TEN years ago, the Singapore Exchange (SGX) scored a coup. Thailand’s largest brewer Thai Beverage, or ThaiBev, ditched plans to list in the Buddhist nation for the Singapore bourse, following protests back home against its alcohol-centric business.

The ThaiBev initial public offering (IPO) raised S$1.4 billion. It became Singapore’s largest IPO since the listing of telco giant Singtel in 1993. The listing also diversified the profile of SGX, which was becoming dominated by Chinese IPOs.

A decade later, ThaiBev has fulfilled its promise to Singapore investors who bought its IPO shares at 28 cents apiece.

The company has already paid out around 14 Singapore cents a share in dividends through the years. And it was trading above 90 cents a share last week – a stunning rise from 20-odd cents just five years ago.

ThaiBev has become one of the hottest stocks among institutional investors. Credit Suisse, a bank which services institutional clients, initiated coverage on May 10 with an “outperform” call and a target price of 85 cents. A few days later, analysts would raise their target prices after ThaiBev reported strong first-quarter results. Credit Suisse’s target price is now 90 cents, while DBS raised its target from 82 to 92 cents.

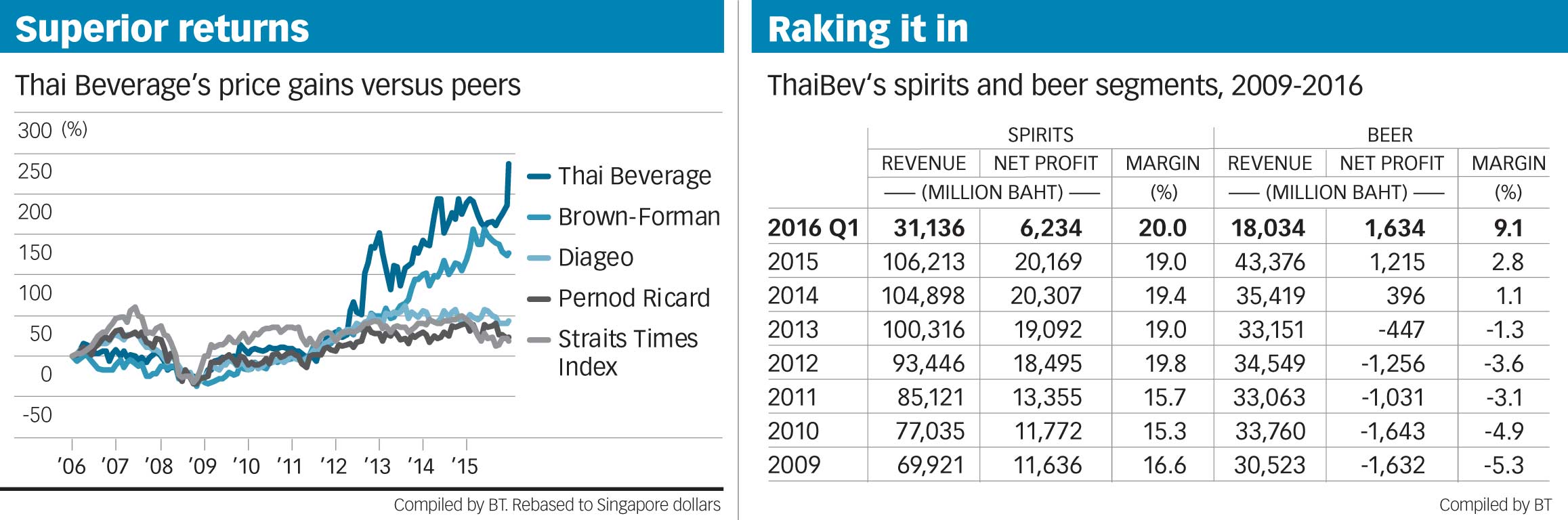

ThaiBev always had a dominant position in Thailand’s spirits market. Spirits made up the bulk of its profits. But the segment, selling products such as the popular Ruang Khao, was seen as a no-growth business. The Thai spirits market has grown at a steady but unexciting 2 per cent clip a year in the last 10 years.

What sparked the latest bout of optimism was ThaiBev’s successful relaunch of its Chang beer brand last year. ThaiBev sold 273 million litres of beer in the first three months of the year, up more than 60 per cent from a year ago. It increased prices, too.

As a result, beer segmental revenues rose from 10.5 billion baht to 18 billion baht, a 71 per cent increase. Segmental net profit went from 0.6 billion baht to 1.6 billion baht, an increase of 175 per cent. (One billion baht translates to around S$40 million.)

Overall Q1 revenue was thus up 21 per cent year-on-year to 55 billion baht, while net profit, excluding associated companies, was up almost 30 per cent to 7.7 billion baht.

After posting the results, ThaiBev shares surged 10 per cent last Monday and more than 10 per cent intraday on Tuesday to over 90 cents. They settled at 87.5 cents at the end of the week, a weekly change of 16.7 per cent. This makes the stock the top performer among its alcohol-selling peers in the past week and month.

