The beer market dynamics in Russia is approaching zero, yet major brewers are divided into those who developed considerably in 2017 and those who considerably reduced their volumes. For instance, company Efes has managed to substantially extend their sales due to restrained pricing policy and activity in the modern trade. Heineken has also demonstrated an excellent performance promoted by significant increase of advertisement budgets launching a non-alcohol sort of the title brand and unusual activity in the economy market segment. Carlsberg and AB InBev have been focusing on margins and lost a market share of their inexpensive brands. Serious dependence on PET package and mass enthusiasm about Zhigulevskoe have negatively impacted the most of big regional brewers, that have been for the first time pressed by the leaders in the key sales channels, especially in Volga and Central regions. In the small business there has been a noticeable slowdown in appearing of new restaurant breweries, yet the number of craft breweries has been growing rapidly. In 2018, the beer market is likely to grow a little, while the share of AB InBev Efes may decrease due to the integration.

The year performance – assessments slightly differ

Performance of companies

Federals broke even

• Carlsberg Group

• Efes

• Heineken

• AB InBev

Regionals went into the red

Small brewers: craft is in trend, restaurants are out

Outlooks for 2018…

The year performance – assessments slightly differ

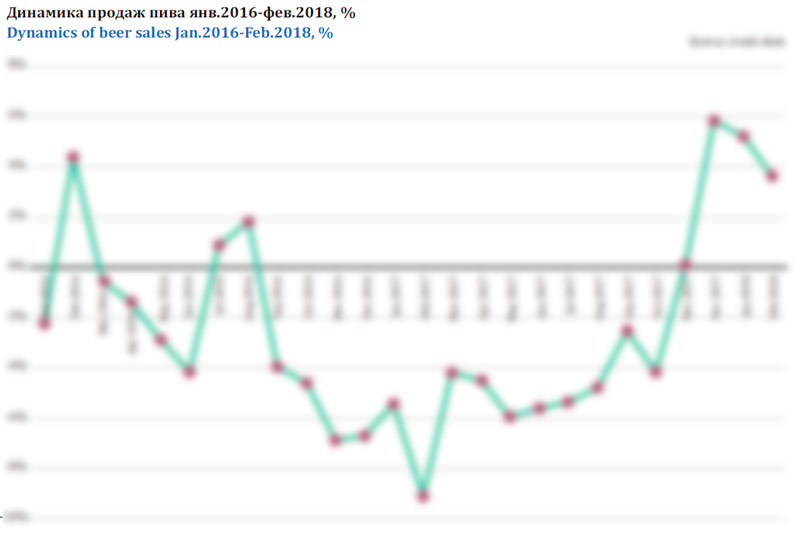

In the end-of-year press release “Industrial production in 2017” Rosstat reported that production decreased by 2.4%, to 744 million dal. At the same time, according to the Federal service for Alcohol Regulation (Rosalkogolregulirovanie/RAR) 760.7 million dal of beer was produced in 2017, which is 1.3% less than in 2016 (770.6 million dal). Perhaps these figures are higher than Rosstat data because RAR statistics includes registered manufacturers of all business scales, and administrative requirements here are much harsher. This is clearly seen when comparing the data for 2016 in the regions where you can only find small producers.

On the basis of data on production, imports, exports, and carryover stocks estimates it can be calculated that the volume of the Russian beer market (as a result of the trade balance) has declined in 2017 by 0.9% to about 757 million dal. In 2017 the market dynamics looks better than production, as 19% less Russian beer was exported and imports conversely grew by 26%. The effect of carryover stocks was neutral or slightly negative, because since the new 2018 year excise tax has not increased and for brewers it was impractical to overstock warehouses of distributors.

Thus, according to the RAR data the reduction was very small and on the basis of official data, it is possible to speak about stabilization of beer production after a period of prolonged and rapid decline in the period of 2008-2014. If official figures are correct, then stabilization took place despite the negative impact of the prohibition on large volume PET packaging.

However, estimates that look much worse than the official statistics are that of Nielsen Russia (according to publications of market participants). According to retail audit, the beer market in 2017 decreased by 4.7% contrary to expectations of positive dynamics of 3-5%. Market audit does not fully cover all the channels of beer sales (excluding HoReCa and part of specialized stores), but adequately reflects retail sales, where the negative impact of limiting the size of PET packaging manifested itself fully.

Note that the dynamics of retail sales were negative for a very long time – from autumn of 2016 to October 2017. And if at the beginning of 2017, the rate was sharply negative, by the summer, the situation was already not looking so bad. Probably the high season would have been better, if not for the bad weather, which many brewers complained of. The results of the fourth quarter of 2017 were quite positive. Naturally, this improvement arose from the low base effect of the end of 2016, when the new restrictions were fully apparent.

Performance of companies

Federals broke even

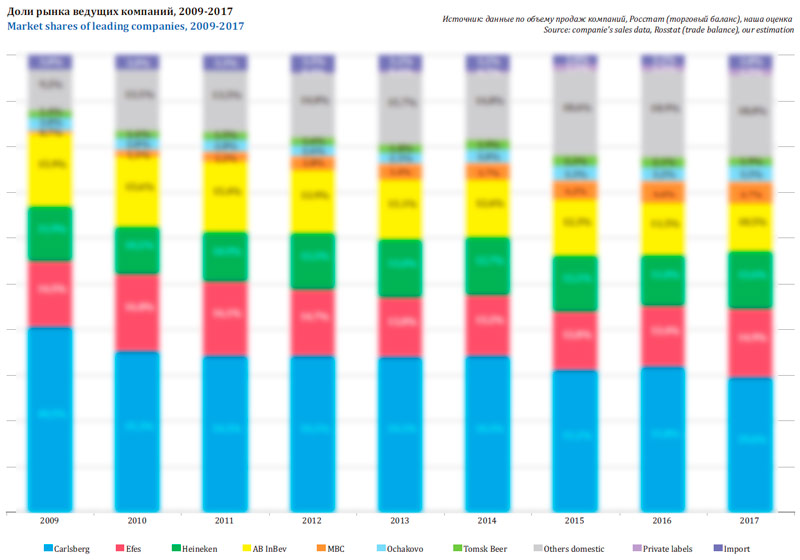

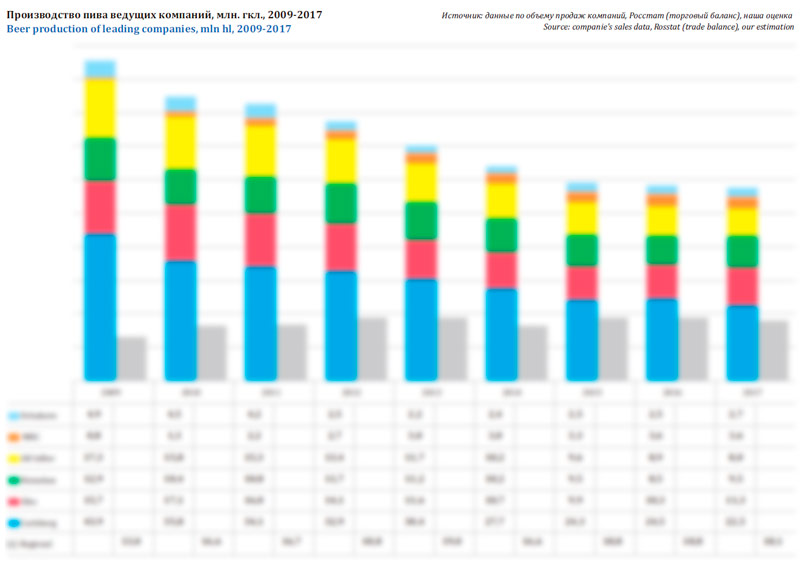

After a dramatic collapse in 2010 and further decline continuing up to 2015, the aggregate sales volumes of the leading six companies with a national distribution level reached a stable rate. Their net market share has remained at the level of 76% and the output volumes have been about 58 mln hl. The last years’ recession resulted from a reduction of beer consumption. Yet the market leaders were also much affected by competition with medium sized regional breweries.

By the end of 2017, for the first time in a long period, one can say that major companies were successful not only in interspecific competition, but in trying to take a share of regional players too. Though such results were caused by several serious trends, one so far can consider it a temporal deviation from the balance. The problems of Efes and AB InBev integration can change the situation back in the favor of independent regional players.

