The natural volumes of beer production and sales have remained almost unchanged, yet in monetary terms the market stopped growing because of promotions and inexpensive brands growth. Unstable retail operation as well as COVID-adjusted behavior of consumers had different impacts on brewers. Yet in general, the negative effect was inverse to the scale of their activity. Thus, the leading threesome kept stable due to mass inflow of beer lovers to supermarkets. As the situation was difficult to foresee, the output dynamics of certain companies seriously differed from their sales in retail. The leaders’ positions were much influenced by promotion that was aroused by higher practicality in consumers. Almost all regional brewers incurred considerable losses at the years start because of unstable work of special beer shops. Craft brewers found themselves in the most difficult situation. The segment of beer in kegs and glass bottle that partially “flowed” to PET and can, decreased significantly.

The general situation at the market and the industry

For the beer market, the first half of 2020 was a period of transition from normality to complete uncertainty and, to some extent, back. At first, the introduced administrative measures as well the shock among consumers led to changes in their behavior. It seemed that the beer that is not the essential item was going to be ignored in preference to basic FMCG.

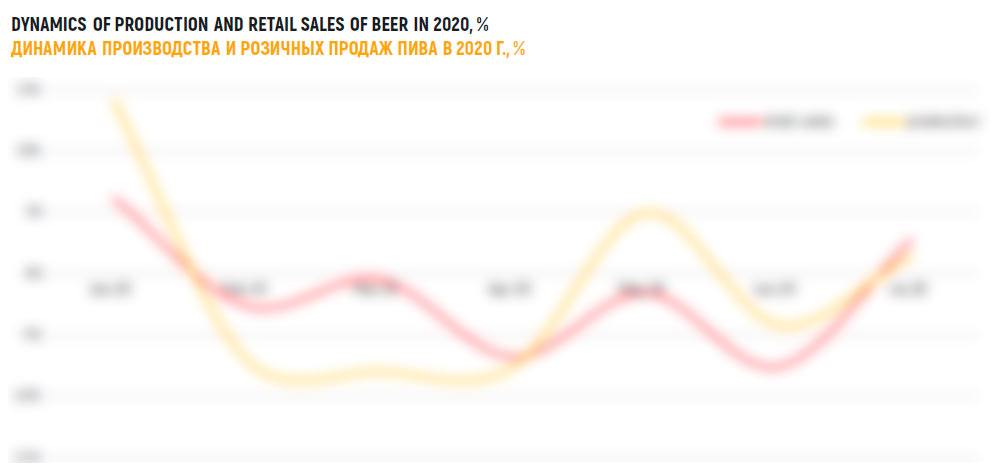

Expenses to form stocks as well as care for their future and health really drew consumers’ attention from beer for a short time. The rates of beer retail sales started slowing down in winter and after fluctuating at zero point, collapsed dramatically in April 2020.

Brewing companies expecting the demand decline, took the lead and cut down their output as far back as in February. The decline of -*% was observed until April. Yet the brewers smartly reacted to the prompt stabilization of retail beer sales in May and followed their dynamics ever since.

Constant fluctuations of retail beer sales resulted in their reduction by *.*% over * months of 2020. At the same time, *.* percent was lost by the beer output. Yet the low-base effect of late 2019 allows expecting the performance of 2020 not to be negative in terms of the output volumes.

As below we will estimate the performance of different brewers during the first half of 2020, for reference the performance for the first * months will be given. Retail sales over that period fell by *.*% by volume. The production shrank by *.*%. That is, in case a company had better dynamics, their market share (or their share in the output) was growing. And vice versa.

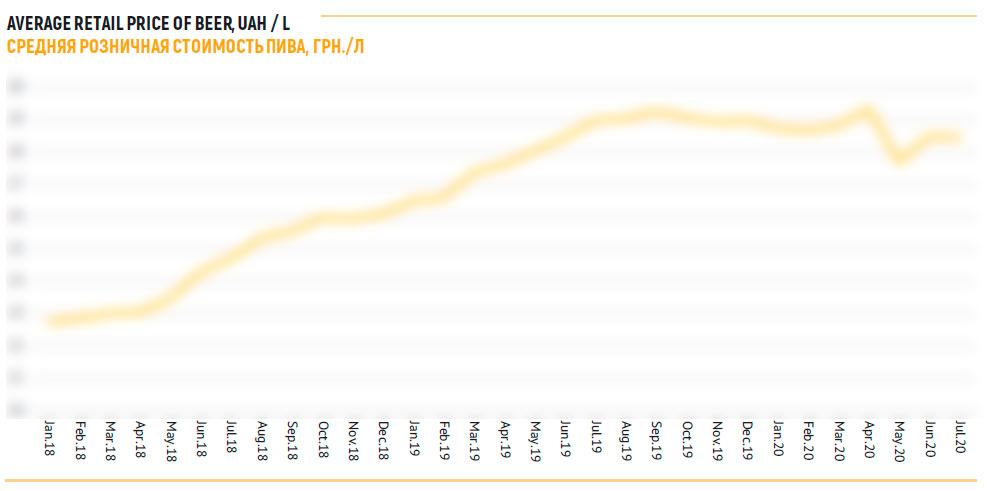

Lower average retail price of the sold beer has become a new trend. Before autumn 2019, it was growing rather distinctly, but then it started decreasing abruptly. And as we can see such decrease resulted from not only coronavirus, as it had begun earlier. We should rather speak of price competition among market leaders.

The very first, autumn decline in beer prices was obviously connected to competitive promoactivity among brewers that decided to sell surplus supplies in the low season. Because in spring 2020, there started correction and the average price returned to the level of September. Yet, by May, the coronavirus lowered the demand and the prices plummeted again.

As a result, the beer market by value over the first half of 2020 increased by only *%, to **.* bn hrn. This growth can be considered very low compared to two digit rates of the previous years. In dollars due to unexpected hryvnia strengthening early in 2020, the growth amounted to *%, to $*** mln. However, in autumn hryvnia devaluated again, and in dollars the market is not likely to grow by the end of 2020.

