The review contains an analysis of interim performance of brewers in the first half of 2019. There are rather dynamic changes behind a modest industry growth. Baltika is again experiencing a stage of volumes and market share slid due to competition with AB InBev Efes. Because of the price competition and presence expansion in the modern trade company #2. has come close to the leading position. At the same time sales of Heineken Russia have continued growing which makes the premium part of the portfolio heavier. The market premiumization trend had been also confirmed by import brands. MBC and Zavod Trekhsosenskiy have been the most successful among federal market players. The market share of independent regional brewers and Ochakovo have continued falling as they are being squeezed out by the market leaders at their competitive fields.

General situation at the market

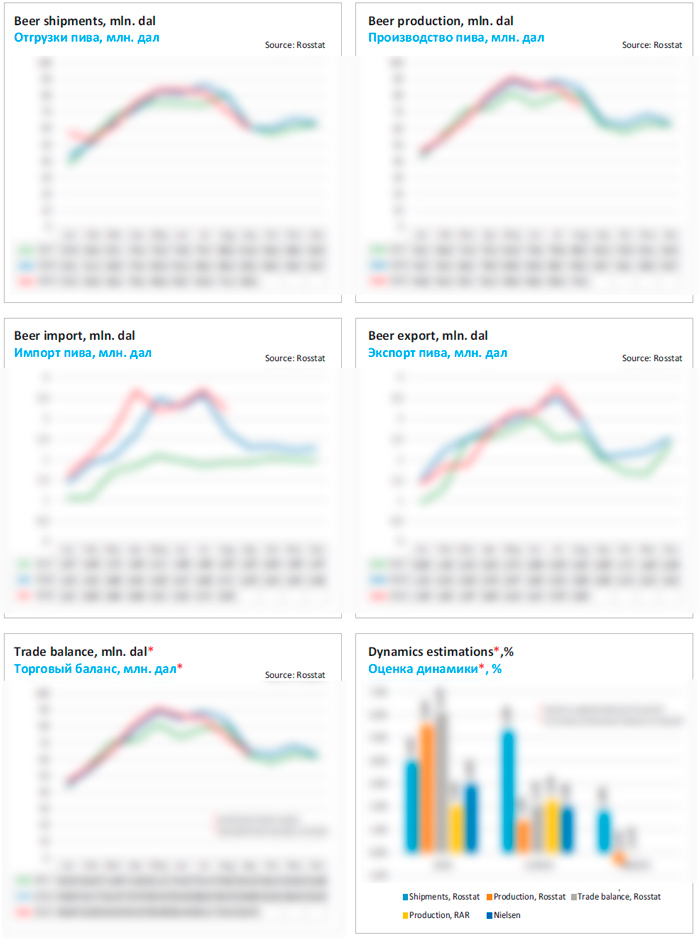

For brewing industry performance of 2019 was confirming of the previous year results, as the world football championship set up a high base. Measured by different data, beer production in the first half of 2019 increased by .-.%.

Volume assessment of sales in the first half-year fluctuated from nearly zero by Rosalkogolregulirovanie (RAR) to +.% for audit of retail trade of Nielsen and the same 2% for estimated volume of trade balance (production+import-export).

Low growth in the first half of 2019 to a big extent is connected to slid of volumes by independent regional brewers. Under our estimation, their upward trend was at the highest point in 2015-2016 (excluding crisis in 2014) and got the opposite direction in 2017-2019. In the first half of 2019, breweries with Russian capital* had net output volumes totaling .%. Though in 2018 they were still growing – by only .% against the .% of the market.

* Including Ochakovo and Tomskoe pivo, excluding Zavod Trekhsosenskiy

Currently many regional brewers speak about fierce price pressure from major companies. For instance, there is a growth of volumes of shops near the house, particularly alcomarkets and discounters belonging to big federal chains where beer by limited number of key suppliers is sold at low prices.