This week, we briefly revisit the story of self-made Thai billionaire Charoen Sirivadhanabhakdi, the man behind the company.

We then try to figure out the thorny question of what is a reasonable price to pay for the firm, while highlighting a few other options out there.

The Charoen story

Born in 1944, Mr Charoen was sixth among the 11 children of a Chinese street vendor hawking mussel pancakes in Bangkok’s Chinatown.

By age nine, he was already selling a lottery-like game to neighbourhood kids, according to a Forbes profile in 2005. He then started a trading business, and began supplying products to a government-owned distillery producing Thai whisky.

In a significant move in the early years, he successfully obtained rights to produce for 15 per cent of the market, thus becoming a distiller in his own right.

In 1985, the remaining licences for 85 per cent of the liquor market were opened up for bidding. According to the Forbes article, Mr Charoen’s business vehicle Thai Charoen Corp, or TCC, borrowed US$200 million and won all the concessions. In one stroke, he established a monopoly in distilled spirits in Thailand.

TCC’s beer story started later in the 1990s, when the Thai government liberalised the beer market. Mr Charoen initially partnered Danish brand Carlsberg to make and distribute the tipple in Thailand.

But Mr Charoen was soon making his own beer, dubbed Chang or Thai for “elephant”, around 1995 to 1996.

At that time, Singha, or the “lion” brand, had a stranglehold on the Thai beer market. Singha was made by the venerable privately owned Boon Rawd Brewery.

But Chang, Mr Charoen’s working-class label, was cheaper, stronger in alcohol content, and sold well in rural areas.

The upstart Chang took advantage of the complacency of the sleeping lion, especially during the Asian financial crisis of 1997 that hit Thailand hard. Chang, cheap and good, had wrested a majority of the beer market share by 1999, and maintained that position for a few years.

Faced with Singha’s decline, Boon Rawd fought back through its cheaper Leo beer brand, which did very well. Chang’s market share declined from 64 per cent in 2003 to 31 per cent in 2009, around where it has stayed in the last few years, based on estimates made by Credit Suisse.

CIMB noted in its May 18 report that before the rebranding of Chang last year, Leo had a market share of 51 per cent. CIMB analyst Kenneth Ng, who co-authored the report, tells us that Chang’s share was 30 per cent, while Singha was at just 10 per cent.

Meanwhile, amid a growing Asia, Mr Charoen’s ambitions ranged far and wide. Even in 2009, Mr Charoen had apparently considered acquiring stakes in Singapore food and beverage and property conglomerate Fraser & Neave (F&N) and Tiger beer maker Asia Pacific Breweries (APB), from OCBC and Great Eastern. APB was itself a long-running joint venture between F&N and Dutch beer giant Heineken.

In 2012, Mr Charoen finally got his way and the deal went through. He grandly upset the order of things, triggering a bidding war that became one of Singapore’s most exciting corporate stories in recent memory.

It all ended with Heineken acquiring APB and Mr Charoen adding what’s left of F&N to his business empire. Hence, ThaiBev now owns stakes in F&N and its property spinoff, Frasers Centrepoint Limited.

Meanwhile, Mr Charoen’s TCC group is also involved in industry, agriculture, finance, insurance and real estate.

Valuing the elephant charge

Last year, Chang’s various brands were consolidated and rebranded as Chang Classic. Lighter in alcohol content, less bitter, and presented in modern-looking green bottles, Chang Classic targeted a younger and wealthier age bracket.

The tactic worked. Chang’s end-March market share has risen to around 40 per cent, according to management.

As Chang finally rakes in the dough, the biggest question on investors’ minds should be the sustainability of its market share gains.

Investors should first note that the spirits segment that the company monopolises in Thailand still contributes the bulk of its profits.

In the latest quarter, amid significant improvement in the beer segment, spirits still contribute about four-fifths to net profit, and beer, about one-fifth.

On the revenue side, spirits make up over half, and beer, about a third.

But spirits are far more profitable to make, with a net profit margin of close to 20 per cent in recent years.

Beer has long been underperforming, making bottom line losses till 2014. Its net profit margin, in a stellar Q1, is now in the high single digits.

If beer can keep up its performance in Q1 for the entire year, ThaiBev could see beer contributing some six billion baht to its bottom line this year. Assuming the spirits net profit contribution stays at around 20 billion baht, we are already talking about a substantial 26 billion baht of net earnings a year.

Now, alcohol companies typically trade at over 20 times earnings. Assuming an earnings multiple of 20, we get a value of over 500 billion baht for ThaiBev’s spirits and beer operations alone.

Divide that by 25 billion shares in ThaiBev’s issued share capital and you get a value of 20 baht a share, which works out to 77 Singapore cents a share – 62 cents from spirits and 15 cents from beer.