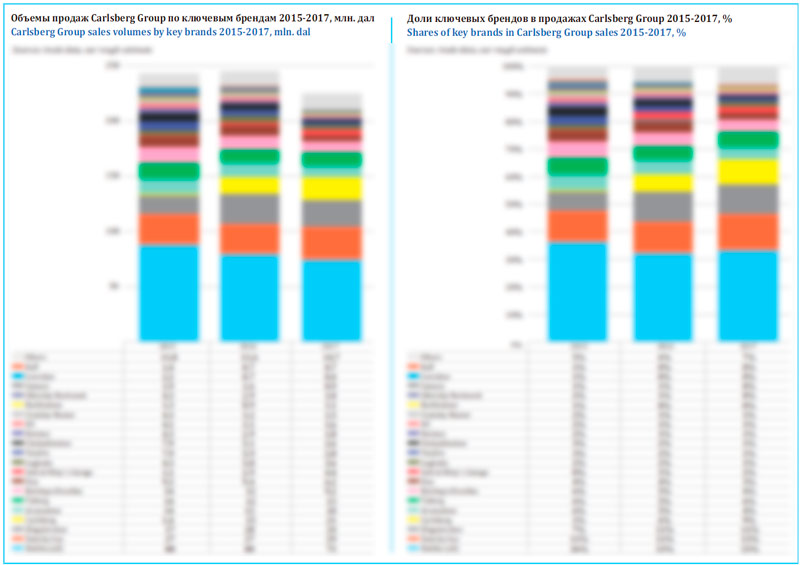

Carlsberg Group

In 2017 Carlsberg Group reported a 8% decrease in sales. About the same decline of about …% show calculations based on regional statistics of beer production (in 2016 there was an increase of …%). Such dynamics looks significantly worse than the two nearest competitors. The market share of Carlsberg Group, according to our estimates, declined by … p.p. to …% (after stabilization in 2016).

Tellingly, the company’s sales were not taken away by regional manufacturers, as it happened in 2008, but by other international groups.

In Baltika’s press release the reasons for the decline are explained by changes in the marketing strategy of the company:

“The sales volumes and market share were significantly affected by the limitation on PET volumes. For adaptation to major changes that have occurred in the market, Baltika adjusted its pricing policy to market growth in terms of value. Some competitors have chosen a strategy aimed at increasing volumes. As a consequence, the price for production of Baltika in PET packaging was above average in this segment, which caused a decline in the market share of the company. However, the approach of Baltika to increase the market share in value terms has led to an increase in profits.”

But the company managed to strengthen the margin portion of their portfolio. According to the full year press release, the positive dynamics in 2017 was shown by some of the key brands in premium and mainstream segments – Carlsberg (growth of the brand’s market share by 0.8 p.p.), Zatecky Gus (growth of the brand’s market share by 0.6 p.p.), Flash Up energy drink (growth of the brand’s market share by 0.6 p.p.), Baltika #3 (growth of the brand’s market share by 0.3 p.p.), Seth&Rileys Garage (growth of the brand’s market share by 0.2 p.p.), and Tuborg (growth of the brand’s market share by 0.1 p.p.).

According to our estimates, Baltika’s title brand continued to cut sales, although not as fast as a year earlier (which already looks good). The market share of Baltika beer decreased by … p.p. but the umbrella brand is still the absolute leader of the Russian market.

In our opinion, the main reason for the reduction in the company’s market share can be explained by stiff price policy. The average retail prices for Carlsberg Group’s beer rose …. And then the company kept them at the same level over the high season. However, two biggest competitors Efes and Heineken at that time on the contrary kept average prices down and won sales of Carlsberg Group.

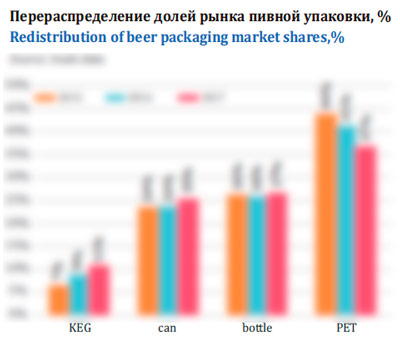

The decline was to a significant extent caused by the branding policy concerning “old” regional brands in PET. This trend is clearly visible in the period from 2015, when the prospect of a ban of large PET volumes did not yet affect the market, till the beginning of 2018, when the ban was fully introduced. During this time, the largest regional beer brands have dramatically decreased their share on the packed beer market, namely Don (…), Yarpivo (…), Chelyabinsk (…), DV (…), Uralskiy Master (…), Sibirskiy Bochonok (…) and Samara (…). By the end of 2017, a rather large Ural brand Legenda, which was bottled at Pikra and occupied nearly …% of the market of packed beer, virtually disappeared from the shelves.

While in the economy segment of packed beer focus has shifted to the well-known federal brands, as well as some new items. In particular, although …, …, … felt the impact of the ban, nevertheless still occupy a larger market share.

According to our calculation, in 2017 these economy federal and regional brands lost about … p.p. on the packed beer market.

By 2018 the share of regional brands will likely shrink even more if the company does not revise its pricing or if its competitors don’t revise it either. And vise versa, the federal economy brands have started growing due to their revised price policy.

According to the press-release, by the end of the first quarter of 2018, the positive dynamics was demonstrated by the following brands: Arsenalnoye (growth of the brand’s share by 0.3 p.p.), Rizhskoye Firmennoye (growth of the brand’s share by 0.1 p.p.), Bolshaya Kruzhka (growth of the brand’s share by 0.8 p.p.), and Zhigulevskoe (growth of the brand’s share by 0.9 p.p.).

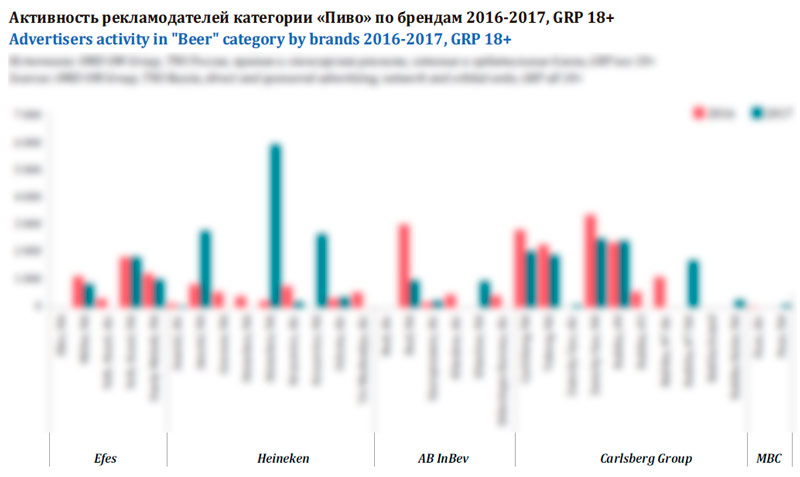

According to OMD OM Group data, in 2017 the company cut their advertising activity by …%. GRP* were approximately equally divided between brands Zatecky Gus, Carlsberg, Tuborg, Baltika #0, and Baltika #7, which reveals the company’s further focusing on marginal brands.

* Shows how many times an advertisement is seen by people over a campaign.

From the regional perspective the production and sales of the company have developed very unevenly.

Shutdown of two breweries in 2015 and subsequent gradual loss of market share of regional brands is naturally reflected in the geography of sales of Baltika during 2016-2017. In particular, the termination of Pikra in Krasnoyarsk and withdrawal from the market of brand … has led to a significant decline in sales and the share of Baltika in the market of Eastern Siberia. A similar situation is observed in the Urals in connection with the closing of Baltika-Chelyabinsk brewery and a sharp drop in shares of brands … and ….

Also perceptible decline occurred in 2017 in the markets of Moscow and St. Petersburg. According to our estimates, there was a decrease of the share of mass brands …, … and …. But in contrast to regional markets, this reduction was largely compensated by the growth of … sales.

Let us recall that in late 2015, the brand migrated from premium to mid-price segment, when its retail value dropped by about …%. As a result of the synergy of a sharp rise in availability, premium image and active advertising of non-alcoholic varieties, Carlsberg beer developed a powerful growth momentum. In 2016-2017, the brand gained significant market weight in Russia and finished in seventh place by sales volume with a share of about …%. But especially noticeable was Carlsberg’s success in the major cities. In particular, in the market of St. Petersburg its share in 2017 exceeded …%, and on Moscow market it was more than …%.

In the cities of the Central region, excluding Moscow, in the Southern and Volga regions, the company has slightly improved its position, but it was not enough to realign the overall negative trend. Perhaps this improvement was associated with expansion in a growing segment of the DIOT (Draft in Off-Trade).

Thus, according to the company, citing data from Nielsen, at the end of 2017 DIOT share made up 10.5% of the total beer market, showing an increase of 2 p.p. against 2016. In response to the segment growth Baltika Breweries has installed PET-keg packaging lines at the breweries in Rostov-on-Don and Novosibirsk and invested of about 417 million rubles in the projects. As a result company dominates DIOT with a market share of 20.4%, and at the end of 2017, the company increased its volume share by 5.3 p.p.

