Production and sales

Before speaking of the data published in the official reports by National Bureau of Statistics of China (NBSC below), let us pay attention to one peculiarity. Firstly, they can change significantly due to updating. Secondly, the percentage figures of the production or sales dynamics, calculated basing on the published volumes can differ considerably from the published growth/decline rates. By the way, significant discrepancies can be found not only in China but also in the neighboring countries for example Vietnam or India.

Before speaking of the data published in the official reports by National Bureau of Statistics of China (NBSC below), let us pay attention to one peculiarity. Firstly, they can change significantly due to updating. Secondly, the percentage figures of the production or sales dynamics, calculated basing on the published volumes can differ considerably from the published growth/decline rates. By the way, significant discrepancies can be found not only in China but also in the neighboring countries for example Vietnam or India.

The changes may have been caused by delay in getting or processing data from enterprises. Probably, the data first come from the major producers and the performance of the minor ones is accounted in the operational data, and added later.

That is why one can either calculate the data on her own or rely on the official estimations of growth and decline and stay in “the official frame”, despite the obvious discrepancies in figures.

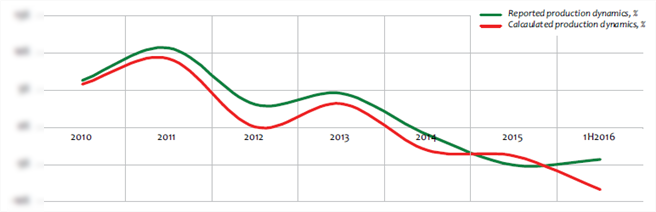

Year 2015. According to the official data by NBSC, in 2015, the beer production fell by 5.1% to 471.57 mln hl.

Besides, NBSC publishes data on beer sales. According to the official data, they decreased by 0.7% to 469.37 mln hl. At the same time, the estimate shows a 5.0% decline, as in 2014 the sales totalled 493.93 mln hl.

Besides, basing on the foreign trade data, we can calculate the trade balance, which would theoretically reflect the size of the domestic market (production+import-export).

In order to make the estimation independent from updating, we calculated the production volumes for 2014 taking into account new data on the 5.1% growth dynamics. Then the result of the trade balance in 2015 will be less by 4.7%. That is, the estimated market decline was a little less than the production decline due to the fast increase of import supplies.

First half of 2016. Last year saw an uninterrupted decline, yet it was the deepest during the first half of 2015. Potentially, it should have led to the low base effect and positive trend in the first half of 2016. However, according to the official data by NBSC, the beer production decrease in China is continuing approximately at the same rates. From January till June 2016, the decline stood at 4.3%, which means the persistence of the negative factors.

If we compare the operational data for 2016 to the volumes of 2015, the estimated production decline will be twice bigger, that is, 8.4%. Such difference can again be explained by the operational data being not final and liable to addition. That is why the production decline calculated by comparing the old updated figures and new operational ones, seems to be underestimated.

The market dynamics, estimated as the trade balance in first half of 2016 is -4.1% that is, reflects the continuation of the fast growth of beer import to China.

")

Prices and market by value

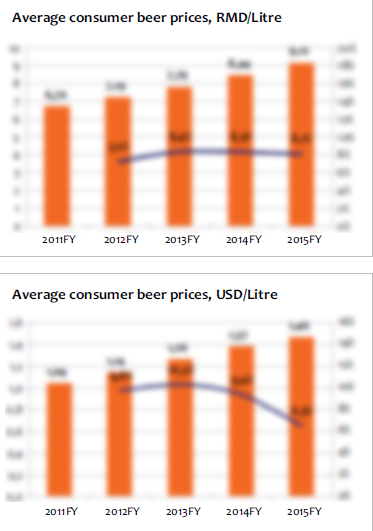

According to the monitoring data for 36 major cities in China, in May 2016 as compared to May 2015, retail prices for beer in a glass bottle of 650 ml went …% up to … yuan per liter. During the same period, the average prices for a beer can of 350 ml fell by …% to … yuan for a liter. Whereas the retail price for beer in a glass bottle was growing rather steadily and the price for canned beer remained practically at the same level during most of the year.

However, the market–value-weighted average for beer in 2015 was growing rapidly driven by the premiumization trend (see the next chapter “Market segmentation”). Under our estimate, it increased by …% to … yuan for a liter, that is why, continued growing at nearly the same rates.

Because of the yuan devaluation, the beer price increase in dollars amounted to …% to $… per liter.

The sold beer price increase allowed complete compensating of the natural volumes decline. By value, the beer market in 2015 expanded by …% and reached … bln yuan, under our estimate. In dollars, the market increased by …% to $… bln.

Market segmentation

Under our estimate, based on data from produces and research companies, …% of the Chinese market belongs to the economy segment, that is, sorts averagely costing less than 8 yuan per liter. By value, the share of inexpensive beer amounts to …%. The economy segment is rapidly shrinking by volume, which is the sole reason for the Chinese beer market decline. Under our estimates, it went …% down by volume and …% by value, that is, the decline rates remained at the level of 2014.