Besides, regional brewers are experiencing price pressure because of steady promoactivity at supermarkets and through lowering of retail price for separate economy brands. Yet, while in the previous year powerful competitive pressure was exerted by … and …brewery, currently …has come to the foreground.

Besides, federal and regional brewers complain of growing market of cheap undeclared beer and unofficial transborder trade.

Fiercer price competition was the reason why the average retail price for beer in the first half of 2019 stayed almost the same versus 2018 (+.% to …. RUB/l) according to data by brewing companies referring to Nielsen. In prior years the rates of price rising was several times higher.

There has been further growth of premium local beer (to a smaller extent) and import beer (to a bigger extent). Thus, the import beer volume in January-August 2019 went ..% up and the range also extended. By the end of 2019, the import volume is likely to exceed .. mln dal and the market share will apparently hit at least .%.

If we look at the situation in general, we will see two opposite trends – premiumization from one side and slowing of price index on the other side. Yet, this opposition is smoothed by the fact that brewers’ promoactivity and the border blurring led to the general shifting of the price structure towards the economy side. More marginal brands by keeping retail prices won the market share of more affordable brands in the neighboring price segment. This trend is more notable for import and license beer. As a result, the premium segment went up, but became less premium.

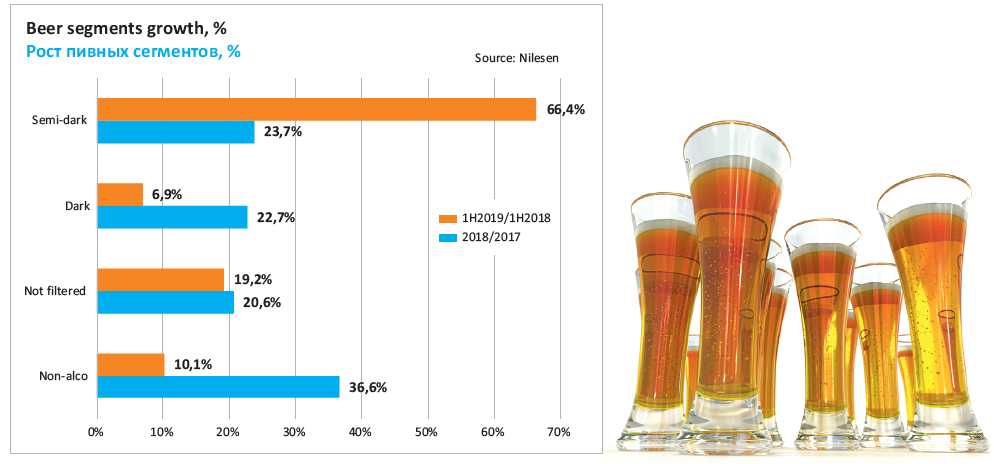

Marginal sorts have grown due to widening tastes that led to further rapid volume growth of special and alcohol-free beer. …, … and even many regional brewers made the major contribution in this process. Thus, in the first half of 2019 according to Nielsen by volume the sales of unfiltered beer increased by ….%, dark and semi-dark beer sales grew by … and ….% respectively. Non-alcoholic beer sales increased by ….%.

By the time of the article preparation, operational data by Rosstat for the first three quarters of 2019 are available, and still can be changed. High calculation base of 2018 when there was the World football championship, warmed with hot weather and exerted a pronouncedly negative effect on the trade balance in the third quarter (-.%). Yet if we estimate the dynamics for . months of 2019, the trade balance remained at the same level. Probably, by the end of 2019, the market dynamics will be close to zero or slightly positive due to import beer.