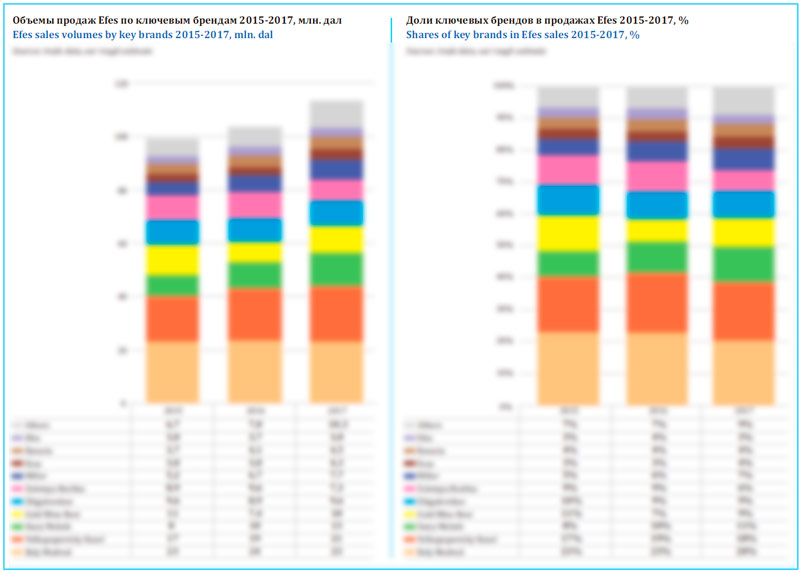

Efes

The Russian subsidiary of Efes in 2015 continues to increase sales and strengthen its position in the beer market. According to our estimate based on company reports, in 2017, sales of Efes increased by …%, up to about … million dal (in 2016, the growth was …%). The market share of Efes increased by … p.p. and by the end of 2017 was …%.

Regional statistics of beer production reflects double-digit growth in Kaluga oblast (…%), Ulyanovsk oblast (…%) and in the Republic of Bashkortostan (…%), dominated by Efes.

According to Efes report for 2017, Russia performed exceptionally well by recording double digit sales growth, despite a very strong base of the previous year. Such performance was driven by increased penetration in the modern trade channel, as well as market share gains in premium and upper mainstream segments.

The company, like a year ago announced its leadership in the premium segment.

As for the price competition, the market share growth of Efes resulted from the prices rising in phase opposition to other market players – during the … they were at the lowest level. That is, the high volumes were provided by smaller profit from each sold hectoliter.

According to our estimates, in 2017 the majority of key brands by Efes increased their market share.

In the economy segment of the market some weight was gained by the brand …, which remains the largest in the company’s portfolio. … after the decline in 2016 almost regained their positions. … also retook lost positions, but its share has not changed much.

In general, fluctuations in the market share of cheap brands have largely been associated with the introduction of restrictions on the sale of beer in large volume PET and the subsequent adaptation. The problem was more relevant for the brand Gold Mine Beer, which is primarily bottled in PET containers larger than 2 liters and less — for beer Beliy Medved, which also gravitated to larger formats, but was better represented in glass and PET bottles of 1.5 liters or less.

However, the greatest contribution to the growth of market shares of Efes was has been made by marginal rather than economy brands. Here positive dynamics was achieved due to the synergy of several factors — significant reduction in average retail prices, increasing representation in the networks, advertising and adapting sorts to the market trends of the growing popularity of light and special beer.

In 2017 the company cut their TV ad by …%, and focused it on the key marginal trade marks, namely …, …, and ….

Velkopopovicky Kozel in 2015-2016 was one of the fastest growing brands on the Russian market and after the sharp weight gain, only slightly slowed its growth in 2017. Thereby Velkopopovicky Kozel has strengthened the leading position in the premium segment with a market share of almost 3%. Unlike previous years, in 2017 the development of the brand was not provided by Moscow and Saint Petersburg, (where its share on the contrary has decreased), but by regional markets.

Strengthening of the marginal segment in the Efes portfolio was not only provided by Velkopopovicky Kozel. In 2017 even greater contribution to the brand was made by …, which keeps up high growth rates. Also the market weight was increased by brands …, … and ….

Furthermore, in the space between converging prices for cheaper licensed brands and economy brands, there was Zolotaya Bochka, one of the company’s major brands, which significantly reduced its market share in 2017. Sales of Zolotaya Bochka dropped in … with a comparative sustainability in ….

The development of Efes in the geographical context was uneven. The only problematic region in 2017 was …, where the company has even reduced its presence in the …. And the main positive contribution came from the retail networks of the … and … regions. Moreover, in the … region, the growth was not provided by …, but by other cities. Also the sales of Efes were positively effected by the … region, where the company’s positions are particularly strong.

Heineken

The Russian division of Heineken in 2017 managed to stop the three-year cycle of reducing market share and to reach the level of 2013-2014 again. In our estimate, taking into account the company’s report and regional statistics, sales of Heineken in 2017 increased by approximately …%, to … million dal (in 2016 there was a drop of about …%). Accordingly, the company’s market share jumped by … p.p. to …%, and Heineken settled in the third place in the list of beer sales leaders.

The Russian division of Heineken in 2017 managed to stop the three-year cycle of reducing market share and to reach the level of 2013-2014 again. In our estimate, taking into account the company’s report and regional statistics, sales of Heineken in 2017 increased by approximately …%, to … million dal (in 2016 there was a drop of about …%). Accordingly, the company’s market share jumped by … p.p. to …%, and Heineken settled in the third place in the list of beer sales leaders.

Statistics on the regions where the company dominates reflects a significant increase in production. In Nizhny Novgorod oblast, where the largest Russian branch of Heineken is located, beer production increased by …%. In Irkutsk oblast the production grew by …%. In the Republic of Bashkortostan, where the company is one of the largest manufacturers, volumes increased by …%. However, regional statistics also reflects a downturn in the Sverdlovsk oblast (…%) and Primorsky Krai (…%).

According to the company’s report: “sales volumes of Heineken brands in Russia increased by more than 10%, moreover, in the second half of the year growth accelerated. The increase in sales was mainly contributed by the brands Heineken Lager and Heineken 0.0 and the launch of new products in the economy segment“.

The level of average retail prices for beer by the Russian Heineken subdivision was significantly changing over 2017 and the company’s market share was also fluctuating. Launching new economy brands as well as price controlling led to a considerable reduction of the retail price and a notable growth of sales in …. A short-time price increase in … had an immediate negative effect on the company’s market share, which made it switch to a new cycle of beer price decrease and growth of market share.

In our opinion, in 2017 the Russian division of Heineken was pursuing a multipronged marketing policy for development in different price segments.

In the economy segment of the market, like other large brewing companies, Heineken came under pressure from the ban on large volume PET. And they redistributed sales from the regional to the federal brands as well, but in a special way.

For comparison, Carlsberg Group had this redistribution due to pricing pressure of competitors; obviously the company deliberately went for a sharp decrease of regional brands. At the same time widely known national economy brands, too, have lost a share, but not so noticeably.

At Heineken, the results look different. Of course, the company also felt the pressure on the key economy brand Tri Medvedya and regional brands, but kept their sales from sudden collapse. And most importantly – Heineken had an unusually high marketing activity in the segment, focusing on new economy brands Zhigulevskoe 1978 and Bochkarev Cheshskoe with national distribution, which were rapidly gaining weight.

In particular, the market share of the “old” federal brand … continued to decrease rapidly in 2017. Within two years, it had halved, to …%. Accordingly, the importance of the brand in the Russian Heineken portfolio dropped sharply.

In regional markets in 2017 the share of a major brand Shikhan was significantly reduced, also brands Bereg Baikala, Sedoi Ural, and Amur-Pivo lost some of their weight. In total, their share decreased by about … p.p. and now accounts for about …% of the Russian market.

However, new items compensated for more than … of the reduction in the share of the mentioned above brands. Their launches were pretty “quiet” from the point of view of marketing activity, but that is usual for economy segment.

Note that the name Zhigulevskoe 1978 had already been used by Heineken in 2011, when it released the sub-brand Okhota Zhigulevskoe 1978, but it soon disappeared from the market. This time the company did without an “umbrella” and brought another version of the nostalgic brand in cans and bottles with a classic design for economy beer. The launch took place in the high season 2017 and was accompanied by a viral advertising in separate points of sale – old Zhiguli cars were used as a stand for beer boxes. According to our estimates, the market share of Zhigulevskoe 1978 was about …% in 2017, but the full potential of innovations may manifest itself this season.