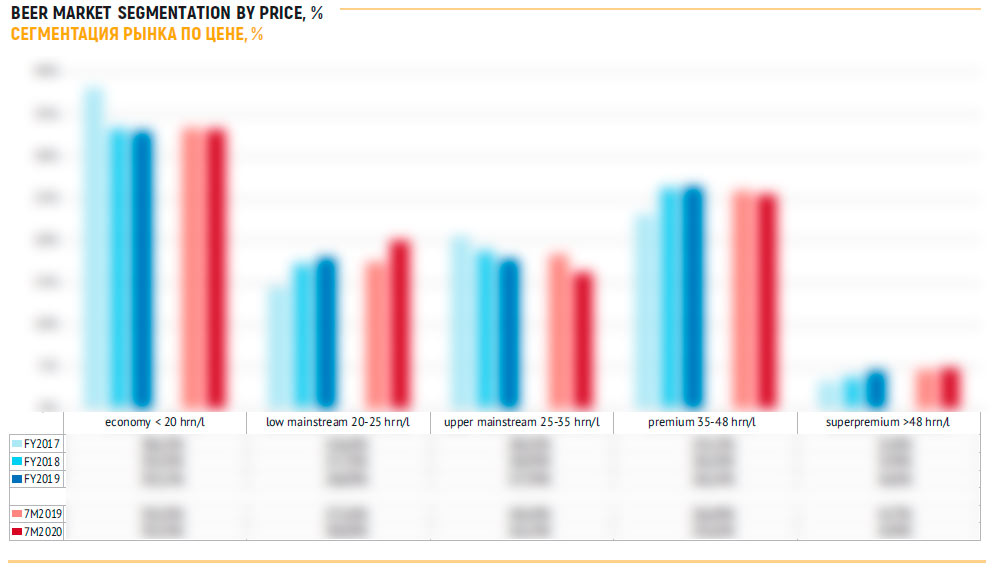

The retail market segmentation by the price and package

Low mainstream has become even stronger

Over the recent years, the Ukrainian beer market headed for premiumization.

Until 2020, consumers ignored very cheap beer, so sales from the economy segment flowed to low mainstream.

The upper mainstream segment (that is mostly represented by local Ukrainian brands yet with pretense for special taste and premiality) was gradually blurred.

At the same time, the consumption focus was being shifted to more marginal license sorts. There was a leakage from the premium to superpremium segment.

No doubt, these processes were driven by branding activity of the market leaders who launched attractive novelties and made license beer more affordable. “Old new” brands by AB InBev Efes as well as gaining popularity international brands had their market weight increase rapidly. This expansion is taking place even now.

Yet, in 2020, the consumers experienced income decrease, unemployment and uncertainty resulting from the epidemic. Many households drifted to lower income levels. Concern for material issues turned on the cost-cutting drive in family members.

The consumers’ behavior was mostly changed in spring, when there occurred the synergy of strict quarantine measures and psychological effects of COVID-** news.

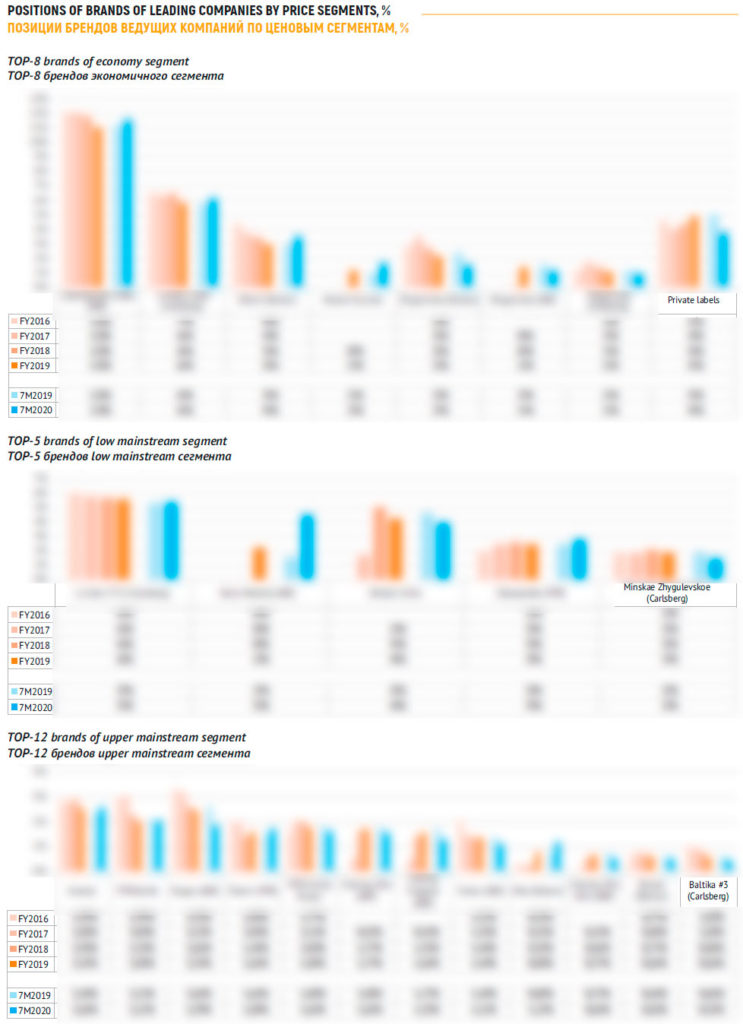

As a result, the market share of inexpensive beer (costing less than ** hrn/l) stopped decreasing and stabilized at a third part of sales by volume.

In 2020, two oppositely directed processes have been behind the economy segment stabilization. On the one hand, major economy brands’ retail sales have been growing rapidly, though they had been decreasing till then. Collective Zhigulevskoe as well as supermarkets’ private brands lost their positions unexpectedly, though prior to that they had been pressing brewing companies’ own economy brands.

Let us note that more than */* of beer sales of private brands accrues to ATB network. And beer Zhigulevskoe, though not belonging to anyone, occupies a considerable position in three market leaders’ portfolios.

Blurring of upper mainstream in 2020 has progressed at a much higher speed; it has lost *.* p.p. over the accounting period. Yet, this process was taking place just “underneath” as only low mainstream got an additional impetus to further growth having gained as much as *.* p.p. In general, that dynamic process was connected to both price policy and changes in brand portfolio of the same company, namely, AB InBev Efes.

And the premium beer market share has not only stopped growing but even lost (nearly *.* p.p.). However, superpremium sorts have remained stable and even showed some growth. One can say that their stability was provided by other beer consumers who left HoReCa.

That is, people willing to spend more for special beer (image, specialized, import, ect) now came to get it not to bars but to supermarkets.

Thus, the economy segment stabilization and the fast share increase of low mainstream have become the key factors of cutting the average selling price for beer at the retail market. Noteworthy, that process had begun earlier than the epidemic. The second factor as we have said, is the active promotion by the companies.

Besides, speaking of the marginal segments (upper mainstream and segment), we should note that there has been a market share reduction of beer with special tastes (white, fruit, etc.). Over the accounting period, it decreased by *.* p.p., to *.*% (we estimated about a dozen of the key sorts). This change might be connected to a higher price for special beer. But we can also speak of beer lovers’ taste simplification resulting from covid type of consumer behavior. People started preferring the basic goods sorts.

