The catalogue of Ukrainian breweries contains 251 producers ranging from transnational groups to craft and restaurant breweries. In the catalogue we have combined open official data, information from social networks and where possible, from brewers themselves.

The previous “census” was made by us in 2011-2012. So, what has changed over the recent ten years and what trends can be currently seen?

Trends of craft brewing in Ukraine

Three-fold growth in numbers

Over the ten years, the number of craft producers (restaurant, microbreweries and minibreweries) has grown threefold, from 79 to 226 businesses* under our estimation. The majority of the breweries from the previous catalogue are still operating.

*By the start of 2012, 11 craft breweries, two regional breweries and one major brewery were located on the territories currently beyond Ukraine’s control.

The growth of beer producers number was taking place by leaps. The first wave 2008-2011 was connected to economical growth after recession in 2008, small business recovery and expansion of foreign equipment suppliers.

The second wave 2015-2016 was connected to growing interest in consumers to local craft beer and incomes stabilization among population. Consumer’s preferences were also changed, as people became more demanding to beer taste yet they started cutting down beer consumption.

Naturally, the development of the craft trend stimulated localization of brewing equipment production. Some brewers started even making it on their own. Lower barriers to the business entrance led to increasing wave of breweries growth in 2018-2020 which has been stopped by covid-19.

Since 2010, only several second-rate regional breweries have stopped operation. Instead producers of nation-wide scale and craft positioning (Fanatic Brewing Center, New Brew, Varvar, Pravda etc.) have scaled up or emerged.

Six-fold share growth

Over the 10 years, we have seen a considerable growth of small producers, which is linked to the low base effect, breweries number increase and their production up-scaling.

According to our calculations in 2011 Ukrainian craft brewers made 15 mln liters of beer. At that time, that volume amounted to 0.6% of the total Ukrainian output.

In 2019, craft breweries made about 45 mln liters and the share in the total output equaled nearly 2.5%. If we take into account breweries with bigger capacity and breweries with craft positioning and national scale, the volumes reached 65 mln liters and the share in the total output volume amounted to about 3.5%.

Regretfully, in 2020 covid-19 knocked down the local business. Many craft brewers announced their sales to fall by more than two times. The key reasons for this were:

1) Problems with beer sales through HoReCa due to several lockdowns and worries concerning the health issues among restaurant visitors.

2 Redistribution of all purchase types for the favor of supermarket where craft brewers are barely represented.

3) Taste simplification (which we have detected in our analysis of sales by sorts) among beer lovers which is connected to drop in incomes and the regime of self-limitation.

Not at the restaurant

The development of the craft trend resulted in specialization at the brewing instead of brewery being a “feature” and a decoration at a restaurant.

Thus, ten years ago, small brewers normally were restaurant brewers. Breweries at a HoReCa institution were predominant (51 businesses or 65% of the total number of small brewers) and only 28 breweries (35%) focused on outer sales. Though sometimes it is difficult to tell the difference between them.

Today we can speak of some parity. Yet by the start of 2021, we have calculated 107 restaurant breweries (47%) and 119 breweries focusing on sales to retail networks. Naturally, net volumes of restaurant output are much lower.

We should also emphasize the growth trend number of breweries oriented at their own retail network, that is, production and shops belong to one owner.

One more trend is ever more often powerful minibreweries supplying beer to several HoReCa establishments