Another idea is to combine the well-known image of mainstream brand Bochkarev and the name of the beer, Cheshskoe, which has become very popular with many regional producers working in the market of cheap draft beer. About eight years ago, mass brand Bochkarev has fallen victim to the market polarization and the subsequent unsuccessful attempts at repositioning in the premium segment. In 2014, Bochkarev has virtually disappeared from the market, but now its name was useful for new items that fit into the overall context of the mass migration of Russian federal brands into the economy segment. Cheshskoe ot Bochkarev appeared on the market in early 2017, with virtually no advertising and announcements about the launch. New brand is bottled in PET of 1.35 l. and kegs. According to our estimates, the market share of Cheshskoe ot Bochkarev in 2017 amounted to about …%.

In 2017, after a small pullback the share of the largest company’s brand – beer Okhota – sharply increased by about … p.p. to …%. It overtook Klinskoe, and ranked sixth in the list of national sales leaders. The brand’s popularity can be attributed to the trend of specialization of beer consumption, which main sort Okhota Krepkoe corresponds to. Obviously, in the segmentation on the strength of beer, there is also a slight polarization of the market. In addition, the sales growth of Okhota was promoted by the previously held downsizing and focus on medium volume PET packaging, restrained pricing, and also restyling undertaken at the beginning of the season, with a focus on strength and masculine image of the brand.

Licensed brands, such as Heineken, Goesser, Amstel, Krusovice and others together contributed the most to the sales growth of the Russian division of Heineken. In total their share increased by about … p.p. to …% of the market. So, we can talk about improvement of the product mix in 2017.

The sales increase was to a substantial extent a result of a most powerful TV support. According to OMD OM Group, last year, Russian Heineken subdivision extended advertisement investments, having demonstrated a … times growth and nearly equaled the share of Carlsberg Group.

In 2017 the company’s licensed brands became leaders by GRP number. Basing on data by OMD OM Group, promotional contact of beer Heineken with the auditory was unprecedentedly high as for a monobrand being not lower than all sorts of Baltika. Amstel and Krusovice also took the lead.

The most significant share increase was shown by brand Heineken with their … p.p. growth to …% (in recent years, the market share of the brand stagnated). A key role in this ad support and revival of sales was played by a global launch of non-alcoholic Heineken 0.0 at the beginning of 2017. The appearance of the sub-brand was supported by an integrated ad campaign that includes commercials on television, social media activity, as well as promotion in the sales channels. In Russia Heineken 0.0 was a response to the trend of a growing popularity of non-alcoholic beer and the emergence of a non-alcoholic version of many large competing license brands.

Sales growth of Goesser beer was caused by the same maneuver as Carlsberg beer – migration from premium to mid-price segment while maintaining a premium image. The main weight was gained by Goesser in 2016, but over 2017 its share also increased by … p.p., and today its market share is about …%.

A significant increase in sales of Heineken was observed in most regions of Russia, but especially rapid growth was in the markets of Siberia and St. Petersburg. At the same time, in the Ural region the company’s market share declined significantly due to the decrease in sales of economy brands and regional beer Tri Medvedya.

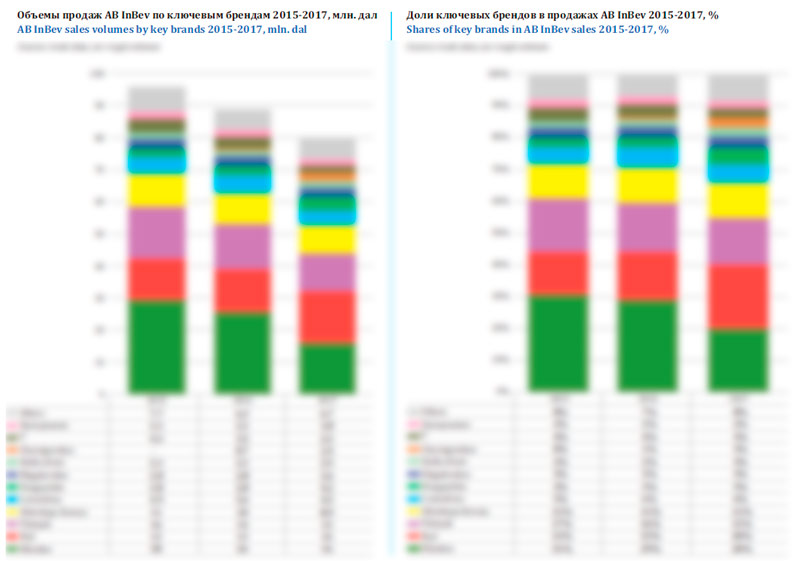

AB InBev

In 2017 sales of Russian AB InBev subdivision continued their protracted and rather intensive decline. According to our assessment, they went approximately …% down to … mln dal. Accordingly, the market share of AB InBev declined by … p.p. to …%.

A considerable decrease in volumes is also shown by data on beer production in the three regions where AB InBev beer dominates. The output decline was registered in Volgograd oblast (…%), in Ivanovo oblast (…%), and in Republic of Mordovia (…%). At the same time the biggest subdivision in Omsk has kept the volumes at approximately the same level, judging by a …% growth of their beer production. In general the regional statistics speak of a low double digit production decline at AB InBev.

Lower figures of sales and market share of AB InBev were transient and connected to the pricing policy of the company. In …, the company together with Carlsberg Group and Heineken started raising prices for their beer. Instead, Efes focused on the volume growth by higher affordability, and soon the average prices for Heineken production started decreasing. Besides, competitors intensified their activity in the modern trade. Yet, AB InBev, following Carlsberg, Group carried out the policy of price rising. As a result, in … (that is, in the …) the company’s positions went down dramatically (as well as the positions of Carlsberg Group), though the average prices continued growing. The market share of AB InBev hit the bottom in …. At last, in … 2017, the company dropped the average prices for beer and the sales recovered very quickly. However, the … slump led to poor final figures. Particularly severe fluctuations and decline of the market share were observed in … and … region.

We can say that AB InBev have continued shifting focus onto the premium part of their portfolio, either purposefully or under the pressure of the competitive situation, judging by the share dynamics of non-marginal brands … and …. Among affordable beer brands, only Zhigulevskoe retained stability.

Basing on the brands dynamics, one can say that the company’s positions in 2017 were drawn down by the abrupt fall of … sales. The brand’s market share immediately decreased by … p.p to …%. The positions deteriorated in all the regions of Russia, yet particularly in the markets of … and …. In our view, the brand’s sales reduction has become an indirect consequence of the ban on big PET packages and stronger competition in the economy market segment of packed beer, where mass sort … drifted in 2015.

Most probably a negative effect was exerted by the company’s pricing policy as well as inflation of the brand image, which was not supported as strongly as previous years. We should note that in Russia the budgets for TV promotion of AB InBev have been cut. According to OMD OM Group data, the GRP number decreased nearly … times. However even launching of … and simultaneous promotional campaign failed to curb the sales fall. Resultantly, … moved from the fourth to the seventh position in the sales leaders’ toplist.

Possibly, the situation will change, and the market share of … will partially recover in 2018 due to decrease of the brand retail prices, which is likely to be positively taken by consumers.

Besides, in the segment of inexpensive beer, one can note a considerable sales growth of … brand, that in 2017 won …% of the market, yet could not compensate the general decline.

Despite weaker support to Bud, it has continued gradually gaining the market weight which is currently more than …%. If the described trends continue, Bud will soon be able to become the major brand in the Russian portfolio of AB InBev.

The majority of other marginal brands by the company have increased their market share a little. For instance brands …, …, …, and … proved to be stable.

Despite the integration, in 2018 some brands of AB InBev (or, rather AB InBev Efes now) can improve their positions due to promotion as the company has become an official official sponsor of the World Football Cup.

Regionals went into the red

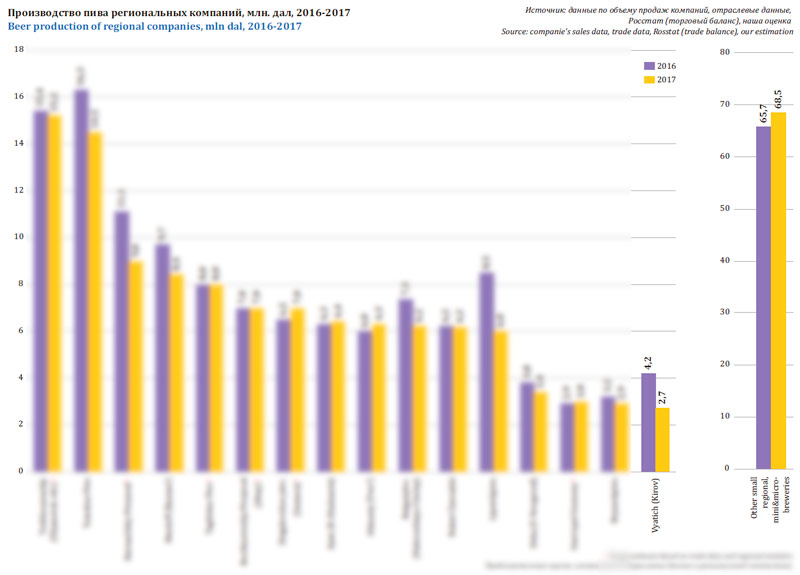

In 2017, the production decline of independent producers was 7%, to 151 million dal, according to our calculations. Despite relatively stable market, this decline meant a decrease by 1.1 p.p. to 19.9%. The weakness of independent producers has become a very important event for the market since for a period of over 10 years (adjusted for crisis of 2014), they had only increased their volumes and taken sales away from transnational groups.