Positions of brewing companies

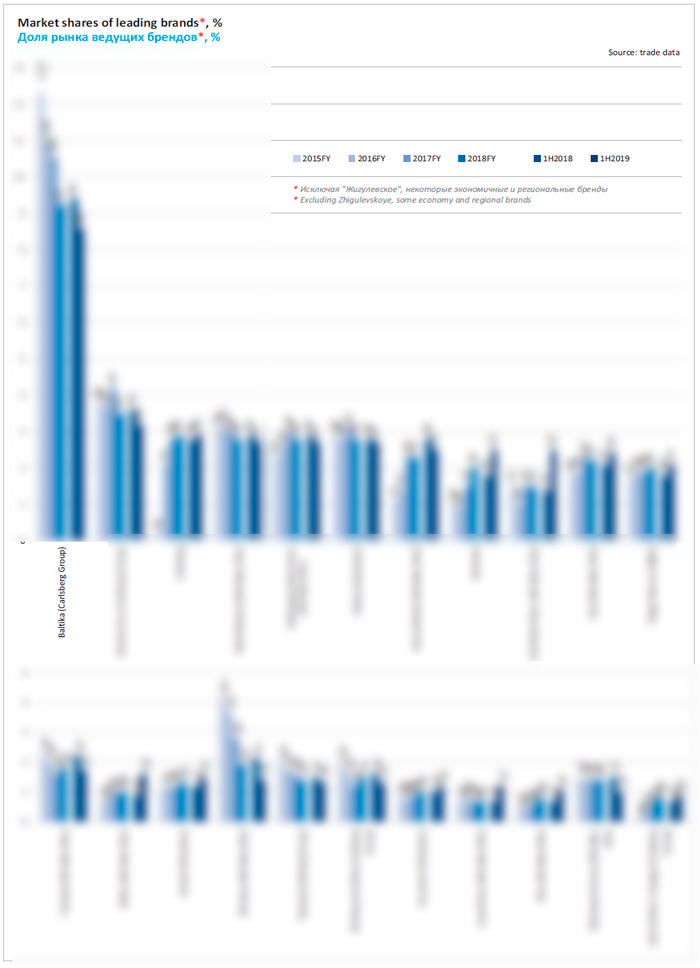

Baltika, Carlsberg Group

In 2018, under our estimation the volume of Baltika sales increased by .% and reached … mln dal of beer. The official revenues amounted to …… bln RUB (+…%) and before-tax profit equaled …… bln RUB (-…%).

In 2018, under our estimation the volume of Baltika sales increased by .% and reached … mln dal of beer. The official revenues amounted to …… bln RUB (+…%) and before-tax profit equaled …… bln RUB (-…%).

In the first half of 2019, Carlsberg Group experienced further sagging of its market positions. Against small growth the industry, the company reported a .% sales decrease. The negative dynamics is confirmed by lower volumes of output. Judging by RAR statistics in the six regions where Baltika is the absolute leader, the beer production shrank by .% in the first half of 2019.