Supermarkets and consumption easiness

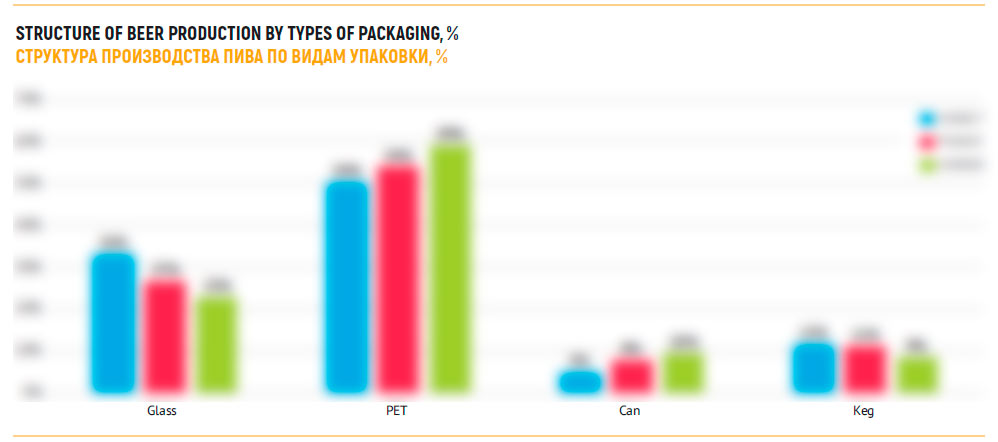

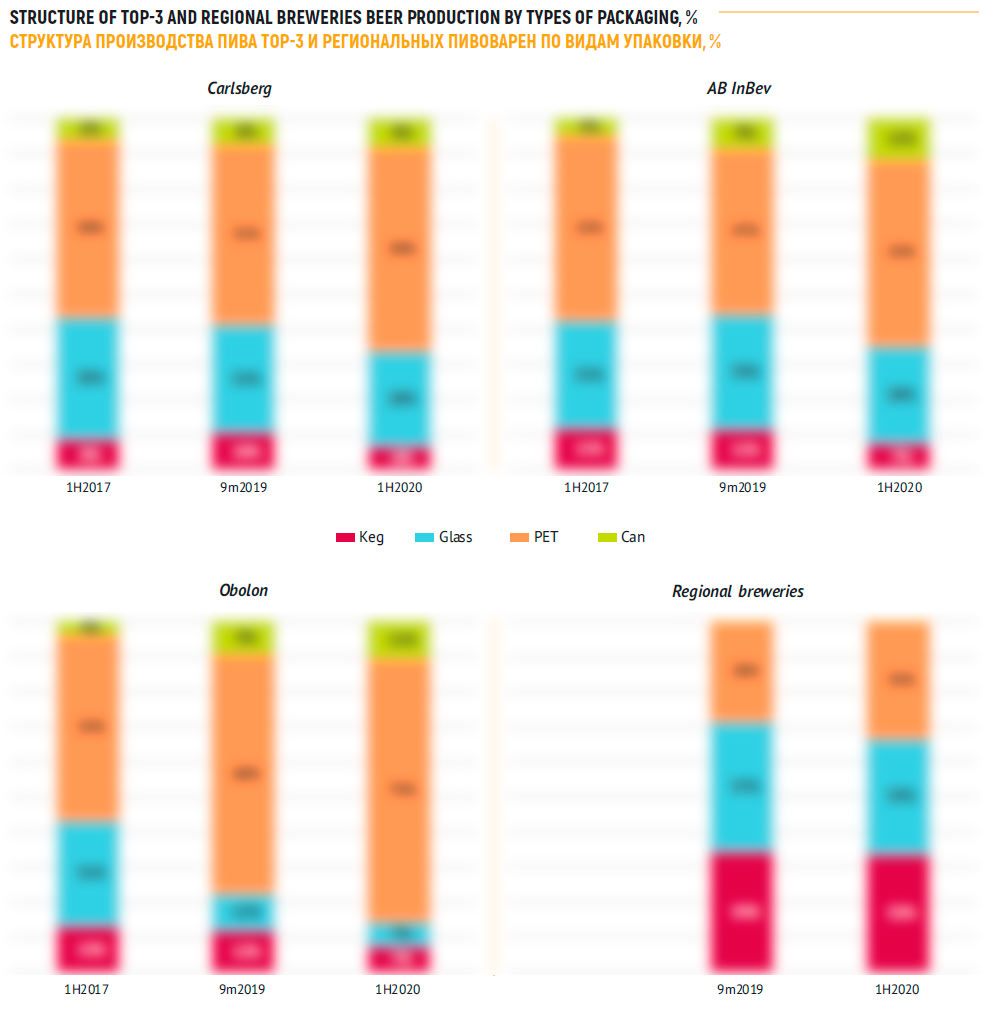

The pandemic has seriously influenced the market segmentation by package as the market share allocation is connected to the consumers’ behavior. For adequate estimation, we used data on output volumes, but not on the beer sales, as it allows taking beer in kegs into consideration.

For a start, one should name the key driver for changes. It is higher significance of supermarkets not only among formats of universal retail trade, but in general, among all beer sales channels. Customer behavior at supermarkets usually includes purchasing of a large number of goods for future use. And judging by the market segmentation and by the package the inflow to supermarkets means focus shifting towards lighter and sizable packages.

In particular the growth of PET package was caused by the opportunity to economize and buy a big volume of beer at the same time. Besides, PET benefited from sales stabilization of inexpensive brands due to consumer economizing.

Gradual popularity growth of aluminum can is a long-term trend that is typical for all post Soviet states. Can is a single option light package for beer of mainstream and marginal segment. Thus, if beer is being bought at supermarkets for the future use, the can share is growing too. However, in 2020, this trend somewhat weakened as consumers paid attention to inexpensive beer (economy and low mainstream segments) that are mostly packed in plastic.

Purchasing beer in glass is currently an impulsive and one-time action that is not planned and not connected to the wish to economize. It is more typical for traditional shops and kiosks. Obviously, active inflow of consumers to supermarkets as well as submission of their impulsive behavior led to reduction of glass bottle glass. However, the sales reallocation in favor of can and PET has been long observed.

Low draft

Closure of public places and subsequent depression in HoReCa segment considerably affected the draft beer market segment. But temporal closure of special draft beer shops in spring 2020 took the heaviest toll on the industry. However, in that channel the situation improved by the summer 2020.

Let us enumerate several factors in order to adequately estimate the changes

1. Keg significance for brewers is inversely related to the activity scale

We know the allocation of keg beer production for three market leaders and regional brewers. The share of kegged beer output of the leading threesome in 2019 amounted to **, ** and **% (ABE, Carlsberg, and Obolon accordingly).

At regional brewers the share of kegged beer averaged **% of the output. However, for certain brewers this share can differ much. For example, such famous mid-sized breweries as Poltavpivo, Umanpivo and Mikulinets brewery Brovar pack nearly **% of their beer in kegs. Other considerable regional brewers for example Berdychev brewery and Khmelpivo sell at least **% of their beer in kegs.

For small craft breweries keg beer is often the only (or the only considerable) package format. Though Varvar, Pravda and some other craft brewers can be proud of having glass bottle as well as of being present in the modern trade with wide sales geography.