Because of a change in Rosstat publication structure, we cannot exclude the products of mini-breweries from this volume, but their market share is small and it is clear that the decline is fully linked to problems of medium-sized regional manufacturers.

Because of a change in Rosstat publication structure, we cannot exclude the products of mini-breweries from this volume, but their market share is small and it is clear that the decline is fully linked to problems of medium-sized regional manufacturers.

On the one hand, the regionals later than multinational companies reacted to the size limit of PET packaging and even used the transition period at the end of 2016 to temporarily occupy the vacated space. Thus, the current decline can largely be attributed to the high base effect of last year.

On the other hand, independent companies began to feel competitive pressure in the specialty retail from large federal companies.

At the time, regional producers have created a powerful Draft in Off-Trade segment, which for a long time allowed them to grow. Today, however, federal companies out of marketing reasons distance themselves from global image and produce special affordable brands particularly in the category of beer in KEG.

Now the launches in economy segment are “quiet” and often do not add a new sort to the brandlist on the company’s site. Moreover, in order to adjust the producer’s signature on the label to regional images, breweries’ names can even be changed. For example, Rostov subdivision of Baltika has been renamed as “Yuzhanaya Zarya 1974” and the subdivision in Yaroslavl has been renamed as “Yarpivo”.

Once again, in response to “Draft in Off-Trade” beer segment growth Baltika Breweries has installed PET-keg packaging lines at their breweries in Rostov-on-Don and Novosibirsk and invested about 417 million rubles in the projects. As a result company dominates DIOT with a market share of 20.4%, and at the end of 2017, the company increased its volume share by 5.3 p.p. Apparently this growth took place due to the share of medium-sized regional breweries that are currently competing not only with each other.

Another factor of the market share reduction of regional brewers was a fiercer price competition. This driver will become obvious if we compare the average-weighted retail prices for beer of 15 regional breweries and 6 national scale brewers. While the net average prices of the large companies decreased by …% over 2017, there was a …% growth of regional producers’ prices. Or if we calculate the difference between the average prices of the liter of “regional” and “federal” beer, we will see that early in 2017, it was …% and …% at the beginning of 2018. This convergence is too dangerous for regional brewers’ sales, as price is often the main weapon in the competitive struggle in the economy market segment which is mostly their main position.

One should note that the price competition that led to lower volumes of regional brewers, got even fiercer in 2017, particularly in the modern trade. There a considerable price rise for many key regional brewers’ production was observed in the second half of 2017. At the same time, the prices for beer by large producers with national distribution were going down.

The third reason for weaker positions of the regional brewers is linked to reallocation of beer sales between modern and traditional retail channels. The today’s problem of regional brewers is caused by the fact that they are dependent on the traditional sales channel. Their share there is rather high. However, in 2017 grocery stores went on reducing their market weight, and supermarket have again raised their market share.

Judging by the sales fluctuation one can assume that their redistribution in 2017 depended on the seasonal factor. As buying beer for Russians is becoming ever less impulsive (more rational), during the hot season, consumers prefer to buy a big volume of beer at a supermarket rather than pay extra for it at a store. In summer, the economizing by large volumes provided the synergy with lower retail prices for beer by Efes, Heineken launches, long-term price migration of many famous brands, and other events we have discussed in the chapter on the market leaders.

Finally, the fourth reason for the market share reduction of independent breweries is too active launching of beer Zhigulevskoe instead of developing brands of their own. The nostalgic traditional image turned out to be extremely attractive for everyone. Due to the efforts of hundreds of brewers, brand Zhigulevskoe* was gaining popularity till 2016. Under our estimation, in 2017 because of the problems in the economy beer segment, the brand’s market share fell by approximately … p.p. to …%.

* We have not taken into consideration the brands with names derived from “Zhigulevskoe” (such as Zhiguli, Zhigulenok and so on).

Currently Zhigulevskoe can be found in the portfolio of the majority of regional breweries and at each federal scale brewer. However, while in the total sales volume of federal brewers the share of Zhigulevskoe equals nearly …%, regional breweries have at the average a … of all brands with such name.

For brewers the problem of sharing a brand is that despite differences in flavor and design, consumers will easily switch to competitors’ beer in case of price rising. Thus, in “Zhigulevskoe segment”, since 2016 there have been strong fluctuations of companies’ market shares resulting from the ban on large PET packages and further expansion of federal companies to the draft beer market.

Thus, in 2017, major brewers together expanded their share of Zhigulevskoe by approx. … p.p. to …% (Carlsberg Group’s reduction was amply compensated by Efes, Heineken, and AB InBev). Accordingly, regional brewers lost … p.p. because of Zhigulevskoe sales decline, and the brand’s total market share accounted …%. In …, …, and the … regions the breweries experienced the strongest losses.

Let us note that not only Zhigulevskoe brewers faced difficulties. For instance Cheshskoe and Nemetskoe are also popular names used by many regional producers and they got the market leaders interested (above we have described a successful launch of Cheshskoe ot Bochkarev).

How considerable was the general reduction of the market share to regional companies?

At this time, we have no information on termination of large regional breweries with the exception of bankrupt Suzdal brewery Yusberg, where Sberbank is actively looking for a new owner. Also the current owner of the Marksovsky Pivzavod, located in Saratov oblast, wishes to sell the operating brewery (or exchange it for grain). Some regionals have been reorganized and changed the name (for example, … that has got a new name …), but most have kept the old owners and brands.

As for the geography of manufacture, one can say that in 2017, the biggest negative impact was made by medium sized breweries in the European part of Russia from Saint Petersburg to Volga region. The Urals and Siberia regional breweries cut their volumes by several percents.

Such misbalance can be easily explained by two factors. In the European part of Russia the weather was bad in June 2017. Besides, in the west the coverage of modern trade is higher where some federal companies decreased their average prices for beer.

In the territory of the Siberia the output volumes in 2017 fell at two major regional brewers. The region is characterized by unusually high segment of beer in KEG, which is experiencing a fiercer competition between all players.

Under our estimation, in 2017, the output of Tomskoe pivo went nearly …% down, to …-… mln dal. As far as we know, the output decrease was caused by the pressure from federal and regional competitors, which led to the share decline in home Tomsk oblast and in …. Broken down by brands, the market loss was experienced by … as well as , and ….

According to the regional statistics, brewers in Altai region produced 5% less, that is, 21 mln dal of beer. Three major regional breweries are located there: Barnaulskiy Pivzavod, Borihiyskiy Pivzavod, Bochkarevskiy Pivzavod, as well as not big Volchihinskiy Pivzavod.

As far as we know, the lower regional volumes of production resulted from the market share reduction of Barnaulskiy Pivzavod caused by substantial retail price rises at the close of the high season. At that time, there was a decline of … market share. It was apparently a purposeful change of volumes for sales in money, probably in order to avoid pulling sales away from other marginal brands. Besides, high growth rates at Borihinskiy Pivzavod that were registered in 2016, have already stabilized and the market share of draft brands … and … went down in 2017. Bochkarevskiy Pivzavod has probably kept its sales volumes.

According to the yearly report, company Ayan in the republic of Khakassia has expanded beer production by …% to … mln dal. The volumes have grown despite higher retail prices and packed beer sales have increased. Under our estimation, the company’s key brands Abakanskoe and Joy have enjoyed some market share growth.

Judging by the regional statistics the majority of other Siberian independent brewers such as Minusinskiy pivzavod, Chitinskiye klyuchi, and many minibreweries of various scale have increased the output volumes.