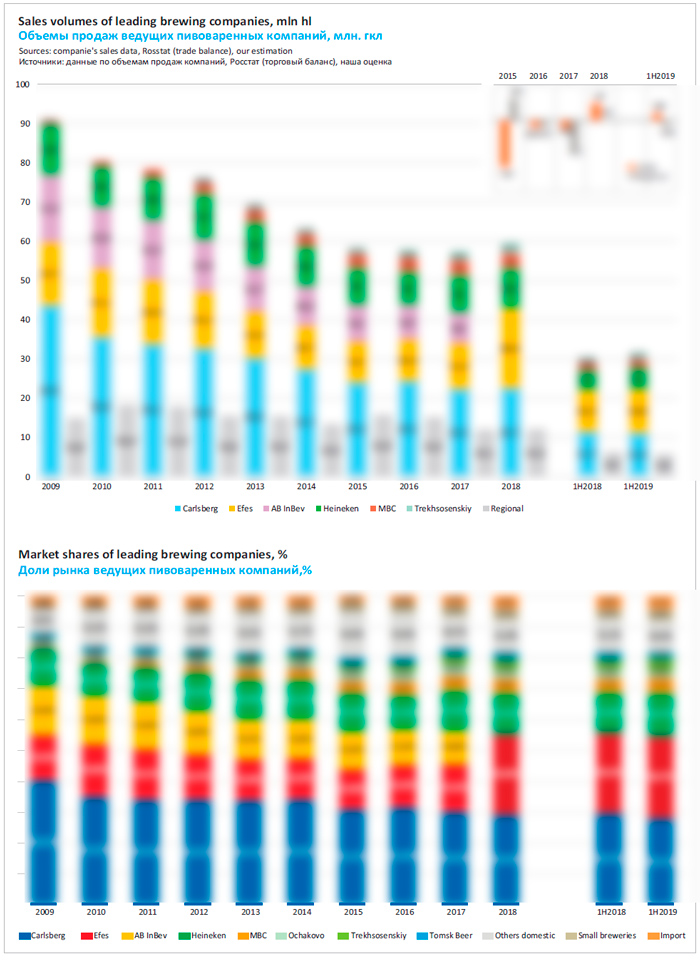

Under our estimation, the market share of Baltika decreased in the first half year by … p.p. to ….%. After merging of the two competitors, the company is ahead of others with a small distance (… p.p.). Thus, provided the existing trends stay in the nearest future, Baltika can yield its first place to AB InBev Efes.

Another cycle of Carlsberg Group market share decline started in October 2018. As almost all fluctuations on the Russian beer market, the negative changes resulted from price competition. In 2018 the company managed to secure its market share by sliding the sales structure towards cheapening, but an effort to improve profitability led to fall in sales volume and market share.

In particular, prices for economy brands Zhigulevskoe, Arsenalnoe, Bolshaya Kruzhka were decreasing which meant a fast growth of their market share. At the same time, striving to improve the price mix the company raised the price for …., … and to a smaller extent but still notably for …. As a result, big mainstream brands experienced a decline of their market weight and the decrease of the market share in 2018 was their “contribution”.

But next came re-balancing of volumes in order to improve the sales profitability. The company did not try to keep the prices for economy brands which resulted in further decline of the market share in the first half of 2019. However, this was happening against comparatively high base of the first half of 2018.

Commenting on the sales volume fall, Carlsberg Group spoke of fiercer competition on the Russian market. While in 2018, average prices for Carlsberg Group products were …% higher than the market average, in the first half of 2019, they were ….% higher (according to the company itself, referring to Nielsen).

At that, the company is again declaring the principle of “the golden triangle”, as improving of the price mix offsets the decline of natural volumes. Mix was improved by erasing economy sorts along with focusing on premium sorts. In the first place these are international brands such as: …, …, … and ….

Big attention is currently paid to rapidly growing niche segments. In the first half of 2019, there was a further popularity growth of non-alcohol original beer …. Besides the company launched a range of novelties, such as red semi-dark lager …, unfiltered sort of Scandinavian subbrand Carlsberg Wild Unfiltered and a cherry sort in Seth & Riley’s Garage range. In May Baltika started producing two types of natural malt drink Barley Bros without additive sugars, sweeteners and preservatives.

As in the first half of 2019, Baltika’s dynamics was negatively impacted by the previous year base effect, the final performance of 2019 can look better than the current one. But in general, the cycle of securing the market share by price and subsequent decline of the market share due to efforts to improve the profitability reminds the situation of past years. It transforms into long-term trend of sequential decrease in shares of big and economy brands and, accordingly, gradual deterioration of Baltika’s market positions.

AB InBev Efes

Historically, integration processes in the course of two companies’ merging as a rule resulted in the decline in the market share belonging to the joined company, which went on several years. However, after merging of AB InBev and Efes in Russia (that took place on 31 March, 2018) their share on the contrary, started growing.

In 2018, under our estimation, the sales volume of the joined company hit … mln dal of beer (growth totaling …%). By the end of the first half year of 2019, the company reported of a growth in sales volume exceeding the market by several times*. Under our rough estimation based on statistics data in the regions where AB InBev Efes dominated, the company’s output volumes grew by nearly .%.