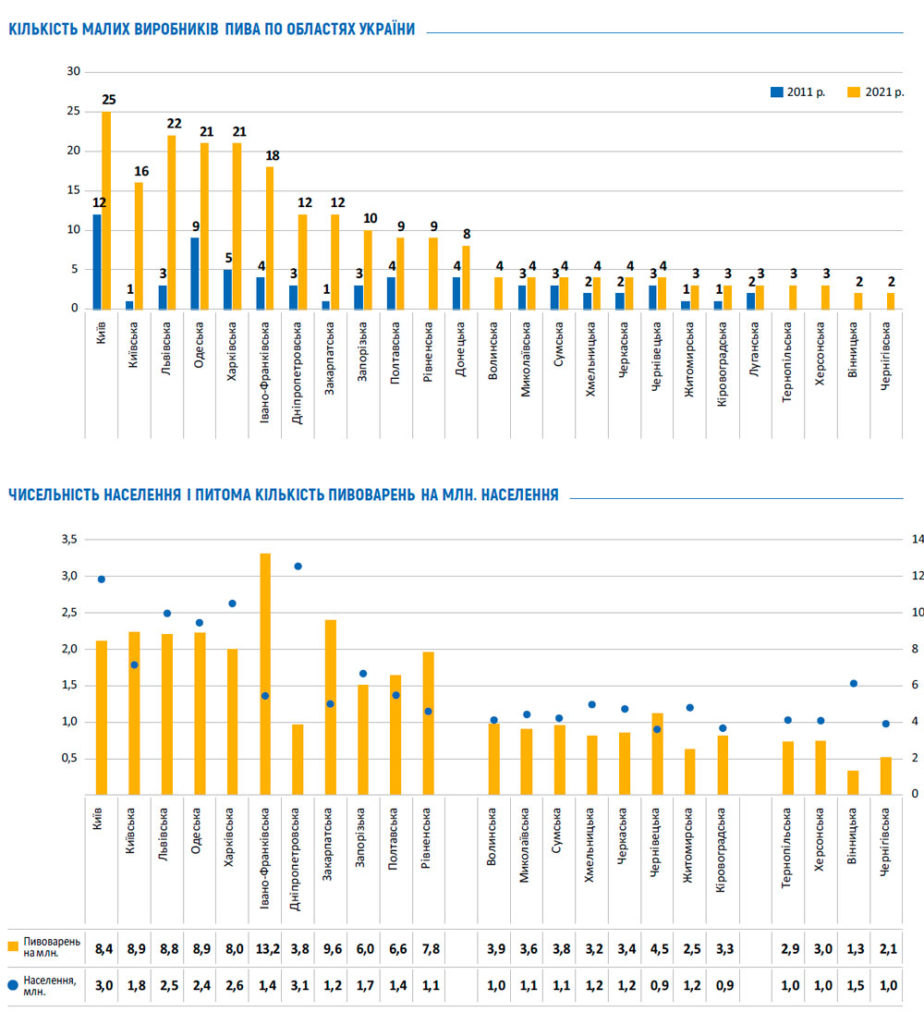

Regional distribution

Obviously, the main volume of craft beer is consumed by wealthy dwellers of big cities. The process of consumption is connected to development of HoReCa, industry of recreation, tourism and other entourage. That is why Kiev and the region, Lvov, Kharkov and Odessa regions lead the pack by the number of small breweries.

Yet, if we compare the number of breweries to the population number, we will see that several regions in the west of the country are considerably ahead. As one can see on the graph, in Ivano-Frankivsk, Zakarpatska and Rivne oblasts entrepreneurs are more often fond of brewing, and more often brewers open at restaurants, most of such breweries outputting small volumes of beer.

One can notice a deficit of breweries in many central regions (especially in Vinnitsa, Khmelnitsk and Zhitomir oblasts) surrounding the capital. There are comparatively few breweries in the industrial region in the east of the country, especially in Dnipro oblast (however, Fanatic Brewing Center exceeds many craft projects by its size).

How this catalogue was made up

In order to make up the catalogue we requested data on 761 organizations with type of business activity “Beer production” (both major and additional) from Ukraine’s Office for National Statistics. Among them we pointed out 458 organizations that were active in 2020 (paid taxes according to Fiscal service).

Then we combined these data with brewers’ register outputting up to 3000 hectoliters per year (licenses for wholesale trade). These breweries are marked with “<3000 Hl” in the catalogue.

Unofficial description of breweries as well as confirmation of their operation have been obtained from the following sources:

• Check-ins from untappd.com catalogue allowed us to trace breweries’ activity by beer availability in retail and HoReCa. There are almost all breweries from the catalogue (93%).

• Official sites and breweries’ accounts on Facebook and Instagram also helps to assess the level of breweries’ activity by messages on new product launches, events, etc. 190 breweries in the catalogue have their accounts on Facebook (76%). 133 breweries have their accounts on Instagram (53%). 168 breweries have their own website or a page (67%).

• Besides, for breweries description we used news on pivnoe-delo.info, beerplace.com.ua, gulikbeer.com.ua, beertechdrinks.com and others.

We have combined official and inofficial data. Then we contacted the found operating beer producers by email, accounts on social networks or by phone.

262 breweries from the official list and untappd.com catalogue have been removed as they duplicate other production, had stopped brewing beer long before, belong to nano-breweries or brew branded beer at external capacities. 59 organizations told us that they had not produced or stopped producing beer.

As a result, the catalogue has 251 beer producers. It also includes 11 producers that we could not contact, yet that are likely to continue operating.

This figure is close to many other estimations. For example, according to BRDO there were 241 breweries in Ukraine, 204 of which being craft breweries with a capacity of up to 300 thousand liters per year. As we calculated beer productions of which there are more than of organizations, our census almost equals the figures by BRDO.

We have info on equipment producers of 102 breweries in our catalogue. The leading five by the number of objects are: Heinrich Schulz, (21), ZIP Technologies (20), Pivoyar (13), Termo-Pub (8) and Stainless Steel Technologies (5).