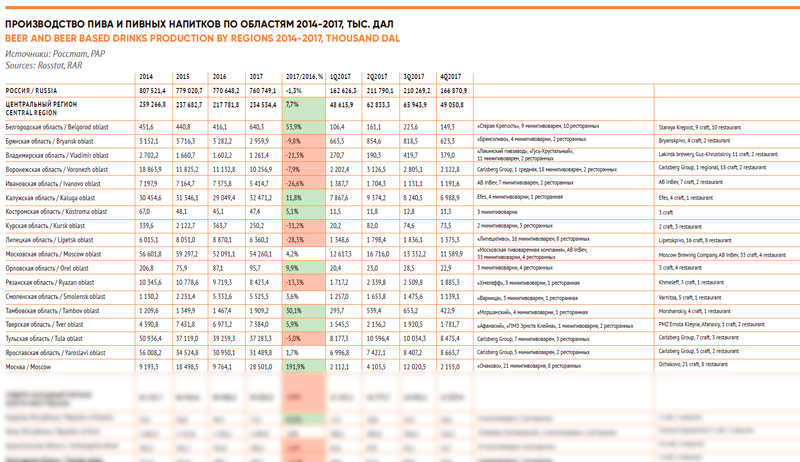

In the Central region of Russia the performance of local brewers in 2017 was quite multivalued.

Judging by regional data, there was a …% nearly to … mln dal output decline at Ryazan company Hmeleff. Such decrease can be explained by a fast growth of retail prices at the beginning of 2017 and lower market share of brands Zhigulevskoe and Russkoe.

In Tver oblast, where holding Afanasiy and PMZ Ernsta Kleina (former Rzhevpivo) are situated, beer output has grown by …%. There the output increase has been obviously linked to regional expansion by Afanasiy company and launching a range of original new products, for example Zhigulevskoe in premium glass package. Yet, what was really creative is the company’s reaction to selling beer in large PET packages on the threshold of the oncoming football cup. The company launched beer Graneney Myach in 4-liter combined package of cupboard and PET.

In Lipetsk oblast, judging by regional statistics there has been a substantial decline of Lipetskpivo output, in particular beer … . To a lesser extent Bryanskpivo has faced a sales loss of …, … and others. Instead, good performance has been shown by small regional brewers with output volumes up to 2 mln dal.

The majority of significant regional brewers in Volga Region experienced a production ramp-down in 2017.

The performance of Trekhsosenskiy Pivzavod in 2017 looks multivalued. Over the previous years, thanks to regional expansion and fast distribution growth of packed beer in all Russian regions Trekhsosenskiy Pivzavod extended its output dramatically. In the first half of 2017, there was also a slow growth, yet then the average retail price for the company’s beer started growing rapidly while the market share on the contrary slid down. The dynamics of brand development was also ambivalent, thus, the market shares of … and … were lost, while brand … went on gaining weight. By regions, Trehsosenskiy Pivzavod has lost a share in the … region and in the …, yet has gone on expanding to the markets of the … region and ….

Under our estimation Bulgarpivo, a major independent brewer in Tatarstan Republic has faced a …% sale reduction to … mln dal. At the same time, company Buket Chuvashii, that is forming a holding with Bulgarpivo has retained the volumes at approximately … mln dal, judging by regional data.

The reduction of Bulgarpivo sales was caused by objective conditions and price pressure from federal companies, for instance the collapse of the market share of … in large PET as well as the decline of their own key brand … . To a big extent the reduction resulted from the rapid average price rises early in 2017. By our estimation Buket Chuvashii has faced a reduction of the market share of … family, however, at the same time, the family of the title brand …, on the contrary reinforced their market positions, which provided stability of sales.

Zhigulevskoe Pivo probably reinforced their position in 2017 in Volga region due to market share growth of the same-named key brand that accounts for the bulk of the company’s sales as well as beer …. The company’s stability was supported by its original focusing on beer sales in glass bottles so the consequences of large PET prohibition did not much affect it. Besides, after a growth of average retail prices for Zhigulevskoe Pivo production in …, they were decreasing rapidly in …. In our view, the output volumes of the company in 2017 could amount to … mln dal.

There has been a further production decline at Kirov brewery Vyatich. Basing on the regional data, their output in 2017 fell by approximately one third, to 2.7 mln dal. The decline was caused by a substantial decrease of the market share of two key brands, namely Vyayich and Zhigulevskoe. This is easily explained by growing average retail price at the beginning of 2017, which was notable for the consumer. The key negative role was played by price pressure in the modern trade from the market leaders.

The production dynamics of a host of other regional brewers with output volumes amounting to … mln dal. of beer has been multivalued but positive in general.

In other regions of the country one should pay attention to Northern Caucasia, with no transnational breweries, yet showing growth in all regions and republics. One can speak of the net growth of many breweries in Stavropol territory, for instance Stavropolskiy pivzavod and Ipatovskiy pivzavod. GK Bavaria has continued expanding production of beer of the same name In North Osetia.

Regional brewers in the Urals have also been doing well, favored by weather in 2017. Company Tagilskoe Pivo managed to keep up the sales volumes due to focusing on glass bottle and launching new products in the family of the core brand Tagilskoe rulit. Besides Kurgan brewery Zauralskie Napitki judging by regional data has enlarged production by …% to … mln dal.

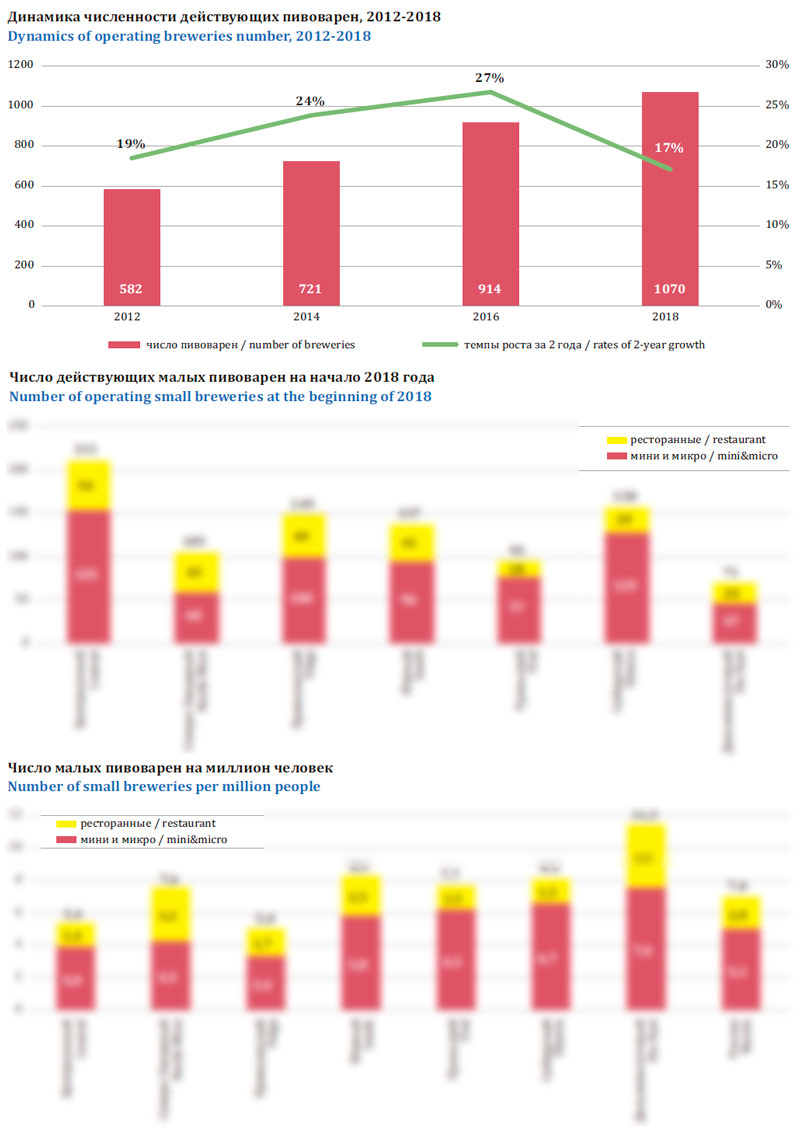

Small brewers: craft is in trend, restaurants are out

The “Catalogue of Russian Beer Producers 2018“, made by us, contains 1070 current brewing productions. In comparison with our data at the beginning of 2016*, their number increased by 156 breweries or 17%. This means slowing the high growth rates that are now below 10% per year. This is probably a result of the strengthening of government regulation. However, we can say that compared to 2012 the number of breweries has already doubled.

* 63 breweries, which opened in 2015 and earlier, were absent from the catalogue of 2016, but were added to the calculation retrospectively, during the update.

In quantitative terms, of the whole mass of production 270 (25%) were restaurant breweries and 693 (65%) were mini and microbreweries, which according to international standards of research companies (small, local, independent) can be named craft breweries.

In particular, at least 134 small productions position themselves as craft (use the word “craft”) and/or produce beers that can be attributed to crafted (for typical sorts, design, and creative presentation). Among these manufacturers, only 20 belong to restaurant breweries, which often prefer classic varieties.

For statistics: in 2016, we observed only a few dozen small producers with obviously “crafty” image. That is, the number of brewers with craft self-definition has increased 4-5 times in two years.