* According to AB InBev Efes estimation, referring to data by Rosstat in the first half of 2019 the growth of beer and beer drinks output amounted to nearly 1% versus the same period in the previous year.

Amid the outrunning growth, the market share of AB InBev Efes got … p.p. up to ….%. Apparently, the joined company managed to overcome the negative dynamics of 2015-2016 and to fight back its market share from regional producers and Carlsberg Group.

If, despite the merge, we look at AB InBev and Efes brands separately, we will see that they continued developing in the same direction, both in 2018 and the first half of 2019.

The volume growth of … brands that previously belonged to Efes resulted from aggressive price policy of the company, that priced regional brewers and the market leader out of the market.

Yet, at the same time, there was brand structure … among former AB InBev brands, that is, the market share of inexpensive brands was blurred and premium brands were gaining weight. That would have resulted in further AB InBev sales decline, but the joined company raised its market share due to bigger Efes weight.

Thus, via sharp price cuts for …, its market share hiked in 2018/2019 and by the end of the first half of 2019, the growth amounted to …. p.p. The brand “…” that had been previously presented in Krasnoe&Beloe chain in draft format, disappeared from shelves. But instead, at the beginning of the sales season 2018 cheaper … was launched that is also packed in kegs and sold in chain Krasnoe&Beloe which together provided for the rapid sales growth. By the end of 2018, the market share of … increased from zero to nearly .% of the market and by the end of the first half of 2019, its market share growth amounted to …. p.p. At the same time, … and … brands made up for decrease of … market share.

Under our estimation in the first half of 2019, the market share of the license segment … went few tenths percentage points down. Yet that was fully offset by growth of several other international brands. In particular through substantial expansion of distribution and notable price decrease, the market share of … grew by …. p.p. Besides, according to the reports by the company in the first half of 2019, there was a share extension of … (+…. p.p.) and … (+…. p.p.). By the year end, the market shares of these brands can grow even more due to low base effect of the second half of 2018 when there was no development. Besides the company went on expanding the range of expensive import sorts and launched Leffe Ruby, Leffe Ambree and Spanish beer La Virgen.

In the mid-price segment by the end of the first half of 2019, there was a prolonged market share decline of …, that however, does not have a big impact on the company volumes any more. Like other brands with youth positioning, its sales suffer from the target audience shrinkage, ever stringer beer market polarization and general falloff interest to old national brands amid the growing range.

As we can see, the sales structure of the joined company is growing ever more polarized as AB InBev Efes does not wish to yield its positions in the economy segment, weakly develops in the mainstream segment and puts a lot of efforts in order to expand the market share in the license segment. And the price affordability of license brands is growing.

AB InBev Efes took a market share in the economy segment not only from the market leader but also from many regional brewers. Here expansion of cooperation with major federal chain of alcomarkets Krasnoe&Beloe became an important factor. While in 2018 as far as we know one could find at shops only several brands by the company, currently there is a wide range of the joined company’s packed beer sorts. The growth of numerical distribution and comparatively low price for the production on the shelves of alcodiscounters definitely have had a positive effect on sales volumes of AB InBev Efes.

Heineken

The Russian subdivision of Heineken continues outpacing other international companies. Basing on regional statistics one can speak of a nearly .% sales growth in the first half of 2019. Heineken’s market share in Russia also gained maximal … p.p. to ….%.

The Russian subdivision of Heineken continues outpacing other international companies. Basing on regional statistics one can speak of a nearly .% sales growth in the first half of 2019. Heineken’s market share in Russia also gained maximal … p.p. to ….%.

In 2018 the company’s sales volume amounted to … mln dal with an .% growth under our estimation. Thus, one can speak of confirmation of long-term upward trend of Heineken positions in Russia.