Other segments, where average beer price exceeded 8 yuan, showed growth. And there was a direct link between the growth rates and beer price. The middle-priced Chinese brands went on growing at medium rates and licensed international brands enjoyed a rapid growth. Mainly it resulted from sales redistribution of various sorts of the same brands. For instance, “draft” and “fresh” beer in bottle is still taking share from economy “usual” sorts. There was also a fast sales growth of licensed international brands, Budweiser and Tuborg. Import beer shone out particularly, as it has already become a significant market growth driver in monetary terms.

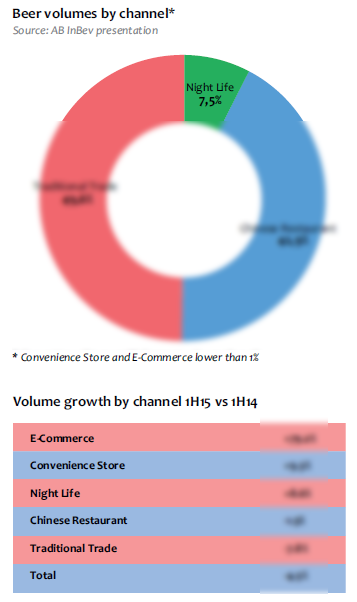

As to the places of beer purchase and consumption, the Chinese market is currently divided in two parts. In the on-trade segments, that is, approximately half of beer by volume is drunk at HoReCa establishments. For instance, according to AB InBev in the first half of 2015, about …% of the market accrues to restaurants of different scale and class and …% to “night life”. Accordingly,… of the sales is retail (off-trade).

Among the beer outlet channels, off-trade suffered the most. Thus, in retail the sales fell by …% compared to 1H2014. In the off-trade the situation was stable. Restaurants registered only a minor decrease amounting to …%. Night clubs demonstrated an excellent growth of …% in contrast to other big channels.

Such beer sales dynamics in E-Commerce is linked to the fact that modern and educated city dwellers increasingly prefer to buy foods via the internet. The main beer volumes are sold via the major online-supermarkets, namely, Yihaodian, Tmall Global, and JD. One should note that beer is not a top-priority, as most often online-buyers put fruits and milk into their baskets. But like at supermarkets, convenient choice and easy purchase allows forming a big order of various goods, including beer.

E-Commerce development opens up wide vistas for selling expensive beer sorts with low rotation and will promote further market premiumization. It is easier for importers and craft brewers to expand their product range and cooperate with on-line shops than to get their products on supermarket shelves. And expensive beer buyers can quickly find info and review on a product in the net.

By value, the on-trade segment is much bigger than the off-trade due to different traders’ margin. Naturally, the markup depends on the price segment, the format of the establishments selling beer, and the consumption style. It is one thing when beer is bought to wash down a meal at a cheap diner and quite another if it is bought to spend time at a night club. One can specify only the average and approximate difference. Thus, in HoReCa, mass medium-priced and economy brands cost usually …% more than in retail. Licensed premium beer is twice more expensive than at a shop and the superpremium brands are three times more expensive.

By value, the on-trade segment is much bigger than the off-trade due to different traders’ margin. Naturally, the markup depends on the price segment, the format of the establishments selling beer, and the consumption style. It is one thing when beer is bought to wash down a meal at a cheap diner and quite another if it is bought to spend time at a night club. One can specify only the average and approximate difference. Thus, in HoReCa, mass medium-priced and economy brands cost usually …% more than in retail. Licensed premium beer is twice more expensive than at a shop and the superpremium brands are three times more expensive.

The current fast growth of expensive beer sales is attributable not only to HoReCa. To a big extent it resulted from the modern retail which is striving to compensate the decrease of natural volumes by means of expensive beer. For example, just several years ago, the main sales channel for imported beer in Beijing was the night life market. But now the situation has changed, as import beer brands are easy to find in the retail.

There is also a clear dependence of beer sales in HoReCa on its price. And it has a very easy explanation – amid other people, during public recreation, it is important to emphasis one’s status and drink an expensive branded beer. Import, premium, licensed (and currently craft beer) in many Chinese’s opinion reflects the modern Western consumption style and good taste and allows casting oneself as a successful person.

At the same time, when we speak of the on-trade segment, we mainly mean not the draft but bottled beer. In China draft beer is considered to be fresher and tastier, but its market share is only …%. And in the total volume of the on-trade sales its share is only about …-…%.

The relatively low popularity of the draft beer can be explained by its high average price, which sometimes exceeds bottled beer multi-fold. The filling equipment from kegs is not affordable for many small HoReCa establishments that sell inexpensive beer.

Besides, two other major problems are controlling the rotation and shelf life of keg beer (which is much shorter than that of bottled beer) as well as adequate logistics of returnables. Complex and multileveled sales system is a famous peculiarity of the Chinese market.

Thus, prospects of the keg beer sales are so far mostly connected to brewers’ searching for the ways to increase the gross profit.

Though the exact numbers of canned beer sales on the Chinese market are not available, judging by companies’ reports, it has been actively ousting bottled beer from the market. The can share under our estimation exceeds …% already.

Next: Who and how much drinks beer in China?->

To get the full article “Analysis of beer market in China” in pdf (60 pages, 65 diagrams) propose you to buy it ($45) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.