Among the 134 craft breweries we did not take into account contract breweries, and brewers, respectively, that brewed and recorded some contracted sorts.

Note that, in fact, craft breweries probably amount to more than 200, as some producers register only permanent trademarks. While small batches of special beer, the range of which is constantly changing, are separated into a specific line within the existing business.

Geographically, the number of small breweries is the highest in the Central region and Siberia. The smallest number is observed in the North-West region (which is compensated by the number of contract brewers) and the Far East.

If you count the number of beer production in terms of number of inhabitants, it would appear that the further you move East, the greater will be the specific number of minibreweries (with the exception of the Volga region). And if in the Central region there are 4 beer productions per a million people, in the Far East there are almost 8. However, the further you move east, the higher the proportion of very small breweries.

Restaurant breweries are relatively abundant in the Far East, where prior to the devaluation it was quite inexpensive to purchase Chinese equipment or to go get it. And in St. Petersburg a relatively high density of large restaurant breweries compensates for some “drop-out” of industrial minibreweries. In addition, there the largest craft brewery in Russia – Vasileostrovskaya Brewery is located, which a few years ago grew to the level of a regional brewery.

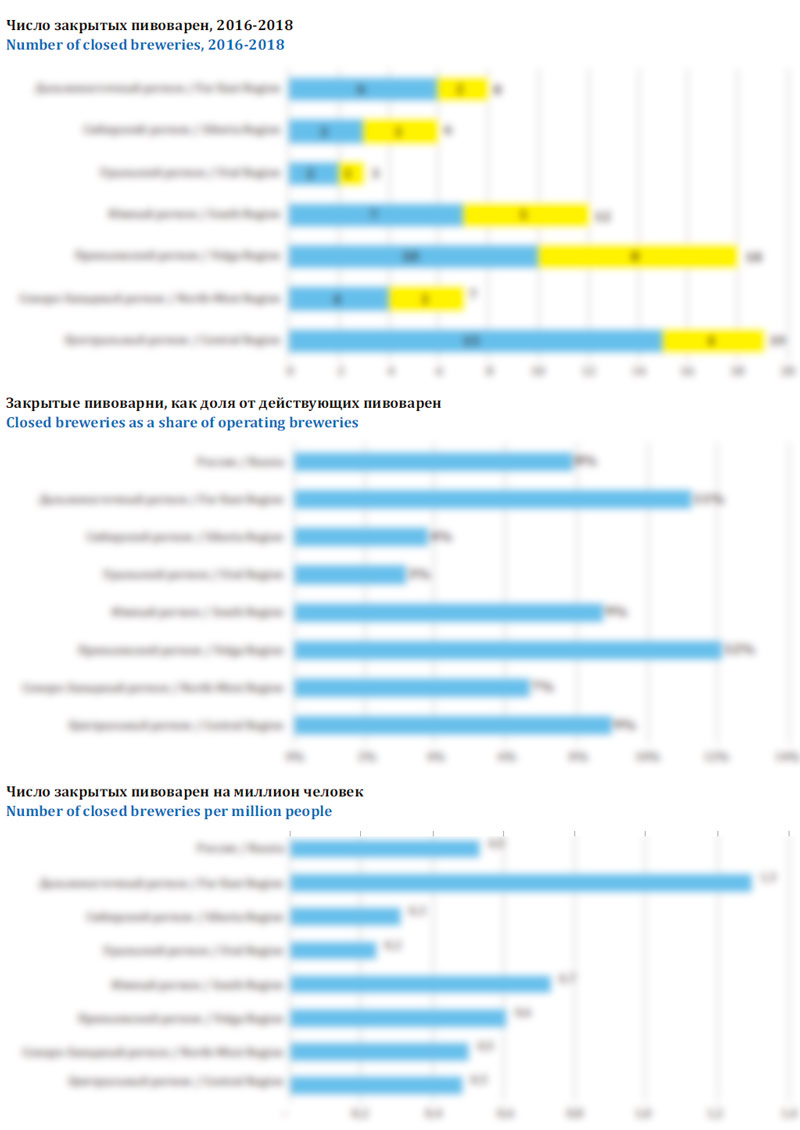

Over two years, the total increase in the number of breweries in Russia was the result of the superposition of two opposite trends – part of the productions stopped working, but newly-launched breweries were much more abundant in number.

According to our estimates, 76 breweries closed, and 234 breweries opened over 2016-2018. That said, we did not consider to be new those productions, that continued to work, but changed their name, business model or ownership.

Breweries of which types were closed more often and which were opened in 2016-2018? Where did this happen?

The greatest losses in volume terms, not compensated by anything, were suffered by major manufacturers – Heineken closed their brewery in Kaliningrad, and AB InBev closed a modern enterprise in Angarsk. Among independent regional companies, despite the negative factors of 2017, only one has dropped out (perhaps temporarily).

Among 73 small manufacturers, that stopped working, the percentage of restaurant breweries is relatively high (27 productions). Of the 47 industrial type productions, the vast majority were very small local minibreweries that released several classic beers. Some of them hardly started working. Thus, the current retirement of minibreweries, in terms of volume or variety, had little impact on the overall situation.

If you look at the retired breweries in the regional context, the most severely affected was the Far East region (in two years, 11% of breweries closed there) and the Volga region (12%). The most stable ones turned out to be small business in Siberia (closed 6%) and the Urals (3% of the retired).

When you consider the number of closed breweries, as the coefficients 1) in terms of the population of the regions and 2) in terms of the number of operating enterprises, the picture will look about the same – Siberia and the Urals look noticeably better than other regions from the point of view of sustainability of small brewing business.

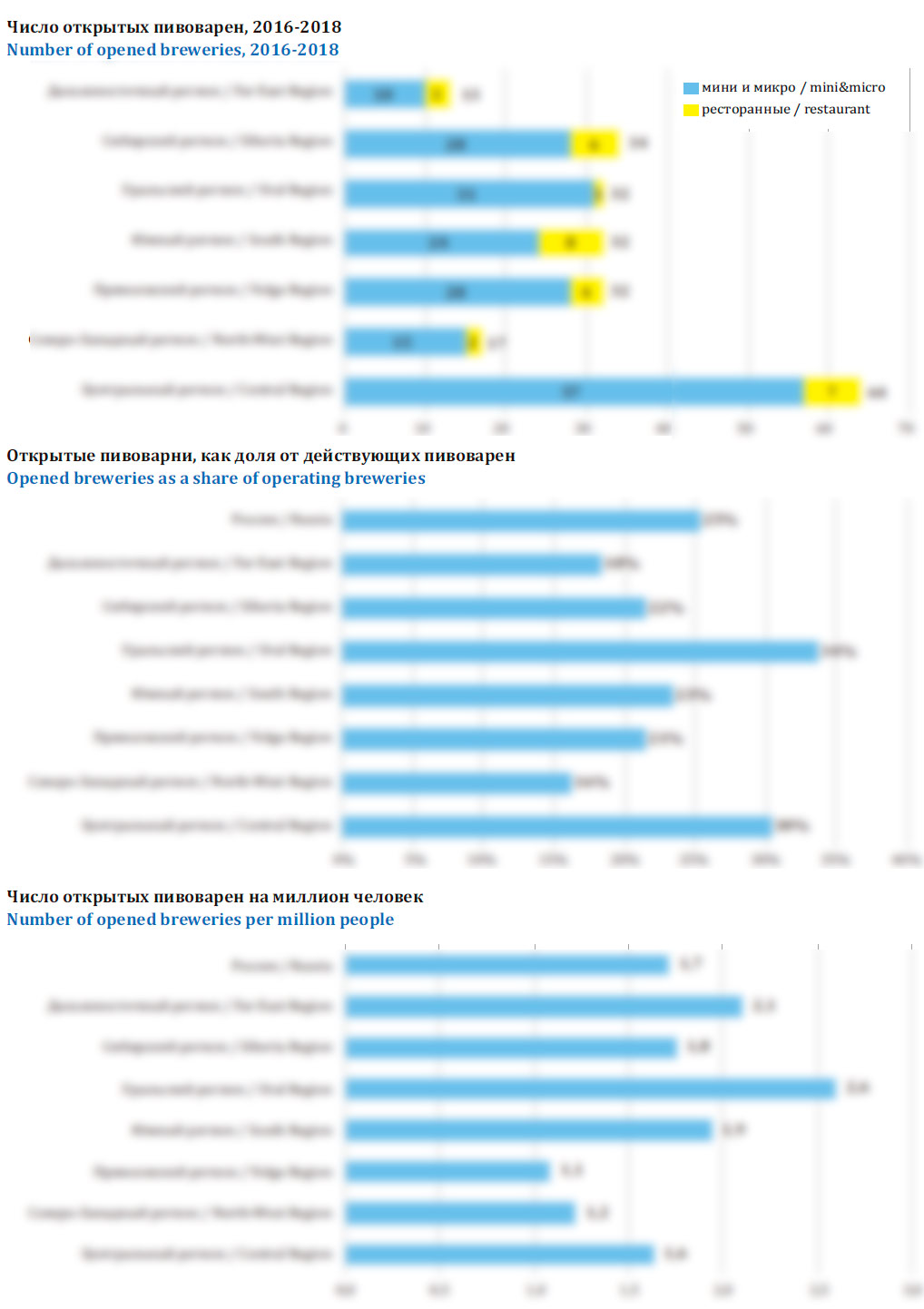

Data on the emergence of new breweries in most cases complements the picture with their closure. By analogy with the demographics of the population in the prosperous regions “birth rate” is greater than “mortality”.