According to the company’s reports, over the first half of 2019, in Russia there was a .-.% volume growth … thanks to the development of premium part of the brands portfolio where … is the leading one as well as due to new license Miller Genuine Draft and Staropramen brands. In the company’s plans there was an output increase at breweries in Nizhniy Novgorod and Yekaterinburg due to production launch of these brands.

By the beginning of 2019, the market share of Miller was nearly …% of the packed beer market which is nearly three times higher than in 2014. At the same time Miller remained the most marginal sorts in the premium segment. Staropramen’s market share dynamics was the opposite as it shrank by several times over five years and equaled tenth parts of percent. Yet, if we sum up the shares of two brands, their rapid transfer by itself could provide for rapid growth of output of Russian Heineken subdivision.

Non-alcohol category has become the second growth driver for Heineken in the premium segment. In 2017 the company launched non-alcohol sort of flagman brand (…), that due to unprecedented advertisement, promotion in HoReCa and numerical distribution gained a substantial market weight. Then the company relaunched the alcohol-free Amstel brand. In May 2019, it was announced of launching Amstel … Natur (alcohol-free beer drink with juice) and alcohol-free dark beer Krusovice. Besides, Heineken within the project “point zero” it is planned to install a specially designed equipment (including fridges) at .. … Russian outlets in order to attract attention to their alcohol-free products.

“We are currently number two (at the market of alcohol-free beer in Russia), our ambition is to lead the market in the future. We think that there are two factors that will help us. The first one is brewing technologies, that are very important in this segment, the second one is marketing technologies in creating premium brands”- said Baudenwein Haarsma, general director of Heineken Russia.

Such activity led to necessity to increase the productive capacity. During 2019-…. Heineken plans to invest more than … bln RUB into development of their biggest production site, Volga brewery in Nizhniy Novgorod. Putting equipment for non-alcoholic beer Heineken … production into operation at Volga brewery is a stage of general investment plan including expansion of production capacities, extension of warehouses and new can filling line launching.

Under our estimation, in the first half of 2019 a mighty sales growth of international license brands was coupled with a decrease in volumes of the company’s Russian brands at the market of packed beer. This took place mainly because of pressure from AB InBev Efes. Thus, like in the situation with Carlsberg Group the competitive situation and the company’s activity caused weight growth of the premium part of Russian Heineken’s portfolio. The difference is only the fact that Heineken’s … brands compensated for the decline of … brands. Besides, the sales of the company’s economy brands have been probably stable.

By the time of the article preparation, there has been Heineken’s report published for the third quarter of 2019. It says that the sales volume in Russia decreased by .-.% which can be explained by cold summer and high comparative base due to World football championship last year. However, such decline in general looks not worse than the average for the industry.

Other companies

The sales dynamics of independent brewing companies varied greatly. The upward trend of Zavod Trekhsosenskiy preserved and MBC improved its positions. Basing on the regional data, we can say that small and craft breweries expanded their output. At the same time, Ochakovo and most of mid-size regional brewers lost a substantial part of output volume and market share.

Judging by the regional statistics data, Moscow brewing company (MBC) raised its output volume notably in the first half of 2019. Cooperation with biggest federal chain of alcomarkets Krasnoe&Beloe was perhaps the key growth factor. Thus MBC managed to expand distribution in regions and compensate for some market share reduction at the domestic market in Moscow. Another key factor, namely steady marketing activity and launches in different segments of beer market, including rejuvenating of import portfolio.

Under our rather rough estimation, in the first half of 2019, production growth of beer by MBC hit nearly ..%, and the market share increased by … p.p. to …%.

In 2018 under or rough estimation, MBC output volumes amounted to about .. mln dal (+.%), the official revenue equaled …. bln RUB (+….%), and before-taxes profit was … mln RUB (versus … mln RUB loss in 2017).