2. More than half of draft beer is sold in HoReCa that has incurred losses.

That is why its sales are crucially dependent on normal working conditions of public places. And judging by the relation of the market shares, more than **% of beer sold in restaurants belonged to the leading threesome. Though craft breweries suffered most of all, in numerical terms their share in restaurant sales amounts to several percent.

Here one should pay attention to assessment by Poster service company, that analyses data on *** HoReCa establishments.

April 2020 was the hardest month for Ukrainian restaurant-keepers. The income of the HoReCa establishments amounted to only **% of that in February. In May, this figure went up to **% of the prior-to-crisis level.

Far from all restaurants made it through the crisis. In July, in Ukraine **% of all HoReCa establishments, Poster clients of all that worked before the quarantine, were operating.

After resuming regular operation, despite lower incomes, most of HoReCa establishments managed to keep or increase the average bill compared to the previous July. This can be connected to altered behavior model of guests. People started going to restaurants less often but if they do, they satisfy all their wants at once.

3. About a third of the draft beer is sold special package in special retail, that incurred losses but not much.

Mid-sized regional breweries sell almost all their products not at HoReCa but in specialized beer retail. Likewise, craft brewers consider restaurants to be their key direction in relation of their image but sell most of their production at draft beer shops.

Strict quarantine in Ukraine continued a little less than two months. In started in mid-March 2020 and finished early in May. During this period, in order to stop the epidemic, the local authority of most populated areas closed all public places except for food shops, drug stores and filling stations. Naturally, the restrictions touched upon thousands of draft beer shops. Yet, this channel of sales suffered much less than restaurants.

For one thing, draft beer shops (unlike HoReCa) are prone to significant season fluctuations of sales. As the lockdown took place during the cool season, it did not have catastrophic sequences.

For another thing, against HoReCa, beer shops look relatively safe to visit, as one does not have to spend much time there and the health requirements are easier to comply there. Under our rough estimation, special retail in the first half of 2020 could lose **% of sales. But, by the end of the year, the reduction is likely to amount nearly **%.

Taking into account all mentioned factors, the draft beer output statistics looks clearer.

Major brewing companies, in the first half of 2020, cut their volumes by **-**% mainly due to decline in restaurant attendance. Each company in the leading three lost several percentage points in the general output volumes.

At the same time, the regional brewers decreased kegged beer output by nearly *% because of the temporal closure of draft beer shops. As the market leaders had even worse dynamics, the regional producers increased their share in the draft beer output from ** to **%.

We do not have statistics on craft brewers, however, judging by their messages, the output of kegged beer in the first half of 2020 can have been cut by **% and more because of blocking of two major sales channels.

Companies and brands

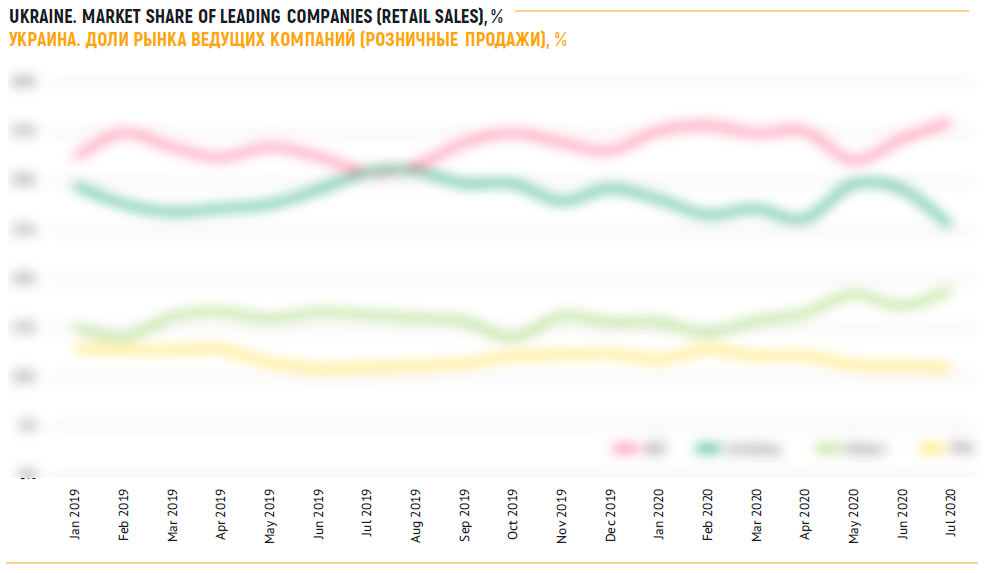

The pandemic interfered with brewers’ plans all over the world. Though in Ukraine the dynamics of output and retail sales matched in figures generally for the industry, but it did not match if we considered separate companies.

Thus, by the end of 2019, the output and retail sales assessment of the three leaders had unidirectional dynamics, in the first half of 2020, the output decline did not mean a sale decrease but the opposite.

Obviously, such difference was connected to stock forming early in the year (in January 2020, their level was by a third higher than early in 2019). But as the epidemic progressed, brewers took a wait-and-see approach and did not hurry to form stocks, that is, in spring, their level was lower than the previous year.

Buyers were very sensitive to price changes, seducing brewers to reduce risks and sell products faster. Constant competition between AB InBev Efes and Carlsberg Group in Ukraine resulted in virtual price wars even during the summer. This competition led to dynamic hikes in market shares and sales the production reaction could not keep up.

That is why it is no surprise that some companies rose their output while the retail sales decreased. The dynamics are likely to even by the end of 2020.

The fluctuations of giants’ shares took place as Obolon’s positions with their more affordable beer were getting stronger and two other national brewers of regional scale were experiencing significant pressure and their market share decline.

Regional companies’ performance can be fully explained by changes in their price segments of the market. Consumers’ higher interest to economy mass brands led to lower demand for Ukrainian beer costing higher than the average at supermarkets. Most of brands by independent breweries outside the home region belong to such beer. Certainly, the temporal lockdown of draft beer shops played its role too.