In absolute figures by the number of open breweries the leader is undoubtedly the Central region, where in 2016-2017, according to our data, 64 breweries opened. However, if you look at relative numbers, than the Urals are leading, both in the share of newly-opened breweries in proportion to the number of already existing ones, and in terms of number of inhabitants. Two-year results of the launch of new breweries in the Volga region look pretty modest (probably due to economic and social reasons) and in the North-West region (where the market is apparently saturated).

Approximately half of the newly opened breweries position themselves as craft ones. In turn, most of them opened in Moscow and St. Petersburg, where the majority of fans of special beer live.

One should also note a significant slowdown in the number of restaurant breweries. These include only 34 of the 234 newly opened breweries, which corresponds to 14.5%. And, as you can see, this share is below the overall proportion of existing breweries.

Taking into consideration establishments that closed (or stopped brewing beer), we can say that the format of a small brewery in a restaurant is becoming less popular. This is easily explained by the fact that the problems that arise today in the administration of the beer production negate the potential economic effect of its sale to visitors, or the effect of attractiveness growth of an establishment with its own brewery. As for the restaurant business beer production is often a secondary supplement, it is more likely to be given up.

Outlooks for 2018…

The year of 2018 can be marked by the beer sales growth as well as by changes linked to integration processes at AB InBev Efes that will influence the companies’ positions.

The results of the first quarter of 2018 look ambiguous. Market audit data referenced by the market participants show a weak positive trend. At the same time, monthly statistics of production indicate a reduction of approximately 5%.

The dynamics of the second quarter of 2018 will be influenced by some short-term oppositely acting factors:

The negative factor is very cold weather in April, which clearly affected the sales of beer and not allowed to “swing” the consumption at the beginning of the season. In addition, consumer sentiment may suffer from the April devaluation of the ruble and negative external political background.

The positive trend is the low base effect in 2017, when the restrictions not only on production but also on the sale of beer in PET entered into force.

An additional percentage of beer sales in the summer of 2018 can be added by 2017 low base associated with bad weather. June of 2017 was cool in the European part of Russia, where the most of the country’s population lives, that is, from Saint-Petersburg to the Volga region (in the Urals and Siberia region it was warm, yet they are considerably less densely populated).

Finally, in the second quarter of 2018, beer consumption can be spurred by the FIFA World Cup final that will be held in 11 Russian cities from June 14 to July 15, 2018.

Thus, despite the negative beginning of 2018, according to its results one would expect a weak growth in production and sales of beer, which would strengthen the focus on market stabilization.

The integration of operational activity of AB InBev and Efes will probably lead to a reduction of the joint company’s market share. It is possible that the reduction of AB InBev market share in 2017 was the beginning of this process.

Here we should pay attention to the past experience.

Under our estimation, mere summing of shares of Efes and SABMiller in 2011 provided about 16% of the market to the companies, yet over 2012, the share of the newly formed company was falling and in 2013 amounted to nearly 13%.

What exactly led to the decline in the course of the previous integration?

Due to the merge, all licensed and large Russian brands kept their place in the joined portfolio, while the share of economy brands and Zolotaya Bochka, a major brand belonging to SABMiller, started decreasing. SABMiller’s volume loss was caused by temporal cease of SABMiller’ sales at modern retail, as agreements with supermarkets had to be made again. Besides, obviously, in case of joining of two companies’ shelf spaces and brand portfolios, there will inevitably be some reduction due to cannibalism and optimization.

Because of volume decline Efes has suspended operation at two breweries. And as a rule, brewery closing negatively affects any company’s regional market share due to logistics reorganizing, lower beer availability, disappearance of regional brands, lack of regional authority support as well as many other objective and subjective reasons.

Quite probably, all enumerated factors will negatively influence the market share of AB InBev Efes in 2018 too.

Joined brands portfolio of AB InBev Efes looks too big and some brands are likely to disappear from it while others can change their market positioning and get cheaper.

Three brands from the global portfolio of AB InBev (Bud, Stella Artois, and Corona) as well as so far actual for European markets Staropramen will hardly face any revision. At Efes there are emerging a threesome of leaders, namely, Velkopopovicky Kozel, Miller, and Bavaria that demonstrated great performance in 2017 as well as the title brand. In the blurred segment “premium” or “upper mainstream” one can clearly see two famous brands that did comparatively well in 2017, that is Stariy Melnik and Sibirskaya Korona.

As for the lower price segment, the joint company’s brands have worse prospects as Zolotaya Bochka by Efes and Klinskoe by AB InBev found themselves among outsiders both in the long period and in 2017. Klinskoe decline looks especially eye-catching.

Besides, if we brought the situation of 2012 to the new realities, one could expect that the economy brands market share to shrink. As a result one or several breweries can stop operating. Basing on the dramatic decline of output volumes, in 2017, AB InBev brewery in Volzhskiy seems to be in danger.

However, despite all the negative factors, one should keep in mind that in the long run the market share of Efes has recovered after 2012, and the company’s weight has grown considerably.

State regulation in 2018 is not likely to influence the market dynamics. The worse for brewers initiatives such as: beer marking, production and sales chain licensing, banning individual entrepreneurs to sell beer and obliging minibreweries with a capacity of less than 100 thousand dal (instead of 300) to mount counters have been voted down by the government or postponed indefinitely.

Among dangers of 2018, let us pay special attention to the ban on beer sales at apartment blocks which has become a widely-spread initiative in many cities, damaging specialized retail. Besides, to our mind, the keg beer segment has been close to saturation. Yet, in 2017 draft in off-trade got an incentive from another prohibition, that is, on beer sales in large PET packages. The sales increase in 2017 failed to compensate for the losses of beer sales in PET of regional brewers which led to a short-time reduction of their share. Thus, in 2018 provided there are no other shocks, regional producers can stabilize their positions in case of reasonable price policy.

In the long term, there is a threat of further limits on PET volumes. Note that the limit to 1.5 was to a large extent connected to government support to major aluminum producer Rusal.

In April 2018, members of the ruling party brought in a bill concerning prohibition to output and sell alcohol in PET package: from January 2019 in volume of more than 1 l, from January 2020 in volume of more than 0.5 l. It actually means refusing PET package.

It happened so, several days after that, a new set of the USA sanctions affected Rusal, whose export supplies came under the cosh. Currently, the government can take different steps to support the company, and there will be more risks that the bill becomes a law (possible in a lighter version).

But first we should assess the effect the seller of aluminum can obtained from the ban that has already been introduced.

Aluminum can partially substituted for beer in PET almost till September 2017. By the end of the year, the share of can increased by … p.p. There appeared a certain synergy with the trend of market premiumization and the sales growth of licensed brands (it might have brought … p.p.) Still, half of PET lost volumes flowed first to kegs and than to PET again when was sold via specialized retail.

A very rough estimation shows that in 2017 canned beer consumption was likely to grow by …% to nearly … bn cans of 0.5 l. To company Rusal having a turnover of $10 bn the profit from selling additional … mln cans seems insignificant as the wholesale price for a can amounts to several rubles.

To get the full article “Leaders’ Plays and Regionals’ Shares” in pdf (54 pages, 25 diagrams, 1 table) propose you to buy it ($35) or visit the subscription page.

2Checkout.com Inc. (Ohio, USA) is a payment facilitator for goods and services provided by Pivnoe Delo.

The article is prepared using the data by Rosstat, Federal Service of Alcohol Market Regulation, “Catalogue of Russian Beer Producers 2018”, presentations and reports by brewing and research companies. At the article preparation publications in editions Kommersant, Sostav.ru (OMD OM Group), and Vedomosti were used.

The data on output volumes and their interpretation are our assessments based on the regional statistics and current trends in case the source has not been named.

We do not claim the given information to be absolutely correct, though it is based on data obtained from reliable sources. The article content should not be fully relied on to the prejudice of your own analysis.