. The year of 2020 thanks to warm summer and growth in home consumption let many producers expand, but Carlsberg Group sales exceeded the market considerably. They increased by …% having amounted to nearly … mln dal according to our estimation.

Let us note that even such growth allowed compensating only a part of losses of past years. Baltika has started actively increasing its share in the second half of 2020. So, in the first half of 2021, due to the low-base effect (especially in the second quarter) it wasn’t too difficult to show a good performance by simply keeping the market share. Now, in order not to deteriorate the performance there is likely to be a high level of promotional activity during the sales high season.

Commenting the first half-year performance, the company management told about the cost growth and of possibility of price revising. Cees ’t Hart, head of Carlsberg Group said:

“With regards to the Golden Triangle* in Russia, well, we’re not entirely satisfied with the balance of the Golden Triangle at this amount of time. I think what we did last year is correcting the decline of the market share and the team has significantly improved our position in Russia. We are now at a market share of, let’s say, between 27% and 28%, which we feel is more or less fine for us at this moment of time. We start to repair the other parts of the Golden Triangle because the increase in market share came at the cost of margin. So we’re now rebalancing this Golden Triangle and the assets of the Golden Triangle… But we take pricing and will continue with the promotions up to the level that we are not going to lose significant share, because 27%, 28% of share is what we feel we need to stick to. We’re going to take another price increase after the season, as said…”

* Carlsberg has traditionally applied its ‘golden triangle’ of volumes, operating profit and growth margins to its business: balancing all decisions against these indicators in order for the company to grow.

Let us look at how the company’s structure has been changing by price segments of the beer market.

One of the key drivers of restoring in 2020 was beer …. Its retail price went considerably down then, but in 2021 it also remained one of the lowest among those brands that have federal distribution (at the level with … and …). As independent producers were made to actively participate in the price competition, … growth slowed down, yet its market share went …% up anyway. Thus, … (or, rather its version by …) has even more reinforced its position of brand number 2. It backfired by a decline in the market share of the shelf neighbor, economy brand …, that had a stable retail price and in 2020 it was considerably higher than that of ….

The share of mainstream brands by Carlsberg Group were fluctuating at different direction but in general, the company’s positions in the segment remained unchanged. Here for the most part the situation was determined by title brand Baltika represented by a lot of sorts at various prices. In the first half of 2021, beer Baltika almost managed to restore the share …. Yet by value the market share was growing … slower.

The recovery took place to a big extent due to promotional activity that brought Baltika’s price from … to … RUB/L. Besides in tune to the general trend, as early as in 2020 sales of “Baltika 0” started growing rapidly. At last, in 2021 the superbrand was supported by new launches: dark, wheat and alcohol-free fruit (Baltika 0 Lime) sorts that started gaining market weight during the first six months.

Baltika’s growth was substantial, yet, it took place against neutral or negative dynamics of many other mainstream sort. Thus, the market share of beer … is still at the same level for the third year running, but retail price is constantly decreasing. … sales stabilized after a dramatic drop in 2020 connected to moving it from the economy to the mainstream. … brand that became a bit more expensive as well as competing licensed brands has lost some of its market share though its dynamics was positive until the recent time (however, here one should take … growth into consideration).

All premium brands by the company have increased their market share to some degree and one could say that it has reinforced its positions in the segment. If it was not for the fact that … had the most substantial sales growth which took place due to mighty promotional activity. This brand’s retail price has gone down considerably over the period under consideration. It virtually went beyond the borders of the premium segment and equaled beer …. At the same time, according to the growth trends of special beer sorts the share of company’s license favorite, beer … were coming up. Besides, the performance of … was reinforced, the brand has been steadily growing since its launch 6 years ago.

Summing up, let us note that in the second half of 2021 the company’s volumes have started being influenced by the … effect and the prices have experienced the impact of their …. So, one shouldn’t expect further fast growth of Carlsberg Group’s share according to the results of 2021.