Zavod Trekhsosenskiy in the first half of 2019, went on increasing sales volumes and the market share, basing on the data of regional statistics. Under our rather rough estimation, the output volumes of the company hiked by . p.p. and exceeded .%, Apparently, the sales growth of the company is still connected to the price competition and cooperation with Krasnoe&Beloe. Zavod Trekhsosenskiy is still the major supplier of both draft and packed beer.

The output volumes of Zavod Trekhsosenskiy in 2018 ran at nearly .. mln dal (+..%). The official revenue rose by .% to …. bln and profit before taxes fell threefold, to … mln RUB.

The period of restoring market positions finished for Ochakovo in 2018 as the company started again losing the output volumes.

Under our rough estimation, based on regional data, in the first half of 2019, the company’s output decreased by ..%, and the market share fell by . p.p., to .%.

Ochakovo’s output volumes in 2018 fell by ..%, roughly to .. mln dal. Due to diversified production and the portfolio premiumization, the official revenue remained approximately at the same level, that is, …. bln RUB, and before-taxes profits soared from .. to … mln RUB.

Despite Ochakovo’s reinforced market and branding activity in the recent years, it is still highly dependent on competitive situation in the economy segment (that is deteriorating) and on sales in the traditional trade channel (which is also shrinking rapidly). In this situation authorities of some regions where Ochakovo is present introduced tax advantages to support brewing businesses. And in Tyumen the advantages were introduced “due to threat of reduction of branch structure of Ochakovo”.

Despite the wide geography of sales, Ochakovo’s problems are to a large extent the same as regional brewers with Russian capital have.

The fundamental reason for regionals’ ups-and-downs is focusing on: .) older audience who keep high loyalty for beer, .) economy nostalgic and “geographic” brands such as Zhigulevskoe, Yachmenniy kolos, Nemetskoe, Cheshskoe and so on that belong to none. .) special outlets, that is, DIOT segment and traditional retail.

In 2015-2018 transnational companies in order to keep the volumes started to actively developing competitive fields of regionals and won initiative from them, as prior to that the only actual drag on leaders’ development was unwillingness to change the marketing strategy, decrease the margin and refrain from promoting local brands of their own.

The difference between recent years and 2019 is that in the past the major competitive pressure on Ochakovo and regional breweries was exerted by Baltika and Zavod Trekhsosenskiy, but currently their market share is mostly being won by AB InBev Efes. At the same time the leaders went on expanding to other rapidly growing niches (import, non-alcoholic and special beer) as well as retail trade channels (supermarkets).

Besides, the chains are experiencing a rapid growth of private labels, that are usually quite affordable. According to Nielsen data, the year June 2018 – May 2019 against the same period previous year, private labels sales grew by ….% by money and ….% by volume. Some independent brewers produce beer under a contract with supermarkets, yet shifting of focus from own brands but minimal marginality affects the business development.

All this caused stagnation of mid sized regional breweries and in the recent years there has also been a reduction in the output volumes. Such reductions have been usually followed by diversification and entering other product categories – from craft beer sorts to energetic drinks.

For instance, the Siberia independent brewers have also decreased their beer output. This region is a kind of indicator as there are located a lot of producers with Russian capital. One could have spoken of weather factor or other natural factors but AB InBev Efes has substantially raised the output at their big brewery in Omsk (by nearly ..%), while the general beer output in the Siberia also has grown a little.

In 2018 there was a nearly …% production growth to …. mln dal at the biggest regional independent brewer of Russia, company Tomskoe pivo. However, in the first half of 2019 the output went nearly .% down under our estimation.

The official revenue, according to the company report in 2018 reached ….. bln RUB (+…%), while the before-taxes profit amounted to ….. bln RUB (+….%).

In the yearly report of the company there were also analyzed changes of the competitive situation that impacted the sales volumes of most of regional producers. Let us cite that part of the text uncut.

In the aggregate, in the first half of 2019, the brewers’ output of Altai Krai fell by 5%. For instance, by our estimation, beer output by Barnaulskiy Pivovarenniy Zavod fell by several per cent (in 2018 its revenue grew by …% to ….. bln RUB).

