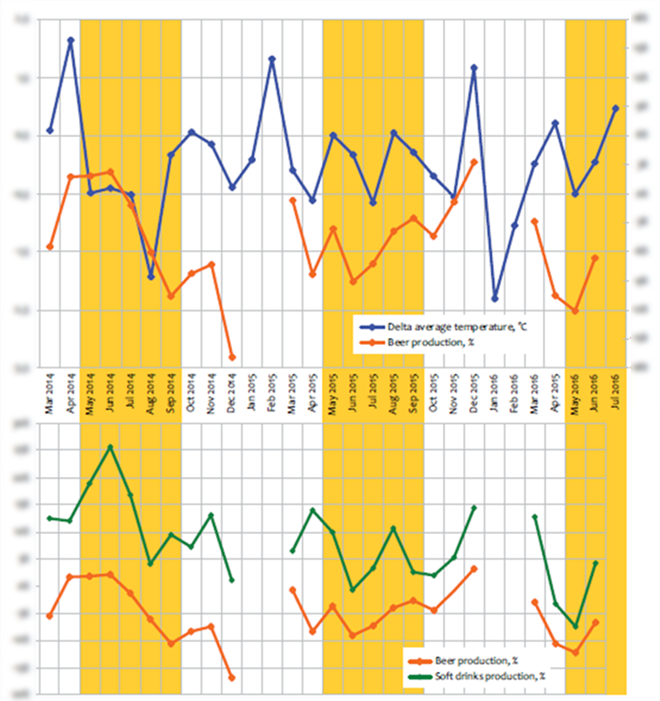

Beer is a seasonal product. The sales level is dependent on the weather: the hotter it is, the higher demand for beer, water, and soft drinks is and vice versa.

Over the recent 3 years, weather has been often mentioned among the reasons for the decline in beer production and sales, though it is clear that it cannot be a constant negative factor.

As we have already noted, better dynamics in 2013 conflicts the social and economy context and the link between the beer market and the GDP. The reason is obvious – unusually hot summer breaking temperature records.

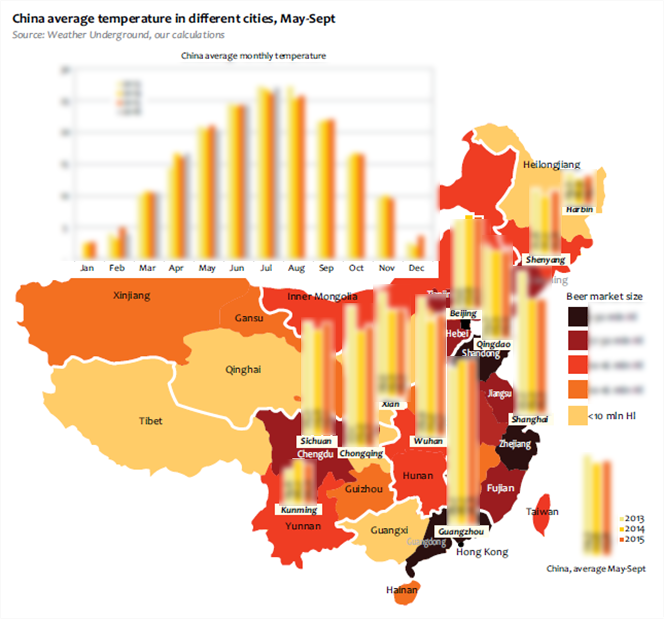

The area of the temperature anomaly is located in the eastern China. While it was just hotter than average in Beijing located to the north of this territory and in Guangzhou located to the south, territories from Shanghai to Xi’an broke temperature records for the recent 140 years. The prolonged spell of scorching temperatures is a result of stationary high pressure off the eastern coast, which has prevented tropical moisture from delivering normal summer rainfall.

As we match the temperature fluctuations to the production dynamics since 2012, we can conclude that if not for the weather affect, the dynamics would have looked like a smoothed curve or even straight line, that is, a gradual transition from growth to stagnation and decline.

The hot summer of 2013 created the high base effect. In 2014, when the weather was usual, it cannot support the beer sales. The simultaneous decline of the average price and the beer production dynamics from June to September 2014 can be seen at the graph*.

* In order to calculate the temperature, we used the weather monitoring archive data for 11 cities which in our view reflect the general situation in the country: Beijing, Shanghai, Chengdu, Wuhan, Kunming, Guangzhou, Chongqing, Harbin, Xi’an, Shenyang, and Qingdao. For daily data in each of the cities the monthly temperature average was calculated, then, the average for city data was calculated.

In order to check if the weather really played such an important role, let us analyze the dynamics of demand change for another seasonal product and beer rival – soft drinks. We can see the obvious connection between their production dynamics and beer output in the high sales season.

In 2015, the weather was rather favorable to the brewers’ sales. On an average in the country July was a little cooler versus 2014, yet the other months of the season were hotter. As for the weather, the base effect of 2015 can be considered neutral or moderately negative.

However the season of 2016 started not very well, and by the end of July we can speak of a pronounced negative effect not only for beer sales but for the country’s economy in general.

The weather in May in the central and eastern regions was comparatively cool, which had a minor negative effect on the production dynamics. In June, the temperature was already at the level with 2015, and in July it became much hotter. The number of days with precipitations in 2016 increased in April and May, but decreased in June and July. However, this year not the rainy days number but precipitation quantity matters.

Every year heavy rains in China occur along the seasonal Mei-Yu (“plum rains”) front extends from eastern China across Taiwan into the Pacific south of Japan. Associated with the southwest monsoon, these rains typically affect southeastern China from mid-May to mid-June and northern China during July and August.

In July 2016, record-breaking heavy and incessant rains caused dramatic floods in central and eastern regions of China. Torrential rains affected 33 million people in 28 provinces, submerging huge areas of cropland. Heibei province population suffered the most.

Heavy rains could not substantially affect beer production and sales in the first year half 2016, but will seriously influence brewers’ performance in the second half of the year.

Next: Beer among other alcohol drinks->

To get the full article “Analysis of beer market in China” in pdf (60 pages, 65 diagrams) propose you to buy it ($45) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.