Don’t forget that ThaiBev’s associate company stakes in F&N and Frasers Centrepoint Limited also have a total market value of around 9 cents a share, given current market prices for both companies.

Thus the recent surge in ThaiBev shares can be explained.

If the good beer run can be sustained this year and does not grow further, spirits contributes 62 cents to ThaiBev’s value, associate companies add 9 cents, and beer, 15 cents, for a total of 86 cents a share.

Given that beer can add 15 cents a share, ThaiBev’s surge from under 70 cents to more than 85 cents a share thus makes sense.

To make a case for even higher valuations, you need to be a raging bull on ThaiBev’s beer segment. Concurrently, you can argue that the company is worth much more than 20 times earnings.

The first scenario requires an assessment that management can defend its increased market share in beer, a position it has not enjoyed for some time. One would hope that the allure of Chang Classic will not fade, beyond the initial advertising and promotional push.

The second scenario is out of management’s control but more a function of financial markets. A scarcity of dividend-paying consumer stocks could push investors across the world into ThaiBev’s arms.

The world’s priciest alcohol stocks now trade between 25 times (Kirin, Tsingtao) to 28 times (Remy Cointreau, Brown-Forman). Assuming 25 times annualised Q1 earnings of its spirits and beer business alone, ThaiBev is worth a whopping S$1.20 a share.

Another future growth area is the company’s lossmaking non-alcoholic beverages segment, known for its Oishi green tea. Sales there, in a hyper-competitive market, are growing at double-digit rates, driven by sales of Crystal drinking water and Jub Jai herbal tea. But advertising and promotional costs have eaten away much of the revenues.

To sum up, based on its steady spirits business alone, one can make a case for ThaiBev’s valuation to be at least 70 cents a share, which is its spirits segment valued at 62 cents and its associate companies at nine cents.

It looks unlikely that ThaiBev will fall below 70 cents anytime soon.

In a bullish scenario, including sustained beer performance and earnings ratios moving up to 25 times, we can see the stock moving up to more than S$1.20 a share, above which we can deem the counter expensive.

Most likely, beer segment performance will diminish as Singha beer makes a comeback.

Beyond a five-year time horizon, who knows? Just ask the ThaiBev IPO investors who are still holding on to the stock.

Perhaps F&N’s 100 Plus will be a hit in Thailand. Perhaps ThaiBev’s Japanese restaurants segment will grow. And perhaps it will make another canny acquisition in South-east Asia that has growth potential like Vietnam’s Sabeco Brewery (of Saigon Beer and 333 Beer fame) and Vinamilk, a dairy giant.

What is certain is this: Good brands are rarely on the market. When they are, a terrific premium has to be paid. Don’t count on the acquisition route to grow ThaiBev, but rather good old organic growth and savvy business strategy.

Other alcohol giants

Speaking of good brands, potential investors in ThaiBev have to compare the company’s concentration in Thailand with some of the truly diversified global firms out there.

The first one, and probably the best known, is UK-listed Diageo. You might not have heard of ThaiBev’s Mekhong spirit, but chances are you will know of Johnnie Walker, Smirnoff, Baileys and Guinness.

The second is France-listed Pernod Ricard. Its top two brands will also be familiar to most people: Absolut Vodka and Chivas Regal.

The third is US-listed Brown-Forman Corp. Its top selling brand is Jack Daniel’s Tennessee Whiskey.

These firms are in innumerable countries around the world, and their brands are in such entrenched positions that they are highly profitable. This means they can charge premium prices while maintaining market share, returning much money to investors.

For instance, their operating profit margins are 26 per cent (Pernod Ricard), 28 per cent (Diageo) and 33 per cent (Brown-Forman).

ThaiBev’s operating margins are not too far behind for its spirits segment, at 25 per cent in Q1. There’s room for improvement. In the meantime, the company is trying to get its beer and other businesses – which can be a drag on various profitability metrics – up to speed.

The biggest advantage the three firms cited have over ThaiBev is their geographical diversification. There is country risk. A sharp depreciation of the baht will hurt ThaiBev’s valuations. Given political turbulence in Thailand, this scenario is not unthinkable. By contrast, a diversified geographical reach means differing revenue streams, and investors can sleep a bit more soundly at night.

Diageo, too, is trading at a slightly lower valuation of 19 times earnings, though it is growing at a slower pace compared to ThaiBev.

In terms of relative valuations, Brown-Forman is the most expensive out of the three international stocks, but it is also the most profitable.

Of course, ThaiBev can be the next Diageo. It is working on international export markets. There is no certainty of success here.

Yet it is exposed to South-east Asia, one of the fastest growing regions in the world.

Such is the tradeoff investors have to make. ThaiBev offers an alluring growth opportunity. It is priced reasonably by international standards, and there is no more country risk dragging down its valuations.

Meanwhile, Thais like to drink.

ThaiBev’s biggest disadvantage is that it hasn’t gone international, and it is too exposed to Thailand.

Yet one thing is certain. SGX has a winner on its hands.