Company Ayan located in Khakasiya Republic, in 2018 reduced its beer output by …% to … mln dal. The company still focuses on packed beer production (…% of the total volume) and sells most of it in the domestic region and Krasnoyarskiy Kray (…% of the total volume).

Sales revenues declined by …% to … bln RUB, and the net profit fell by …% to … mln RUB due to higher cost price.

Under our estimation, based on regional data, in the first half of 2019, the beer production went on declining at approximately the same rates.

In the yearly report by Ayan it was said about the necessity to lead reasonable price policy because of the negative trend of counterfeit production market share growth. Raising in producer’s prices only compensated for the lost volumes.

The situation in other Russian regions looked not better than in the Siberia. The majority of independent brewers reduced their production amid minor market growth. Let us speak of the major ones.

Under our estimation, based on regional statistical data, Ryazan brewery Khmeleff reduced its output a little (-.%). This company stakes on keg beer and specialized beer outlets. The key sales directions are the domestic market and geographically close market of Moscow. Its revenues in 2018 amounted to ….. bln RUB (+…%), and before-taxes profits reached … mln RUB (+….%).

Output volumes were also cut at Buket-Chuvashii-Bulgarpivo that has production sites in Cheboksary (Chuvash Republic) and Naberezhnye Chelny (Republic Tatarstan). In the first half of 2019, the holding manufactured about … mln dal of beer under our estimation (…+… mln dal), which is nearly .% lower than the level of the previous year. The both breweries have by now organized alcohol-free beer output and are expanding their ranges by special sorts. For instance, ales and alcohol-free beer have been showing a rapid growth amid reduction of the general beer category of Bulgarpivo, according to the company’s press releases. Besides, in the general sales volume of drinks by the holding the share of kvass and cyder increased.

For reference, in 2018 the revenues of company Buket Chuvashii rose by …% to ….. bln RUB and the profit grew twofold, to .. mln RUB. The same year the revenue of Bulgarpivo fell by …% to ….. bln RUB and before-taxes profits reached .. mln RUB changed nearly the same loss.

Deka company in Velikiy Novgorod dropped its production volume sharply. If we base on the regional data, one can also assume that beer output in 2019 was partially or fully stopped. Because of problems with creditors and owners Deka experienced administrative receivership and long-lasting court processes that limit the operational activity.

Though Deka is known as a kvass producer, and beer is not a major category for the company, it used to be a big supplier of private labels for trade chains and output nearly . mln dal of beer per year. Currently this niche is occupied by other producers.

One of few exceptions in the row of “sagged” independent businesses is Beliy Kreml brewery. But, for one thing, the brewery only started operating last year and is currently approaching the full capacity. For another thing it belongs to big alcohol holding Tatspirtprom that has ambitions beyond the region boarders.

Over the first half of 2019, Beliy Kreml shipped … mln dal of beer. Out of the total volume, ..% of supplies accrues to packed beer and the rest to draft beer. About a quarter of beer was sold in Tatarstan, and the rest was delivered to .. regions of Russia. The expansion is based on close cooperation of Beliy Kreml with regional and federal chains. The company’s partners are Ashan, Tander (Magnit), X5 Retail Group (Pyaterochka), Bristol and Krasnoe & Beloe.

To get the full article “Russia: Positions of Brewing Companies in pdf (18 pages, 12 diagrams) propose you to buy it ($20) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.

The article is prepared using the data by Rosstat, Federal Service of Alcohol Market Regulation, «Catalogue of Russian Beer Producers 2018», presentations and reports by brewing and research companies. At the article preparation publications in editions Kommersant, Sostav.ru and Vedomosti were used.

The data on output volumes and their interpretation are our assessments based on the regional statistics and current trends in case the source has not been named. We do not claim the given information to be absolutely correct, though it is based on data obtained from reliable sources. The article content should not be fully relied on to the prejudice of your own analysis.