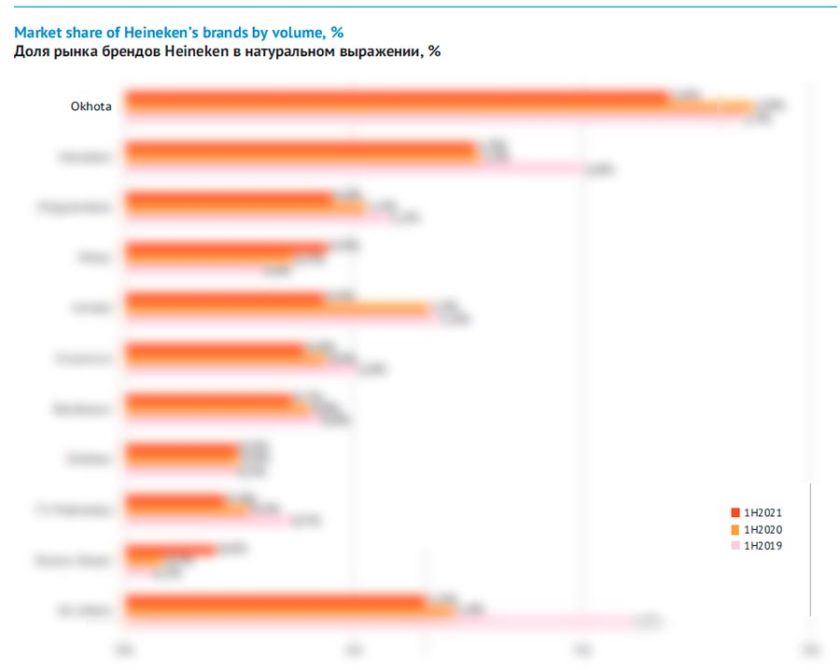

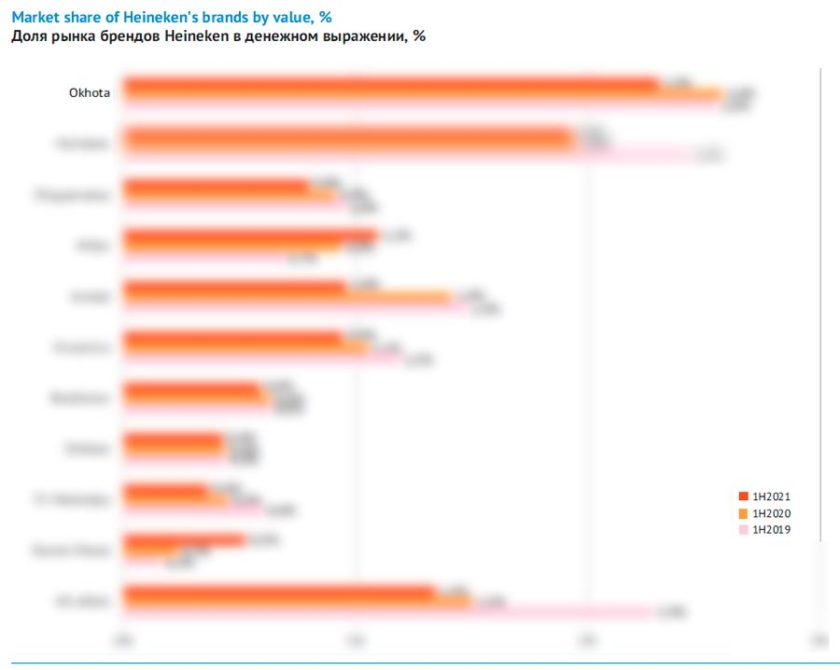

Heineken Russia

In 2020 Heineken company after a rather long period of growth virtually nullified the performance of the past years. In the first half of 2021 the market share stopped decreasing so rapidly, and according to the company’s estimation the dynamics in Russia was positive.

Their press-release says:

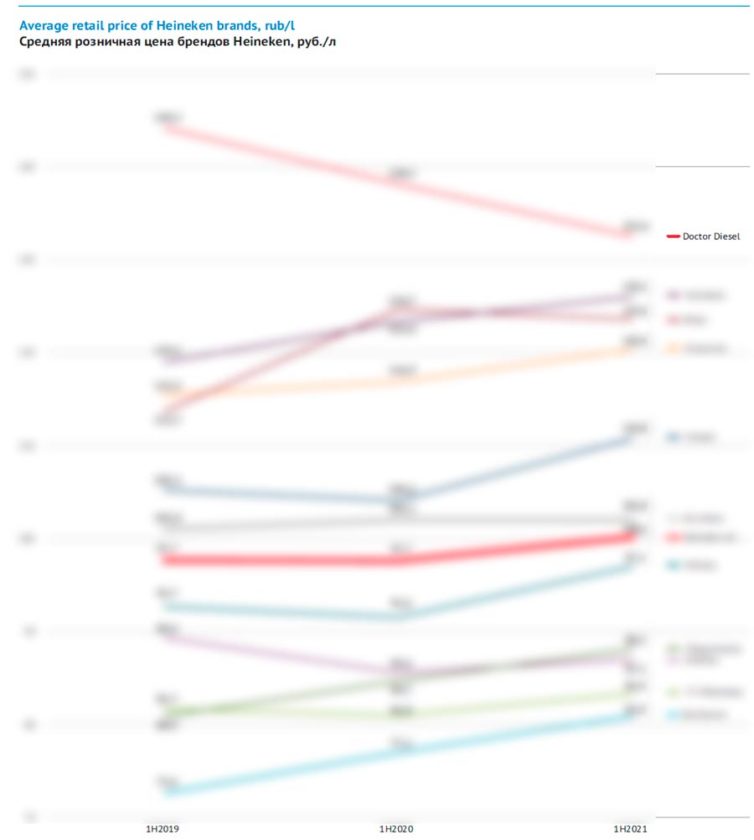

“In Russia the sales volume has grown by 4-6%, which is based on sales growth of premium brands by more than 10%, in the first place due to Heineken, Miller and Dr Diesel. We have widened the taste range of Dr Diesel by launching a drink with strawberry and lime taste combination, fewer calories and no sugar. Our cider portfolio has grown by at least 10%”.