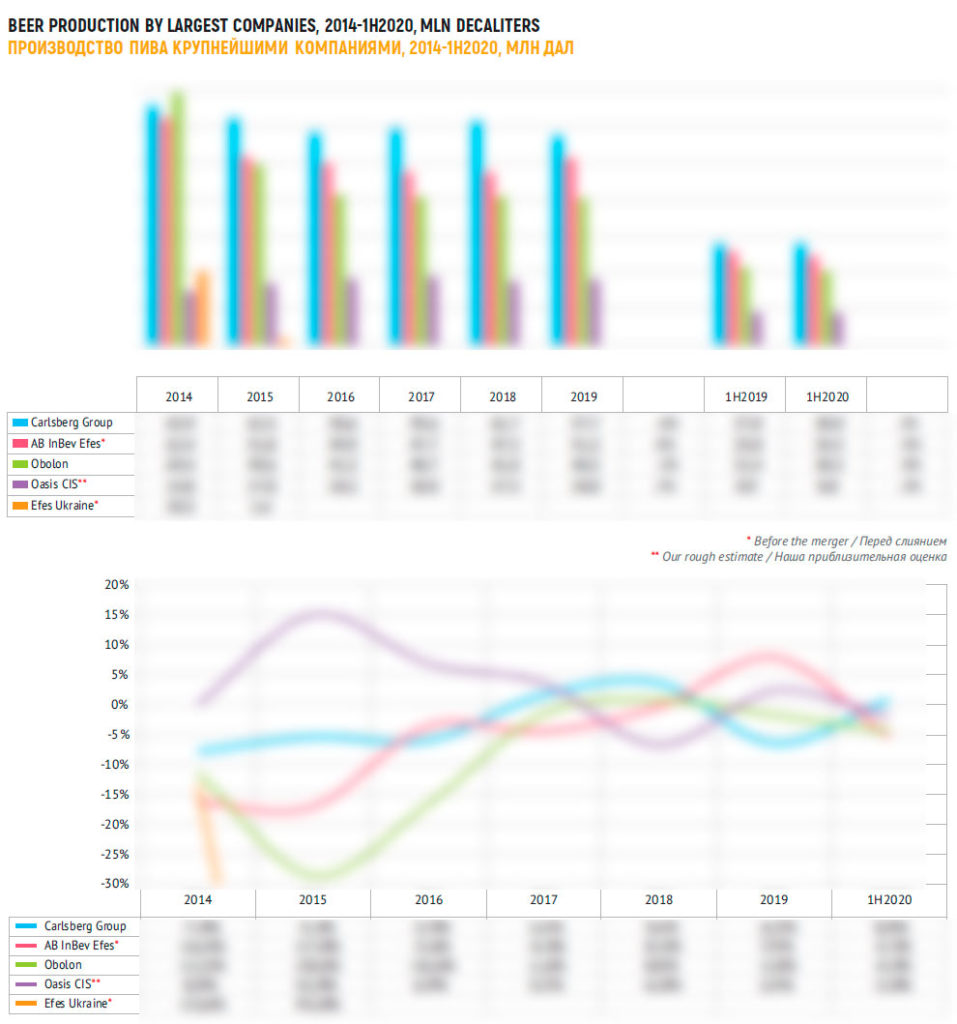

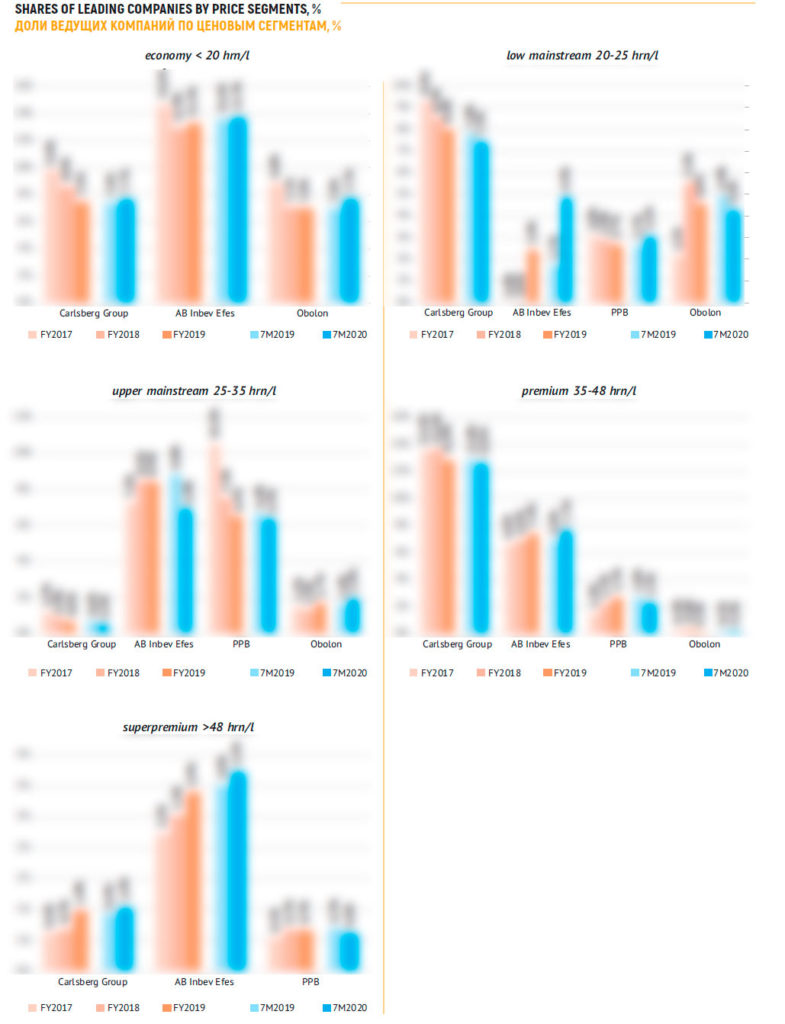

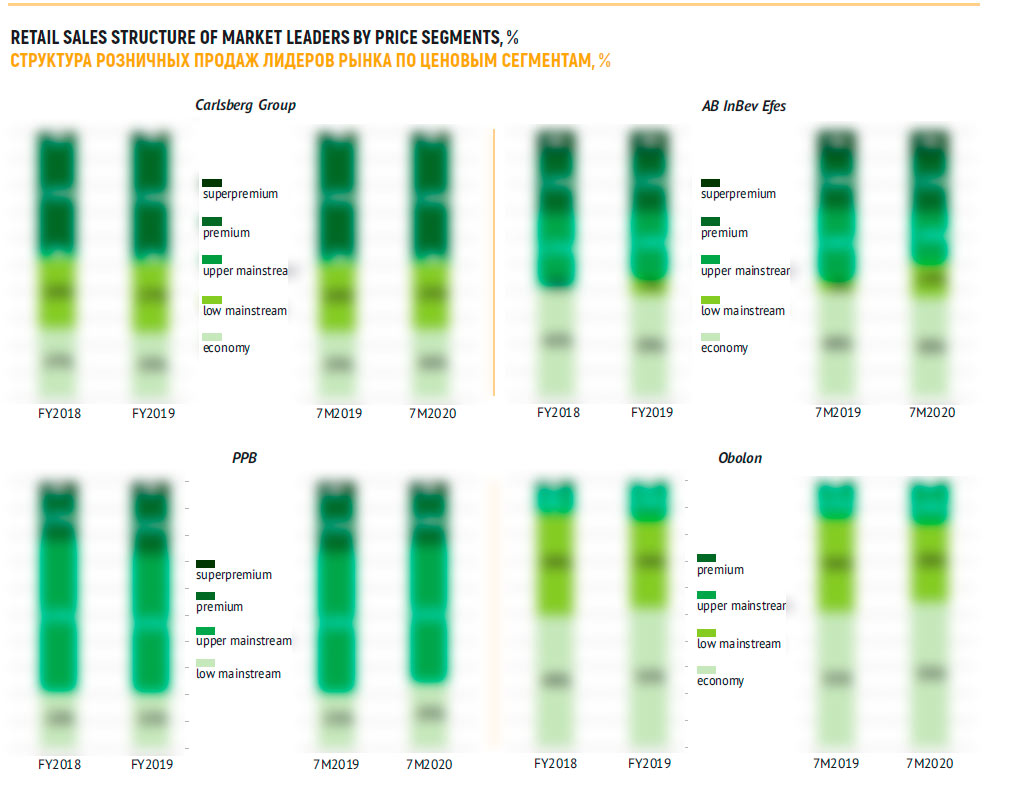

Carlsberg Group

According to the official data, in 2019, Carlsberg Group cut their alcoholic beer output by *% to **.* mln dal. The share in the net output volume fell by *.* p.p. But in the first half of 2020, the company expanded output by *% which, against the negative dynamics of the industry, resulted in a *.* p.p. growth to **.*% of the output.

Thus, Carlsberg Group kept their first position in the industry, though not long ago the company’s leadership was at risk.

The distributors’ data reflect the natural volumes reduction by *% in 2019, which matches the data on production. But, in the first half of 2020, a *% decline has been already registered, which does not quite fit even the minimum growth.

One should note that Carlsberg Group is in general focused at the premium segment. The average retail price of its beer is higher than that of AB InBev Efes and Obolon.

The average prices for sold beer remained rather high, despite the constant reduction of the market over 2019 until April 2020. In May, however, prices went down dramatically while Carlsberg Group market share on the contrary increased. Let us note that discounts were proposed not within a certain promotional campaign but for most the company’s key brands at the same time.

The prices for some brands collapsed more dramatically, though not for a long time (for example, Tuborg with a price falling by a quarter in May), while for others that decline was also significant but even more lengthy (Lwiwske Eksportowe and Lvovskoe ****) and Zhigulevskoe price went down to the lowest price level.

This step was tactic, perhaps in order to sell out stocks. Quarantine sale allowed to partially restore the lost volumes, though not to the previous year level.

As soon as in July, the company considerably exceeded other brewers by price. The price leadership makes the competition more difficult. They are probably gambling on marketing and trade marketing. But Carlsberg Group will have to put every effort not to drop their sales in the second half year.

Over the accounting period, some Carlsberg Group retail share decline took place due to isolated falls but all along the wide price spectrum.

Lengthy decline in the economy and low mainstream segments in January-July 2020 changed into a relative stability. Over the recent years, it has been rather difficult to compete with Obolon in the inexpensive beer market.

Thus, in the economy segment Zhigulevskoe share decreased and has not restored the volumes yet even after a sharp price cut. But this failure was fully compensated by Lvovskoe Svetloe growth. Minskae Zhigulevskoe went on losing the market share despite moving from upper to lower mainstream. At the same time, Lvovskoe **** has kept stability given the price reduction.

In general, the market share of Lvovskoe brand that accounts for almost a half of retail sales of the company is fluctuation with a big amplitude.

In the upper mainstream segment, in the cold season, good performance was shown by strong beer Arsenal that has started restoring the lost positions. Against that background negative performance of Baltika #* Strong seems to be not important. This sort along with Baltika #* Classic have been long pressed out of the market by competitors. It is possible that the same can happen to them as to Zatecky Gus that gradually disappeared from retail shelves.