The main reason for Heineken’s positions’ deterioration in 2020 as we can see from liters and money relation, there was a harsh price policy. The company wishing to keep the profitability sacrifices its volumes though … and then … applied the opposite marketing strategy. The drop mitigation can be explained by the fact that the retail price for beer of … competitor has gone up and one can expect the same at ….

In the market’s economy segment Heineken company as well as many other brewers made a big stake on …. It used to be one of the cheapest in the market, yet a rather aggressive policy of … in promoting its version of the brand. In the first group of 2021, … decline sped up due to higher price. At the same time, the shares of federal economy brands … and … were deteriorating. Only regional brand … kept its stability.

In the mainstream segment the company for the most part is represented by brand Okhota which is still the biggest in the portfolio and the leader at the strong beer market. In 2020 Okhota obviously managed to take a part of Arsenalnoe sales as the “strong” competitor lost some of its consumers due to moving from the economy to mainstream segment. Yet the average price growth in the first half of 2021 led to a decrease of … share.

In the premium segment of beer market the performance of Russian subdivision of Heineken were multivalued as the shares of certain brands were fluctuating considerably and the general market share of the company remained virtually at the same level.

Perhaps, we cannot call the neutral dynamics of … a bad performance, as the dynamics of the whole premium segment was neutral. The market share stabilized after an unexpected decline in 2020. It was been obviously connected to the company’s inflexibility when renewing contracts with supermarkets and following reduction of brand’s representation in modern trade.

Market share of … and … has not yet managed to overcome the negative trend though their reduction has been compensated by … that is new for the company’s portfolio and has not exhausted its potential yet as well as … brand thanks to new launches. In the light of consumers’ interest to special beer sorts the company relaunched non-filtered wheat beer Edelweiss early in 2021.

As we can see Russian portfolio of Heineken is growing ever more …. But while outrunning growth of … beer had been drawing the … before, in 2020 and early in 2021 this process took place due to share decrease in the … and … segments as well as the ….

Other brewers

The positions of the three market leaders are not stable, and if we consider their share in general, we will see that it has been declining in the long run. In the first half of 2021, the big three lost … p.p. though while in the past they mostly competed with regional brewers, over the recent years the leaders’ volumes have been taken from them by … and ….

Among mid-sized federal companies … has been demonstrating a steady growth, … was stable until recently, and … company was losing its market share.

… unlike the leading three has been keeping its key brands retail prices at roughly the same level for three years. Almost a … of retail sales of the company is accounted by …. In the first half of 2021, its share restored following a drop a year before. The share decrease of economy brand Obolon has been compensated by volume growth of …, while the shares of … and … brands have hardly changed. In the aggregate, all these movements led to neutral dynamics according to the market development.

… brewery that was actively developing due to price competition and cooperation with modern trade, was shifting from growth to neutral dynamics and now is experiencing decline. In the first half of 2021, the shares of three key brands, namely: …, …and especially …went down. Probably the reasons lie in the relation with their main partner, major chain of alcohol shops Krasnoe&Beloe that refused selling draft beer. Besides, the brewery faced technical problems in August. According to … publication, … brewery was loaded only to …% because of busted water main.

Regional breweries dynamics is not stable and barely predictable. In the first half of 2021, they in the aggregate decreased the output volumes by nearly … p.p. which can be explained by competitive situation. In the economy segments the pressure from …and beer importers from neighboring countries (Belarus and Kazakhstan) went stronger. All over the price range, regional producers experience pressure from market leaders and from above craft brewers attack by beer sales in special retail (not shown in the diagrams).

In the first half of 2021, Siberian brewers saw their share in retail decrease. …, under our estimation based on regional statistics data, has kept its volumes at nearly the same level. However, along with the price raise, the retail share decreased from … to …%. Altai regional breweries have also raised the retail prices and cut the beer output by …%. …, … and … breweries lost some of their retail share. Brewery … in Omsk has sharply cut down beer output perhaps due to the owner’s problems and undefined status of the brewery itself. Besides, going west beyond the border of the Siberia we can notice a considerable sales decline of beer by brewery … in the Ural.

At the same time, almost all breweries in the Volga region demonstrated good performance, taking into consideration their reasonable price policy. The retail share of …holding has grown considerably. The share of … slowed down sharply but has not yet stopped growing following a riotous start. Besides breweries …, … and … have improved their positions a little.

Considerable breweries in Krasnodar Krai and … have shown generally good performance.

In the Central region the positions of mid-sized breweries have been generally neutral. Three major breweries, namely …, … and … (after shifting its production from mainstream to premium) have had some decrease in their shares. The retail share of … in Voronezh has dropped, yet two other Voronezh breweries, … and … have grown. … have decreased its output volumes as well as the market share. Instead, judging by regional statistics and retail market share … in … has shown excellent growth as the brewery has been developing for the third year running transforming into a considerable regional market player.

To get the full article in pdf (28 pages, 27 diagrams) propose you to buy it ($40) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.