Instead, three other sorts by Baltika belonging to premium segments have improved their positions and keep substantial market weight. The share of Baltika #* Non-Alcoholic is dependent on the season but during the warm season, it exceeded the level of the previous year. Besides, the growth wave of Baltika Draft Myagkoe exceeded that of the previous year. Baltika # * Export strengthening was even more notable. This sort provided the bulk of positive dynamics of umbrella brand Baltika.

If the company manages to keep Baltika share at least at the current level, due to the low-base effect of the second half of 2019, the brand will substantially strengthen its positions by the end of 2020.

Other premium brands by the company more or less dropped their market shares (though their negative dynamics did not outweigh the positive performance of Baltika). Thus, Seth & Rileys Garage probably reached the ceiling of potential in 2018 and now it is losing the market share. Possibly the interest to the brand will be supported by launching a new sort in June. Expensive special beer Slavutich has been long losing its market share. Tuborg positions are fluctuating as after a leap resulting from promotion, its market share started falling again.

In the superpremium segment excellent performance was shown by Kronenbourg **** due to among other things launching a new fruit taste.

In general, in the first half of 2020, the sales structure of brands by Carlsberg Group did not change much by the price segments except for slight polarization trend. But as for package segmentation, the production structure of the company has become more economical. The share of beer in PET has grown sharply at the account of glass bottle and KEG, yet the can share remains unchanged.

AB InBev Efes

According to the official statistics data, the volume of the alcoholic output at three AB InBev Efes breweries in 2019 grew by *% having amounted to **.* mln RUB. The share in the total output increased then by *.* p.p. However, as soon as in the first half of 2020, the production lost *% and the company share in the total output volume declined by *.* p.p. to **.*%.

Thus, lagging behind the leader increased to *%, though a short time ago, it seemed that the newly formed alliance would head the market.

Like in case with Carlsberg Group distributors’ data concerning AB InBev Efes sales are roughly equal by the end of 2019 reflecting a *% growth. But they do not match in the first half of 2020 as they register not a decline but a growth of *%.

At the same time, in the general foods retail according to independent assessment AB InBev Efes extended the gap with the major competitor and continues to be the sales leader.

During 2019, the price policy of AB InBev Efes was rather reasonable and only early in 2020 the average price started growing. However, due to dramatic changes in the market conditions, and in response to Carlsberg Group actions as well as other brewers, the company initiated a new cycle of price competition as in May, the average price for sold beer started decreasing. Besides, unlike Carlsberg Group’s violent maneuver, that reduction was gradual.

As a result, while in April 2019, AB InBev Efes beer cost *% less than that by Carlsberg Group, in July the difference reached **%. In general this difference fully explains the positive dynamics of retail sales. Though the effect of relaunching the brands that used to belong to Efes is still not exhausted.

Let us examine the dynamics of the company’s brands by price segments.

The mass and most requested beer sort in Ukraine is Chernihovskoe Svetloe. That is the cheapest sort in Chernohovskoe range and the demand fluctuations of this brand fully reflect the company’s positions in the economy segment. In the past season, the sort sales plummeted among other reasons due to cannibalism resulting from AB InBev Efes launching competing brands in the low mainstream segment.

However, the market share dynamics of Chernihovskoe Svetloe reflected as mirror its retail price dynamics. When in July 2019, the prices reached a local peak (**.* hrn/l) its share too reached the bottom (*%), and in July 2020, as the prices fell to **.* hrn/l the sort share went up to **%. Thus Chernihovskoe Svetloe has become the direct competitor to Zibert. But due to such step, the sort was able to change the decline in 2019 into growth, over the accounting period 2020. However, this growth was offset by Zhigulevskoe market share reduction, second grade and discount beer in AB InBev Efes product range.

AB InBev Efes succeeded mostly in low mainstream. In March 2019, the Ukrainian market saw the return of Belyi Medved brand. Before the beginning of military activity in the East, it had been produced at Donetsk brewery of SAB Miller. This brand can serve as a good example of how important brand awareness and the output geography are.

Let us note that due to the active advertising campaign that continued since 2013, as well as due to rapid distribution growth, the brand entered the national level at that time. There was a natural reduction of the market share from the east to the west. Currently, in the east of the country one can still see old refrigerators, tents and branded furniture featuring Belyi Medved.

It is no surprise that even taking into consideration a much developed distribution of AB InBev Efes the current market share of the brand replicates the pattern of * years ago. That is, the market share of Belyi Medved in the east is *-* times bigger than in the western Ukraine. As for other brands, there is also a regional link, but for example, Chernihovskoe brand had a *.* times difference.

In general, at the national level Belyi Medved market share has grown over the accounting period from * to *%. One can say that that brand was an engine of retail sales over the accounting period. The rapid transition from upper to low mainstream gave an additional growth driver.

In the upper mainstream the company did not manage to succeed. The negative dynamics was caused mainly by brand Rogan dynamics though the company seemed to have stabilized it in 2019. The rapid fall started in 2020 even before consumer behavior changed. Besides, negative dynamics was also noted for special sorts of Chernihovskoe brand. Probably, as the quarantine started, Ukrainians switched for simpler, basic beer sort.

Instead, in the premium segment AB InBev Efes had a good performance. On the one hand, the market share of several license sorts, in particular two Czech brands by the company.

Staropramen has restored its positions. Besides, having advertisement support and the low-base effect Velkopopovicky Kozel has gone on increasing though its share fluctuated strongly depending on promo actions. Excellent performance was demonstrated by another brand from former SAB Miller portfolio, namely Stariy Melnik beer. Bud share stabilized after a riot growth. Woman’s beer Essa (novelty of 2019) remains a niche sort as its market share is not likely to exceed *.*% by the end of 2020.

Besides, the performance of AB InBev Efes in the superpremium has been also positive. The market share of Stella Artois, Hoegaarden and Leffe brands have stabilized after a prolonged growth. Instead, Miller brand that is recognized by consumers after the previous launch to the Ukrainian market enjoyed a rapid market weigh gain.

We also could observe Corona brand market share grow which is quite unexpected from the psychological point of view and in spite of the news on its output cease in Mexico. That was the most considerable increase among superpremium brands and by mid-summer Corona brand share exceeded *% of the market. It makes us think that secondary negative connotations are not so important for sales as frequency of brand name mention.

If we look at AB InBev Efes sales structure by the price segments, we can notice a considerable change, that is, low mainstream share increase. On the other hand, this increase took place at the account of both lower and higher price levels, so we cannot say whether it had a negative or a positive effect.

In the beer output structure by the package one can see that shares of keg and glass bottle have decreased. On the contrary, the shares of “economical” PET-package and “premium” can have increased which in general coincides with changes by the general segments.

Obolon

According to the official data, in 2019 Obolon corporation cut the output volumes by *% to **.* mln dal. The share in the total output volume fell by *.* p.p. In the first half of 2020, the company cut the output by further *% which resulted in a *.* p.p. reduction of the output, to **%.

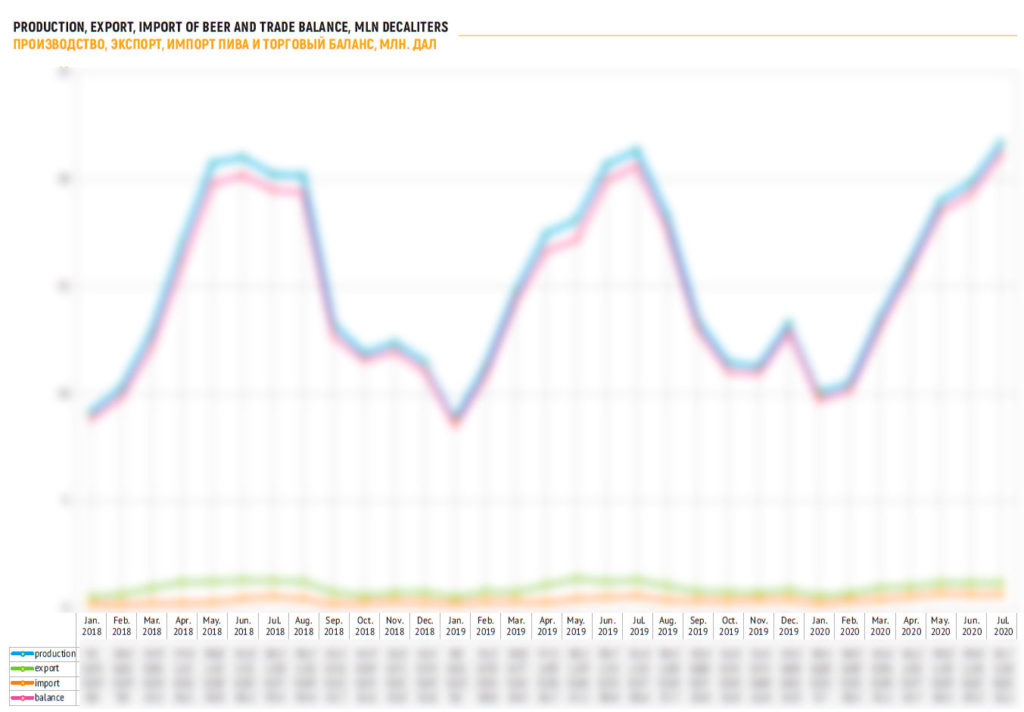

As Obolon is the main exporter of the Ukrainian beer, normally its dynamics hardly reflects the market position change. Especially today as the market conditions changed dramatically. In the first half of 2020, the Ukrainian export reduced by several per cents, that is, the trade balance shifted towards the sales on the inner market.

On the other hand, due to cooperation with ATB Obolon is the biggest supplier of beer under private labels, that lost some of their market share.

The distributors’ data reflect the growth of Obolon’s retail sales by *% in 2019 and a *% reduction in the first half of 2020.

The average retail price of the sold beer of Obolon is much lower than that of competitors because of the current focus at the economy segment. Over the previous year, the company made efforts to gradually rise the prices for the key brands. But at the same time, the market share during the warm season of 2019 remained roughly the same and started falling sharply in October. Then the company swiftly cut the prices and took measures to keep them. Consumers positively reacted to such steps and another discount in May 2020 gave additional impetus to the market share growth of Obolon.

Over the accounting period, Obolon’s positions in the economy segment have improved a little. On the one hand, being a major producer of Zhigulevskoe the company suffered more than others from consumers’ loss of interest to that peoples’ brand. On the other hand, the company own brands’ share have grown. They have managed to overcome the previous year negative trend having increased the share of Zibert beer. Besides, sort Obolon Kievskoe that had appeared on the market late in 2018 went on rapidly gaining the market weight.

However, in the low mainstream segment key sort Obolon Svetloe has found itself under a too strong pressure from a cheapened and fast developing Beliy Medved as well as from cheapened Minskae Zhigulevskoe. Due to fiercer competition Obolon Svetloe has lost *% of the market.

In the upper mainstream segment, the market share of light youth brand Hike has continued growing. Instead, the market share of strong “male” beer Desant has been decreasing slowly.

As a result of all these alterations, Obolon retail sales have polarized by the price segments. That is, the final changes in the brands portfolio can be considered neutral.

In production allocation by the package there has been a sharp slant towards beer in PET, and it accounted for */* of Obolon output over the accounting period of 2020. Obviously sales of beer in glass bottle flowed to plastic. But we can also observe the growth of can. As we can see, these changes adequately reflect the price segments dynamics. The share of beer in kegs decreased by * p.p. at one stoke.

PPB and regional producers

Persha pryvatna brovarnia is a national producer that is well represented in marginal segments of the beer market. We do not know the company’s operating data for 2020. But, under our rough estimation, based on the regional statistics, in 2019, PPB expanded their beer output by *% brewing about ** mln dal of beer.

PPB retained higher average prices of the sold beer than those of competitors in the first half of 2020. However, in July, it was left behind by Carlsberg Group that, by that time, had finished “quarantine sales”.

Judging by PPB brands the mode of consumer cost saving has resulted in sales slant to mainstream. It mostly happened due to popularity growth of inexpensive brand Zakarpatskoe. Both sorts of title brands by the company and license brands experienced diverse and ambivalent fluctuations.

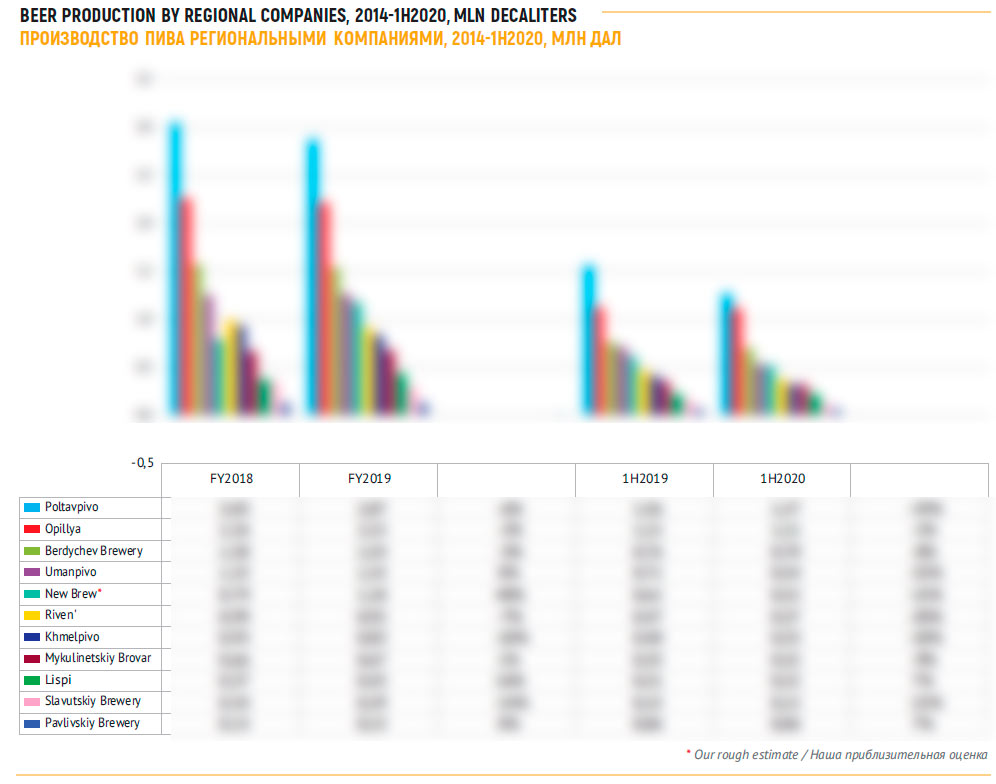

The first half of 2020 was unsuccessful for most of independent region-scale breweries. The volumes decreased to various extent at * out of ** businesses that we considered and their net output fell by **%.

Let us look at the dynamics of four comparatively big breweries outputting more than * mln dal.

Firma Polatvpivo has continued losing the output volumes. But, while in 2019, the reduction amounted *%, in 2020 it is already **%. Some time ago, the company placed stake on packed beer and regional expansion with a wide brand range, and that strategy paid off. The current decline, if we speak only of the retail sales, was caused by an obvious reduction of distribution level especially in the modern trade in the east of the country. In this connection the market shares of virtually all brands have gone down considerably.

The operational results of Ternopol brewery Opillia were stable by the end of the previous year, and in the first half of 2020. *% decline in the new conditions can be considered a good performance. At the same time, there was a noticeable reallocation of output volumes in favor of PET (at the account of glass bottle reduction). The company is well represented in the retail all over Ukraine. They managed to increase distribution in networks in the second part of 2019, but yielded a little in 2020.

Berdichevskiy pivzavod had no output volume changes in 2019, yet over the accounting period, the production has fallen by *%. Besides, the retail prices remained at the same level, which against the fiercer competition could have become the main reason for Berdichevskoe market share decline. In the net output volume of the company the share of PET has increased like at other brewers.

Umanpivo productionin the first half part of 2020, fell by a quarter at one stroke. That could be caused by an abrupt decline of representation during the strict quarantine. In general the local drop took place in southern and eastern regions of the country. Higher retail prices starting from the autumn 2019 could have played a considerable role. In the company’s structure of output the share of keg has fallen notably and PET on the contrary has gone up given a relatively stable glass bottle share.

Besides in Cherkassy region there is New Brew brewery that belongs to actively developing New Product Group. The group manufactures a range of product categories and beer is one of them. Under our estimation basing on the regional data, in 2019 New Brew increased the output volumes by nearly **% to *.* mln dal. But beer products are positioned in the marginal market segments, that is why due to the market segment situation, in the first half of 2020 the reduction amounted to **% according to our estimation. In summer 2020, New Brew reported of new brand Zhashkovskiy Kaban that rapidly has expanded its distribution. Probably it will help the company to even the dynamics by the end of the year.

To get the full article in pdf (24 pages, 20 diagrams) propose you to buy it ($40) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.